Interim management report as of 30 June 2017 – Press release

02 August 2017 - 07:31 price sensitive

Positive first half performance: improved net profit and operating result. Operating return on equity again above target

- Net profit increased to € 1,221 mln (+3.7%), thanks to the positive performance in all areas of operation

- Operating RoE stood at 13.6% (target >13%)

- Operating result up to € 2.6 bln (+4.1%), despite the current low interest rate environment, reflecting the improved profitability in the Financial and Property&Casualty segments

- Technical performance confirmed at excellent levels with CoR at 92.9% and Life New Business Value at € 942 mln rising by 52%, with a margin of 4.11%

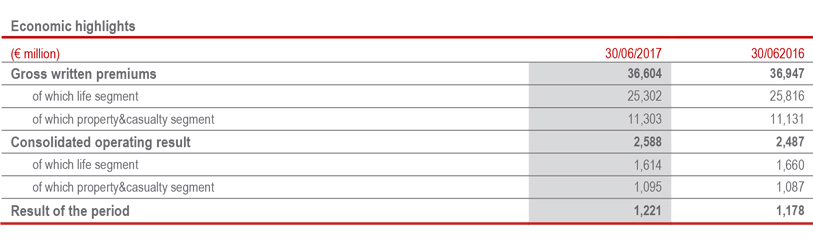

- Premiums solid at € 36.6 bln (-0.8%1). Growth recorded in P&C business (+1.5%); in Life, net inflows stood at best in class levels exceeding € 5.7 bln

- Improved capital position with Regulatory Solvency Ratio2 at 188% and Economic Solvency Ratio at 207%

Generali Group CEO, Philippe Donnet, declared: “Generali’s first-half results confirm the solidity of our business and the efficient execution of our industrial transformation. The Combined Ratio at 92.9% and the New Business Value, which registered a strong increase of 52% with a margin of 4.11%, continue to remain at excellent levels. The rise in P&C premiums together with the solid and continued high-quality Life net inflows, are a result of our focused and disciplined approach to growth. The successful execution of our strategic plan led to today’s positive results with a 3.7% rise in net profit, operating RoE remaining above our target and an overall increase in capital-light products. We are achieving our financial goals thanks to the determination, the focus and the commitment with which we are implementing our strategy to make Generali ‘simpler & smarter’.”

Milan - At a meeting chaired by Gabriele Galateri di Genola, the Assicurazioni Generali Board of Directors approved the consolidated results as of 30 June 2017.

Executive Summary

Generali Group’s results in the first six months of the year highlight an excellent performance in terms of profitability and capital strength. The results confirm the effective and disciplined management of our business targeted at pursuing its strategic objectives. The Group’s performances were obtained in a recovering macroeconomic context, albeit with interest rates that have remained low, with growth in the equity markets, especially in the second quarter, a gradual increase in returns on German bonds and a tightening of spreads of Euro peripheral countries.

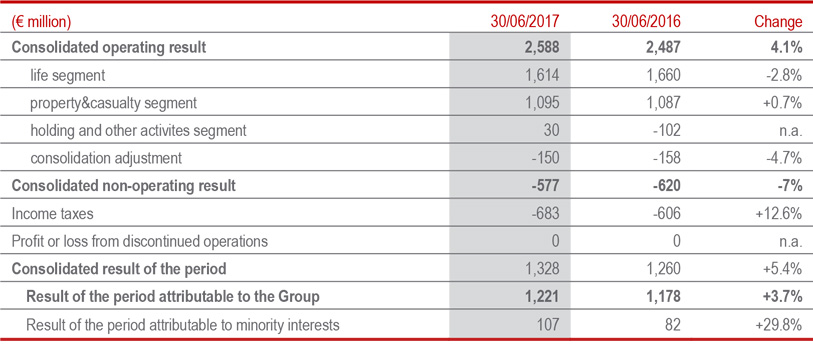

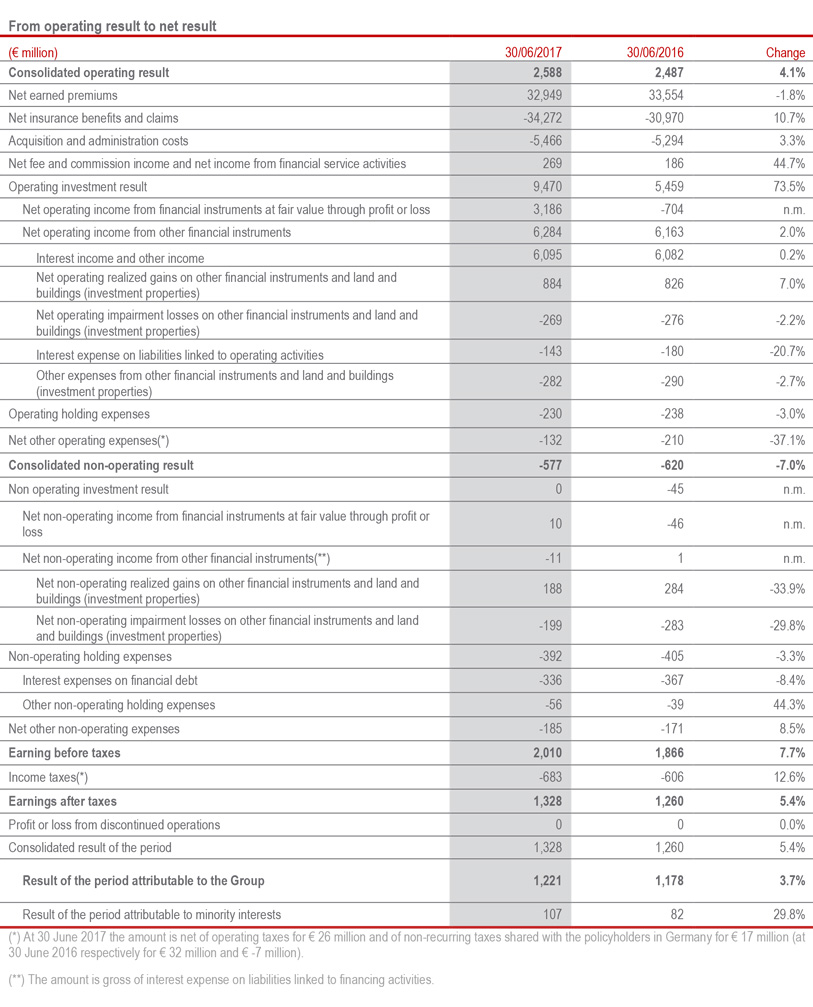

The operating result rose by 4.1% to € 2,588 million (€ 2,487 mln 1H16) reflecting the development in the P&C segment, with a combined ratio that was confirmed at excellent levels (92.9%), and in particular the Holding and other businesses segment, mainly thanks to the excellent performance of Banca Generali, the reduction in the Operating holding expenses (-3%) and significantly higher income from private equity and the property sector recorded in the second quarter of the year. The Life technical margin net of insurance expenses fell slightly. The operating financial performance reflects, on the one hand, a context of low interest rates and the impact of foreign exchange translation effects and, on the other, the higher realised gains registered in the period as a result of the seizing of financial market opportunities.

Therefore, the Group maintains excellent operating profitability levels, measured through the annualised operating RoE, equal to 13.6%, in line with the plan objective.

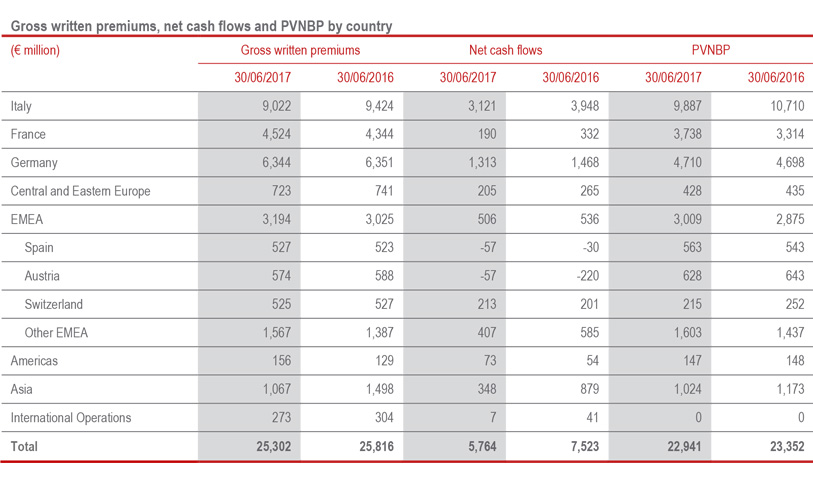

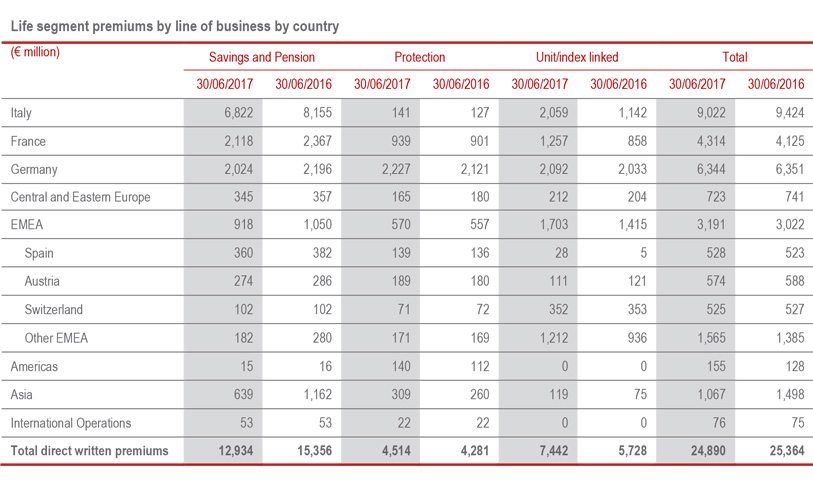

With reference to volumes, Life Net cash inflows remains solid exceeding € 5.7 bln. The decrease of 23% reflects the more selective underwriting policy in the savings line and a targeted rebalancing in favour of products offering better risk-return terms. Furthermore, Italy, France and Ireland experienced an increase in surrenders. Life gross written premiums, amounting to € 25.3 bln, recorded a drop of 1.8%, due to the continuation of the aforementioned strategic objectives, savings products declined by 15.5%, while unit-linked policies registered significant growth (+30%) in particular in Italy and France, together with a remarkable growth in the protection line (+5,4).

New business in terms of present value of new business premiums (PVNBP) amounted to € 22,941 million (-1.6%). As a result of the aforementioned execution of the strategic objectives, savings production decreased (-22.6%), counterbalanced by the increase in unit linked (+44.3%) and protection business (+8.2%). Notwithstanding the slight slowdown in PVNBP, new business value (NBV) recorded a sharp increase (+51.8%), totalling € 942 million (€ 627 mln 1H16). The above mentioned Group actions aimed at selective underwriting and product rebalancing, boosted the PVNBP margin to 4.11%3 (2.68% 1H16), up by 1.44 p.p..

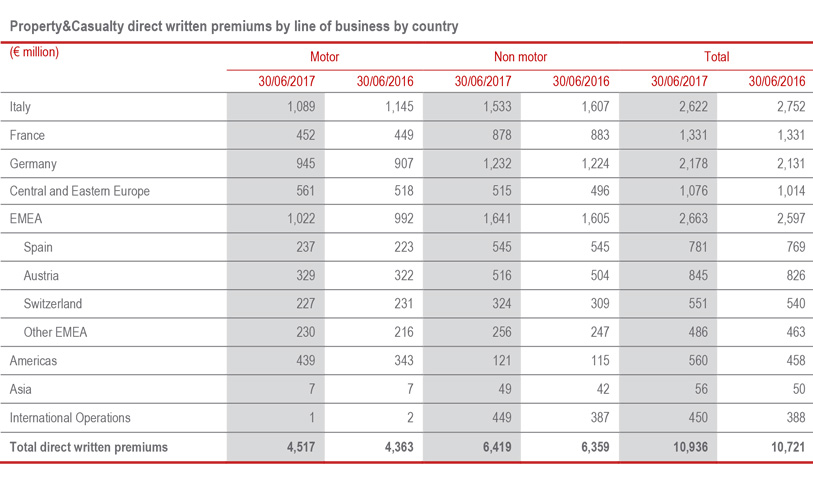

The growth observed in the P&C premium income in the first quarter continued, and rose to € 11.3 bln (+1.5%), due to the increase in the Motor segment (+3.7%), concentrated in particular in Germany, in Central and Eastern European countries and in the Americas. Premiums in the Non- Motor segment were also positive (+0.8%).

Total gross written premiums of the Group consequently reached € 36.6 bln, a slight drop (- 0.8%) compared to the previous year.

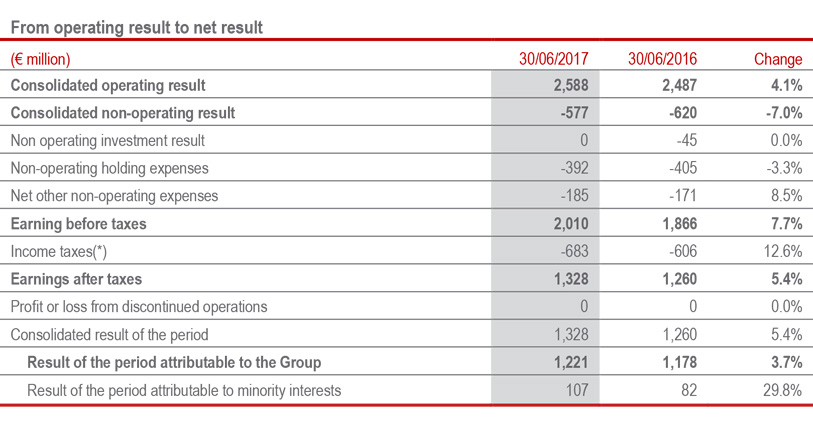

The Non-operating result improved to € -577 mln, reflecting better financial performances, lower interest on financial debt and lower restructuring costs.

The aforementioned positive economic performances, partially offset by the greater weight of taxes, which went from 31.6% to 32.5%, are reflected in the Result of the period attributable to the Group of € 1,221 mln, up by 3.7% compared to € 1,178 mln in the half in 2016.

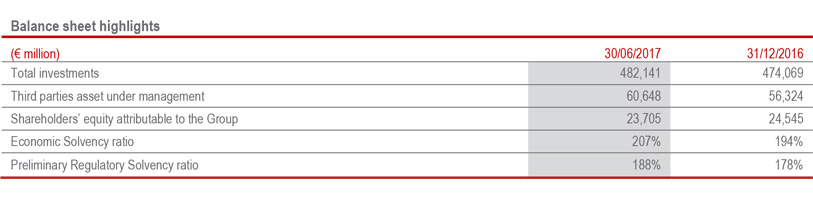

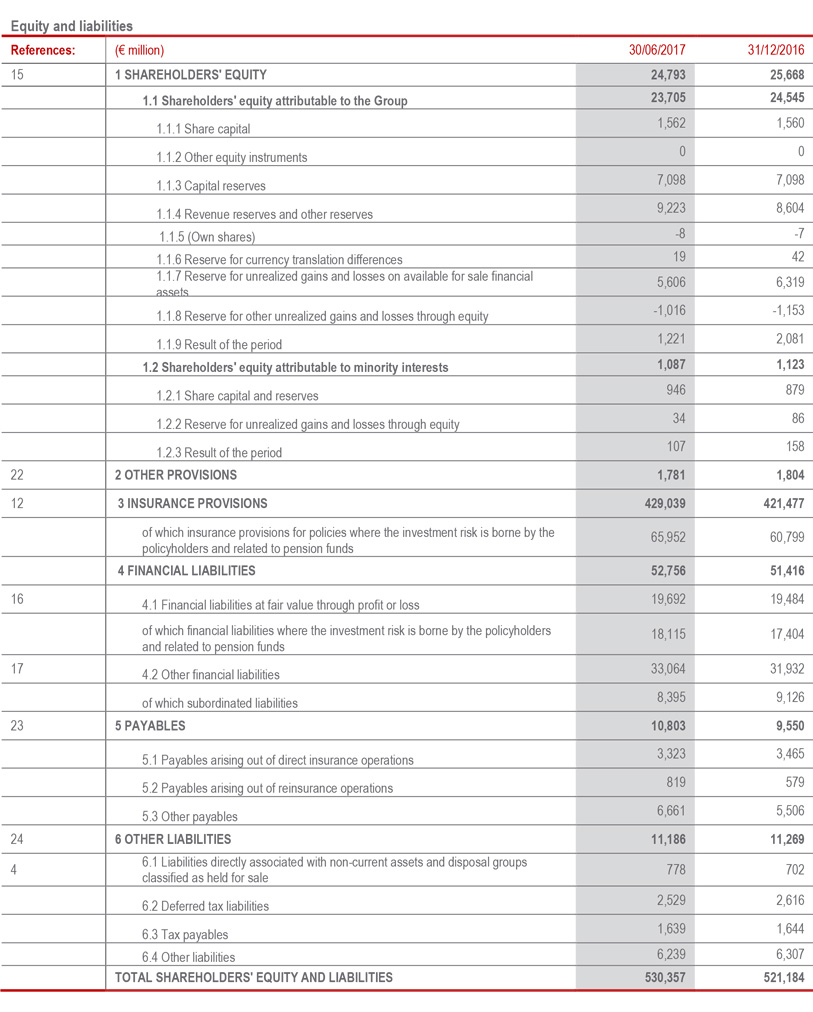

The shareholders’ equity attributable to the Group remains solid amounting to € 23,705 mln, down by 3.4% compared to the € 24,545 mln at 31 December 2016. The change was due to the result of the period attributable to the Group, amounting to € 1,221 mln, more than offset by the payment of the dividend totalling € 1,249 mln and the reduction of € 713 mln in the reserve for unrealized gains and losses on available for sale financial assets.

The Preliminary Regulatory Solvency Ratio – which represents the regulatory view of the Group’s capital and is based on use of the internal model, solely for companies that have obtained the relevant approval from IVASS, and on the Standard Formula for other companies – stood at 188% (178% FY 20164; +10 p.p). The trend is due to normalised generation of capital, net of the accrued dividend for the current year, and the positive trend of financial markets.

The Economic Solvency Ratio, which represents the economic view of the Group’s capital and is calculated by applying the internal model to the entire Group perimeter, stood at 207% (194% FY16; +13 p.p.).

Life segment: NBM up, disciplined underwriting approach, solid operating performance in a context of low interest rates

- Life net cash inflows exceed € 5,7 billion

- NBM improves to 4.11%

Life net cash inflows - premiums written net of claims and lapses - reached more than € 5.7 bln. The decrease of 23% reflects decreases in France, Italy, Germany and China, primarily as a result of the trend in premiums. France and Italy also felt the effects of the trend in lapses, which also rose in Ireland.

Life premiums, amounting to € 25,302 mln, recorded a drop of 1.8%, due to the continuation of the more selective underwriting policy for savings products (-15.5%) and the rebalancing in favour of products offering better risk-return terms, such as unit-linked products (+30%) and protection contracts (+5.4%).

With reference to the main countries in which the Group operates, Italy recorded a decrease of 4.3%, due entirely to the aforementioned savings products underwriting policies, while unit-linked policies registered significant growth (+80.2%) deriving from hybrid products, as well as protection policies (+11.2%). Also France, which grew by 4.1%, and Germany, whose premium income is stable, recorded trends similar to those of Italy, with growth in unit-linked policies, especially in France (+46.5%), and protection policies. Central and Eastern European Countries registered a decrease of 3.4%; the growth recorded in unit-linked policies is actually offset by the fall in savings and protection products.

After a particularly favourable 2016 in terms of premium income, thanks in particular to the bancassurance channel in China, premiums in Asia recorded a drop of 25.5%, accompanied by a major improvement in the new business margin.

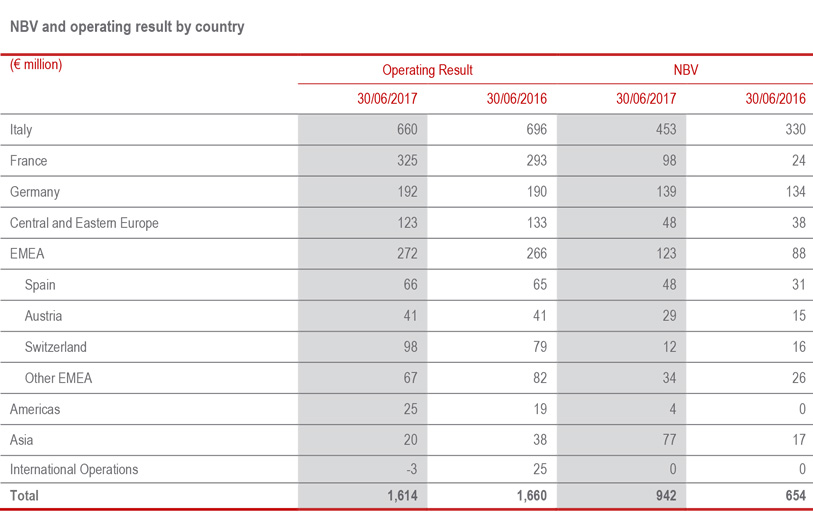

New business in terms of present value of new business premiums (PVNBP) amounted to € 22,941 million (-1.6%; € 23.352 mln 1H16). As a result of the aforementioned execution of the strategic objectives, savings production recorded a general decrease (-22.6%) in the Group's main operating countries, in particular in Italy (-24.7%) and in Germany (-26.6%). On the contrary, unit linked showed an increase (+44.3%), concentrated in Italy, whose new production doubled, in France (+56.3%) and in Germany (+ 16.6%). The protection line was also positive (+ 8.2%), particularly in France (+33.6%). Notwithstanding the slight slowdown in PVNBP, new business value (NBV) recorded a sharp increase (+51.8%), totalling € 942 million (€ 627 mln 1H16). The mentioned action aiming at selective underwriting policy and product rebalance, boosted the PVNBP margin to 4.11% (2.68% 1H16), up by 1.44 p.p., despite the less favorable economic scenario than the first half of 2016.

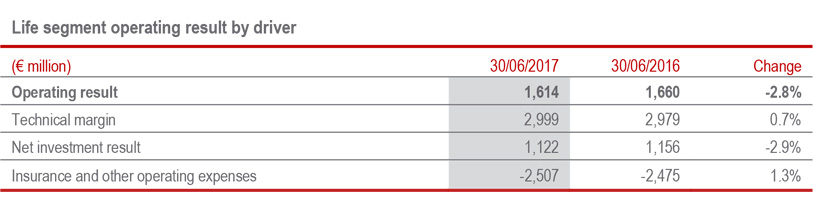

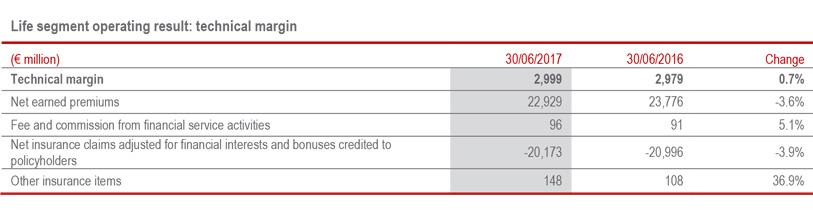

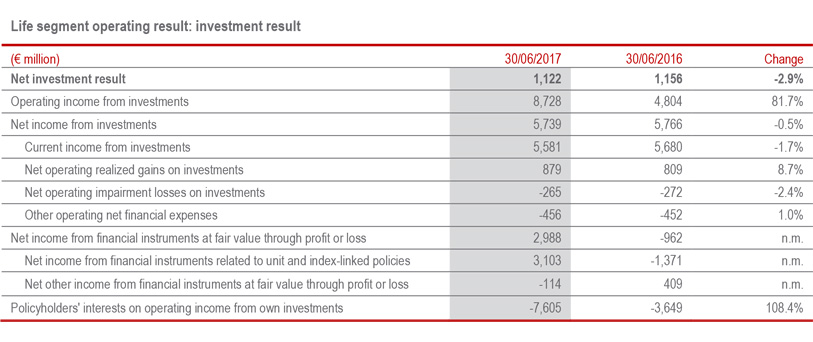

The Operating result of the life segment came to € 1,614 mln (€ 1,660 mln in 1H2016; -2.8%), reflecting the contraction in the technical margin net of insurance and other operating expenses. The financial performance was also down (-2.9%) due to a lower contribution from current income and impact of foreign exchange translation effects.

With reference to the main countries of operations, a solid contribution was made to the Group result by Italy, Germany and France, despite the low interest rates. France recorded significant growth in the operating result, thanks to the increase in the technical margin, which benefitted from a better business mix.

Finally, the operating return on investments of the life segment stood at 0.38% (0.40% in 1H16).

The expense ratio - the ratio between costs and the earned premiums - went from 9.6% in 1H16 to 9.9% in 1H17, due to the increase in administration costs ratio (+0.2 p.p.) and acquisition costs ratio (+0.1 p.p.).

Property&Casualty segment: increase in premium income, solid technical profitability

- Premiums up to € 11.3 bln (+1.5%), thanks to the strong Motor (+3.7%) and Non-motor (+0.8%) performance

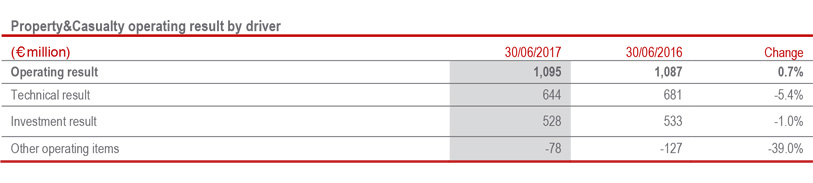

- Solid operating result at € 1,095 mln (+0.7%)

- Combined ratio confirmed at excellent levels: 92.9% (+0.5 p.p.)

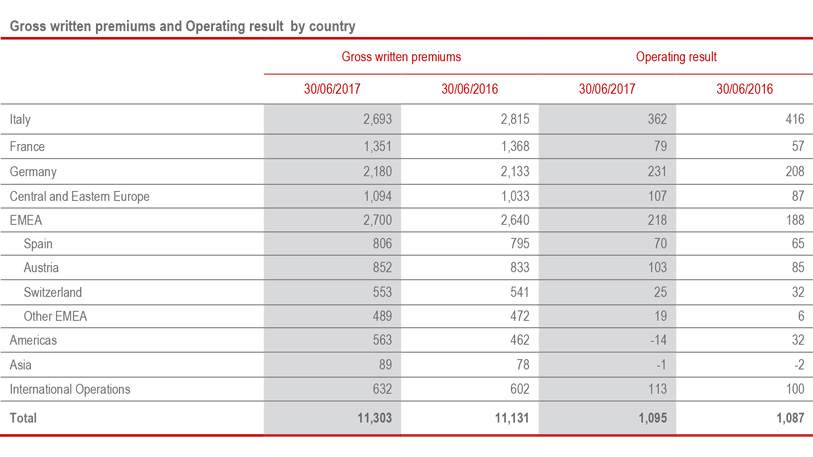

Positive performance recorded by P&C premiums which increased to € 11,302 mln, thanks to the increase in the Motor segment (+3.7%), concentrated in particular in Germany, Central and Eastern European countries and in the Americas. The decrease of 4.9% in Italy reflects the prolonged contraction of average premiums and the portfolio. A positive performance was also recorded in the Non-Motor segment (+0.8%), which increased in the main countries of Group operations, with the exception of Italy (-4.6%), which reflects the drop in premium income of Global Corporate&Commercial. Premiums were essentially stable in France (-0.5%).

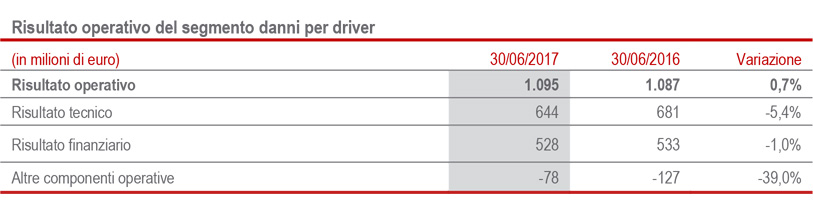

The operating result amounts to € 1,095 mln (€ 1,087 mln in 1H16; +0.7%). The technical margin is influenced by the increase in the acquisition cost component reflecting the rebalancing of the portfolio towards the Non motor segment, while the financial result remains solid, despite interest rates remaining low. An improvement was registered by the other operating items, that, during the period, benefitted from lower allocation to risk provisions.

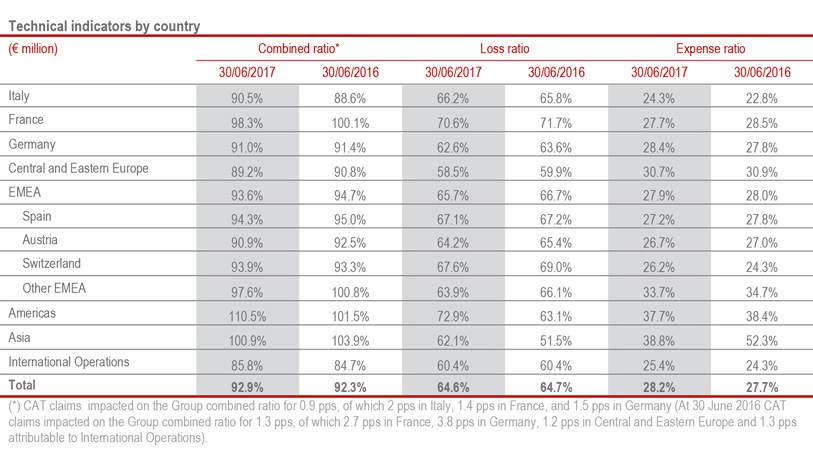

The combined ratio stands at 92.9% (+0.5 p.p.). The half just ended was affected by catastrophic events for around € 93 mln, relating mainly to the severe winter and the bad weather of late June in Italy, storms in Germany and France, impacting for a total of 0.9 p.p. on the CoR (1.3 p.p. in the first half of the previous year). The current year loss ratio excluding natural catastrophes increased (+0.4 p.p.), due to the evolution observed in the Non-Motor segment. The contribution of previous generations remained stable at -4.4 p.p.

As regards our main countries of operations, in Italy, the CoR rose to 90.5% (+1.9 p.p.), impacted by higher natural catastrophe claims of 2 p.p. The CoR improved in Germany, standing at 91.0% (-0.4 p.p.), thanks to the positive development of the loss ratio, which benefitted from a lower impact of natural catastrophe claims equal to 2.4 p.p.. The improvement in the combined ratio in France continues, equal to 98.3% (-1.9 p.p.); net of the benefit deriving from the lower increase in natural events (-1.3 p.p. compared to HY16), the CoR would, nonetheless, still improve thanks to the evolution in the expense ratio. The CoR in CEE countries improved to 89.2%, the best Group ratio, down 1.6 p.p.; this performance reflects the absence of natural catastrophe claims (1.2 p.p. in HY16) and benefits from the positive trend in the loss ratio in the Motor business. The CoR increase in the Americas (from 101.5% to 110.5%) is entirely due to the observed growth in Argentina, reflecting an adjustment of the local reserve for some classes of claims following the inflationary dynamics observed during the period.

Holding and other business segment5

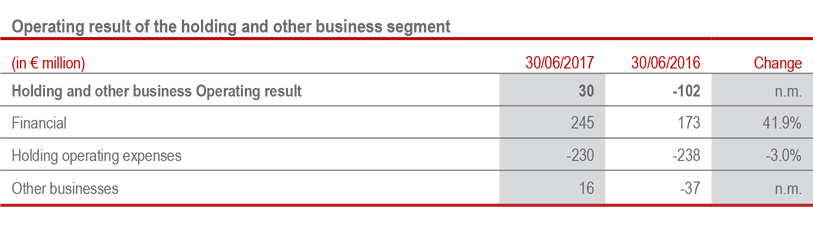

The operating result of the Holding and other activities segment went from € -102 mln to € 30 mln, thanks to the positive contribution from all sectors. In fact, the Financial operating result increased, going from € 173 mln to € 245 mln due to the excellent performance of Banca Generali as a result of the equity markets performance.

Operating holding expenses improved to € -230 million (€ -238 mln 1H16), primarily thanks to the reduction of personnel costs.

The operating result of other activities went from € -37 mln to € +16 mln, due to higher income from the private equity and property sectors, benefitting from favourable conditions in the financial and property markets.

From operating result to net result

The Non-operating result of the Group went from € -620 mln to € -577 mln. This performance reflects the improvement in the result of investments and the reduction of non-operating holding expenses.

In particular, the Non-operating investment result improved by € 44 mln, due to lower impairments on financial investments, partially offset by less realised gains compared to the previous year.

The non-operating holding expenses went from € -405 mln to € -392 mln, reflecting the drop in interest on financial debt which went from € -367 mln to € -336 mln.

Finally, other net non-operating costs went from € -171 mln to € -185 mln. This item mainly consists of € -52 mln for the amortisation of the value of acquired portfolios (€ -62 mln 1H16) and € -54 mln for the restructuring costs (down compared to € -91 mln in 1H16). The variation in other net non-operating costs with respect to the previous year was mainly determined by allocation to risk provision.

The tax rate increased to 32.5%, (31.6% in 1H16); in the first half of the previous year, the tax rate had benefitted from a more positive non-recurring income on taxes for previous years.

The result attributable to minority interests, amounting to € 107 mln, which corresponds to a minority rate of 8.1% (6.5% 1H16), increased when compared to € 82 mln in the previous year due to the results of Banca Generali.

As a result of the performances commented on above, the result of the period attributable to the Group rose by 3.7% to € 1,221 mln (€ 1,178 mln 1H16).

Group financial position

Shareholders’ equity and Group solvency

Share capital and reserves attributable to the Group amounted to € 23,705 million as at 30 June 2017, a decrease of 3.4% compared to € 24,545 million as at 31 December 2016. The change was due to the result of the period attributable to the Group, amounting to € 1,221 million, more than offset by the payment of the dividend totalling € 1,249 million and the reduction of € 713 million in the reserve for unrealized gains and losses on available for sale financial assets.

Group investments policy

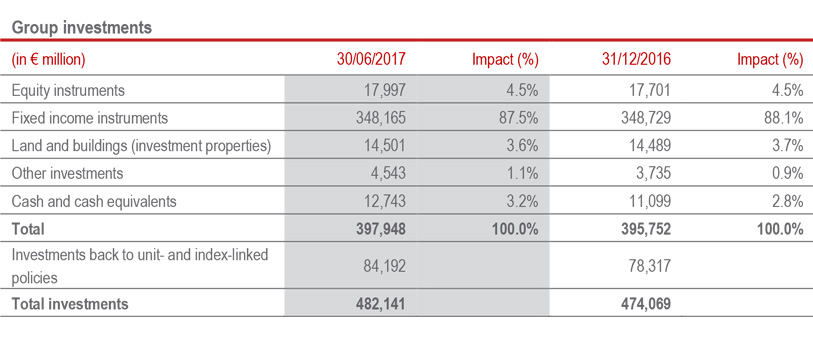

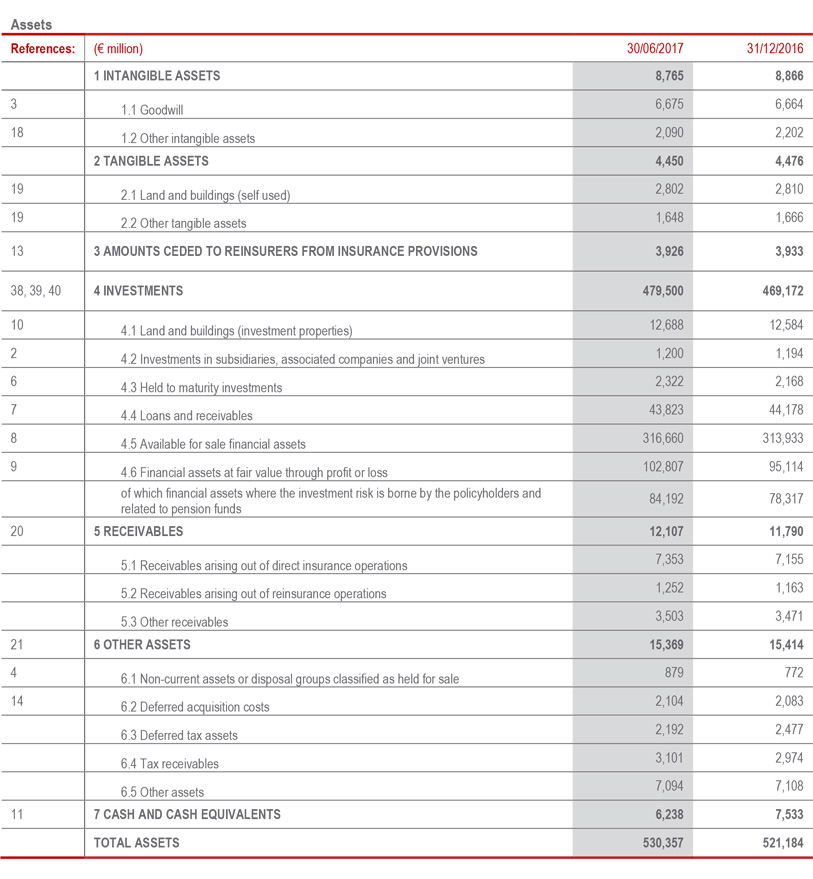

Group’s total assets under management recorded an increase of 2.3% at 30 June 2017, up to € 541,3 billion. In particular, total investments amounted to € 482,1 billion, while third party assets under management came to € 59,2 billion.

Total investments, amounting to € 397,9 billion, recorded an increase of 0.6%, mainly due to the increase in cash and cash equivalents and the rise in the equity sector owing to the recovery in share prices. The bond portfolio showed a slight decrease in relation to the increase in interest rates, which more than offset the net purchases in the period, concentrated on government bonds in particular.

Other investments registered an increase due mainly to the rise in the value of derivatives. With reference to cash and cash equivalents, the former remained substantially stable, while the latter item recorded an increase, mainly due to the increase in repurchase agreements, used to hedge some Group companies’ exposure to currency risk.

Investment properties remained substantially stable.

The investment strategy for fixed-income investments aims at portfolio diversification, in both government bonds and corporate bonds. The objective is to ensure adequate returns for the policyholders and a satisfactory return on capital, while maintaining a controlled risk profile.

Equity and investment property exposure will be kept substantially stable.

SIGNIFICANT EVENTS WITHIN THE PERIOD AND AFTER 30 JUNE 2017

Appointments of Group CFO and GMC

The Board of Directors of Assicurazioni Generali on 25 January decided to appoint Luigi Lubelli as Group CFO, who also joined the Group Management Committee, as a consequence to the termination of employment relationship with Alberto Minali. It also decided that the Investments Committee would expand its responsibilities to strategically relevant operations, so its name was changed to the Investments and Strategic Operations Committee.

Marco Sesana, Country Manager of Italy, and Timothy Ryan, incoming Group Chief Investment Officer, become members of the Group Management Committee.

Early redemption of perpetual subordinated bond

Generali Finance B.V. exercised the early redemption option on the perpetual subordinated notes on 8 February 2017. This debt has already been refinanced through the subordinated bond, concluded on 8 June 2016, for an overall amount of € 850 million, targeting institutional investors.

Mazzocco designated as the new Generali Real Estate CEO and general manager

On 16 March the Board of Directors of Assicurazioni Generali has approved the designation of Aldo Mazzocco as the new CEO and General Manager of Generali Real Estate, who entered in the Board of Directors of Generali Real Estate in June.

Share capital increase

On 20 April Assicurazioni Generali completed the share capital increase in execution of the Long Term Incentive Plan approved by the Shareholders’ Meeting of the Company on 30 April 2014. The share capital of Assicurazioni Generali S.p.A., fully subscribed and paid up, is subdivided into 1,561,808,262 ordinary shares of € 1 each (par value).

Fitch conferms rating A- and Stable outlook

On 26 April, Following Fitch’s recent downgrade of Italy’s sovereign rating to 'BBB' from 'BBB+', with Stable Outlook, the agency announced that it has affirmed Generali’s and its core subsidiaries' IFS ratings at A-. The outlooks are Stable. Fitch said that the ratings are two notches higher than Italy’s sovereign rating (BBB/Stable), “in recognition of Generali’s resilient capital position and strong geographical diversification (with around 60% of operating profit from outside Italy), including significant operations in France and Germany with strong market positions”.

Generali Board approves the Group’s new Charter of Sustainability Commitments

Assicurazioni Generali’s Board of Directors has approved the Group’s new Charter of Sustainability Commitments. This policy document defines Generali’s position regarding sustainability and identifies its commitments towards stakeholders.

2016 financial statements approval and appointment the board of statutory auditors

On 27 April the ordinary and extraordinary General meeting approved the financial statements for the year 2016 and appointed the Board of Statutory Auditors for the three-year period 2017-2019. Carolyn Dittmeier (Chairwoman), Lorenzo Pozza and Antonio Di Bella were elected as Auditors and Francesco Di Carlo and Silvia Olivotto as substitute Auditors. The members of the Board of Statutory Auditors declared that they met the conditions of professionalism, good standing and independence.

Transformational asset management strategy for Generali in Europe

On 11 May Generali announced the new strategy for its asset management unit addressing the needs of insurance companies and individuals in a low interest rate environment and supporting Generali’s shift towards a greater contribution from fee-based business. The new asset management strategy is based on two pillars: broadening the investment capabilities and offering bespoke investment solutions to European companies and individual savings products. Asset management unit will broaden investment capabilities and enlarge product offering to reach €500bn of assets under management by 2020.

Granier new CEO of Generali France

Jean-Laurent Granier joined Generali Group as Country manager for France and Président Directeur Général (PDG) of Generali France. Furthermore, Jean-Laurent Granier joined the Group Management Committee.

Intesa San Paolo

On 30 May Assicurazioni Generali sold 510 million ordinary shares of Intesa Sanpaolo, amounting to 3.04% of the share capital, and started the process to terminate the previously disclosed securities lending transaction. At the same time, Generali ended the collateralized derivative transaction, settled on 17 February 2017, in order to fully hedge the economic risk related to the acquisition of these shares. Generali Group maintains a marginal exposure to Intesa Sanpaolo shares as an ordinary financial investment.

New catastrophe bond issued by Generali

Generali returns to the ILS market with a €200 million cat bond on floods and windstorms in Europe and earthquakes in Italy, through a reinsurance agreement with Lion II Re DAC, an Irish special purpose company, providing per occurrence cover in respect the mentioned events over a four year period. The Lion II Re transaction transfers part of these risk to the bond investors allowing for a more optimized protection for the Group against catastrophes.

Footprint optimization

On 19 July Generali has agreed to the disposal of its participation in the Colombian companies, equivalent to 91.3% of Generali Seguros and to 93.3% of Generali Vida, to the Talanx Group. Furthermore Generali also completed the sale of its stake in its Guatemala-based subsidiary to the Neutze family.

Outlook

In an improving macroeconomic and financial context, but still characterized by low interest rates and uncertainty on financial markets, the disciplined strategic plan execution will continue. With reference to rebalancing of the insurance portfolio and to the enhanced of technical capabilities, in the Life segment the Group will continue to foster the offer of policies less sensitive to the level of interest rates and with less capital absorption. In the Property&Casualty segment, that is relevant for the Group strategy to become a leader in the retail segment in Europe, it will continue to focus on the technical profitability, in order to support the performance in a scenario of minor financial earnings. The Group continues to optimise the international footprint, through the aforementioned disposal operations, and to rationalise the operating machine by managing operating expenses. Finally, the strengthening of the brand and innovation initiatives continue in order to retain clients and our distribution network, and to attract new ones.

The above initiatives will enable the Group to counteract and overcome the prolonged scenario of low interest rates and encourage growth, confirming the pre-established objectives of the strategic plan.

The Manager in charge of preparing the company’s financial reports, Luigi Lubelli, declares, pursuant to paragraph 2 article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

ADDITIONAL INFORMATION

For further information please refer to the Interim Condensed Consolidated Financial Statements of the Generali Group.

List of annexes

Group highlights

1) GROUP HIGHLIGHTS

Debt

2) DEBT

Balance sheet

3) BALANCE SHEET

From operating result to net result

4) FROM OPERATING RESULT TO NET RESULT

Additional key data per segment

5) ADDITIONAL KEY DATA PER SEGMENT

LIFE

Operating result by driver

Life segment indicators by country

PROPERTY&CASUALTY

Operating result by driver

Property&Casualty segment indicators by country

Information on significant transactions with related parties

6) INFORMATION ON SIGNIFICANT TRANSACTIONS WITH RELATED PARTIES

With reference to transactions with related parties, in accordance with the provisions of paragraph 18 of the Procedures relating to transactions with related parties approved by the Board of Directors in 2010 and subsequent updates, it should be noted that:

(i) no significant transactions were concluded during the reporting period and

(ii) no transactions with related parties having a material effect on the financial position or results of the Group were concluded.

Further details on related party transactions can be found in the related section of the Consolidated half yearly financial statements.

1Changes in premiums, net cash inflows and Annual Premium Equivalent (APE) and the present value of new business premiums (PVNBP) are presented in equivalent terms (at constant exchange rates and scope of consolidation)

2Preliminary Regulatory Solvency Ratio net of the accrued dividend. Please for definition see Glossary at page 134 of Consolidated Financial half-yearly Report 2017.

3This performance indicator is calculated as the ratio New Business Value (NBV)/ Present Value of New Business Premiums (PVNBP, that replaces the performance indicator APE, in order to provide a better representation of margin on new business volumes). For further information please see Glossary at page 134 of Consolidated Financial half-yearly Report 2017). The technical margin calculated considering APEs would increase up to 40.5%.

4The ratio represents an update with respect to the figure communicated on 16 March 2017 (177%), consistent with the information disclosed to the Supervisory Authority in accordance with the timing provided by the Solvency II regulations and published on 30 June 2017 in the 2016 Report on the solvency and financial position of the Generali Group.

5The “Holding and other activities” segment includes the activities carried out by the Group companies in the financial advisory and savings products sectors (financial segment), the costs incurred from the management, coordination and financing of the business, and other activities that the Group considers subsidiary to its core insurance business.

The Group CEO Philippe Donnet comments 2017 First Half Results