GENERALI GROUP CONSOLIDATED RESULTS AS AT 30 JUNE 2021(1)

03 August 2021 - 07:23 price sensitive

Generali confirms the Group’s excellent profitability, with strong growth in premiums, operating and net results. Extremely solid capital position

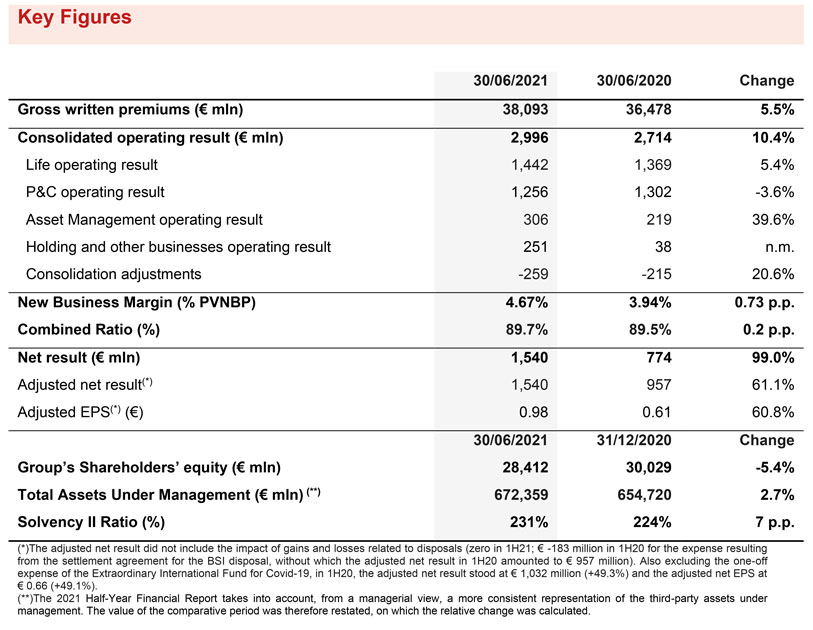

- Operating result rose to € 3 billion (+10.4%), thanks to the positive performance of the Life, Asset Management and Holding and other businesses segments. The excellent contribution from the P&C segment was confirmed

- Gross written premiums increased to € 38 billion (+5.5%), up in both the Life segment (+5.8%) and the P&C segment (+4.9%). Strong Life net inflows at € 6.3 billion (-8.6%)2. The New Business Margin was excellent, and at 4.67%, among the best in the sector (3.94% 1H20). The Combined Ratio was substantially stable at 89.7% (+0.2 p.p.)

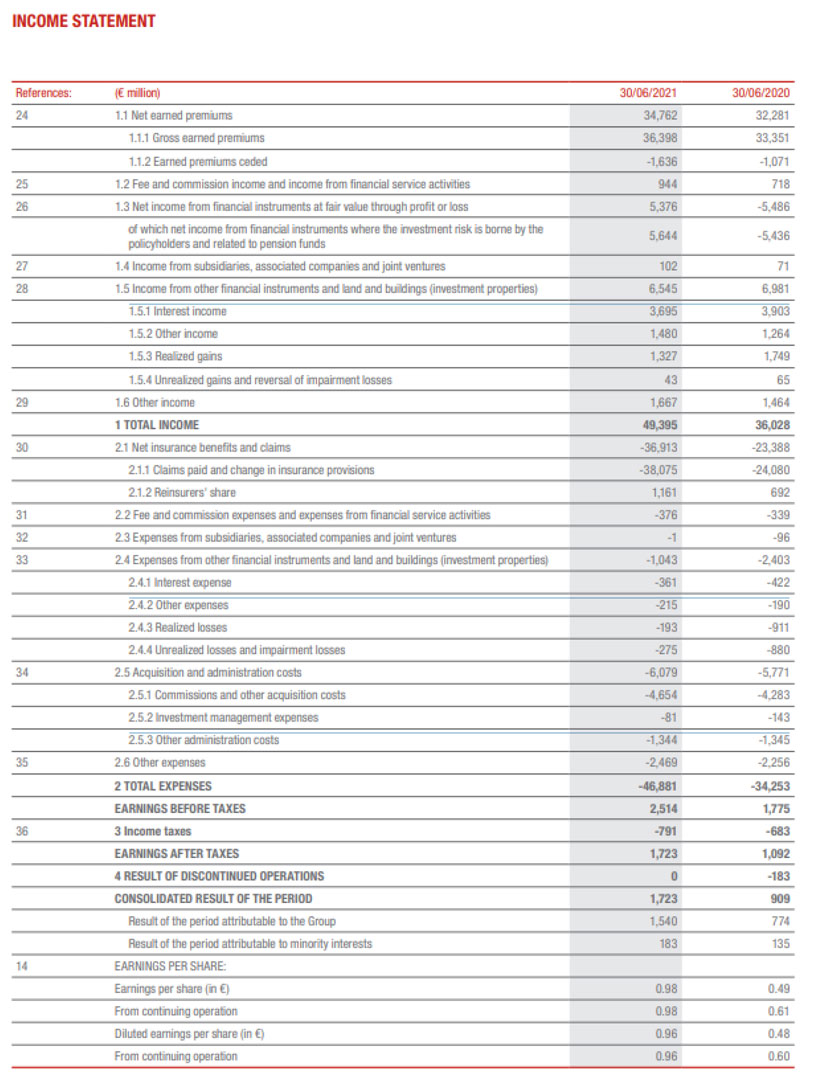

- Strong growth in the net result which rose to € 1,540 million (€ 774 million 1H20)3

- Solvency Ratio was extremely solid at 231% (224% FY2020)

- The Group is fully on track to meet its targets for the year and successfully complete the ‘Generali 2021’ strategic plan

The Generali Group CEO, Philippe Donnet, stated: “Today’s excellent results confirm that we are fully on track to successfully deliver the ambitious targets of the current ‘Generali 2021’ plan, even in this very challenging environment. The significant growth achieved in the first six months of the year strengthens Generali's position as the European leader, thanks to our operational excellence, the acceleration of our digital innovation and the quality of our distribution network. We will continue to forge ahead with an even stronger focus on our Lifetime Partner ambition, leveraging on the enthusiasm, passion and energy of our 72,000 colleagues and 165,000 agents worldwide, and we look forward to presenting the new plan at the Investor Day on December 15th.”

EXECUTIVE SUMMARY

Milan - At a meeting chaired by Gabriele Galateri di Genola, the Assicurazioni Generali Board of Directors approved the 2021 Consolidated Half-Year Financial Report of the Generali Group, expressing its satisfaction for the excellent results achieved in a particularly challenging environment.

The operating result rose to € 2,996 million (+10.4%), benefitting from the positive performance of the Life, Asset Management and Holding and other businesses segments. The contribution of the P&C segment was excellent, despite the impact of several significant natural catastrophe claims in continental Europe.

The Life and P&C segments confirmed excellent technical profitability, demonstrated by the New Business Margin at 4.67% (3.94% 1H20) and a substantially stable Combined Ratio at 89.7% (+0.2 p.p.). The operating result of the Asset Management segment reached € 306 million (+39.6%), mainly boosted by the rise in operating revenues, also supported by the increase in assets under management.

The non-operating result was € -496 million (€ -941 million 1H20). The significant improvement was thanks to the lower impairments on available for sale investments – which were particularly affected in 1H20 by the impact of the pandemic on financial markets – and the increase in the realised gains, mainly deriving from equities and € 67 million for a real estate transaction for the Libeskind Tower in CityLife, Milan. The first half of 2020 was also impacted by the impairment on goodwill related to the Life business in Switzerland for € 93 million, the one-off expense of € 100 million4 for the Extraordinary International Fund for Covid-19 and further local initiatives for € 54 million to face the pandemic. The impact of interest expenses on financial debt further improved, as a result of the debt optimisation strategy.

The net result significantly increased to € 1,540 million (€ 774 million 1H20) driven by the operating result and the non-operating performance, mentioned above.

The gross written premiums increased to € 38,093 million (+5.5%), thanks to positive growth in both business segments.

Life net inflows were strong and stood at € 6.3 billion (-8.6%)5, the decrease was attributable to the savings and pension line, consistent with the Group’s portfolio repositioning strategy. Both the protection (+10.3%) and unit-linked (+0.9%) lines recorded growth.

Life technical provisions grew to € 393.4 billion (+2.3%; +3.4% excluding the effect from the deconsolidation of a pension fund in central and eastern European countries).

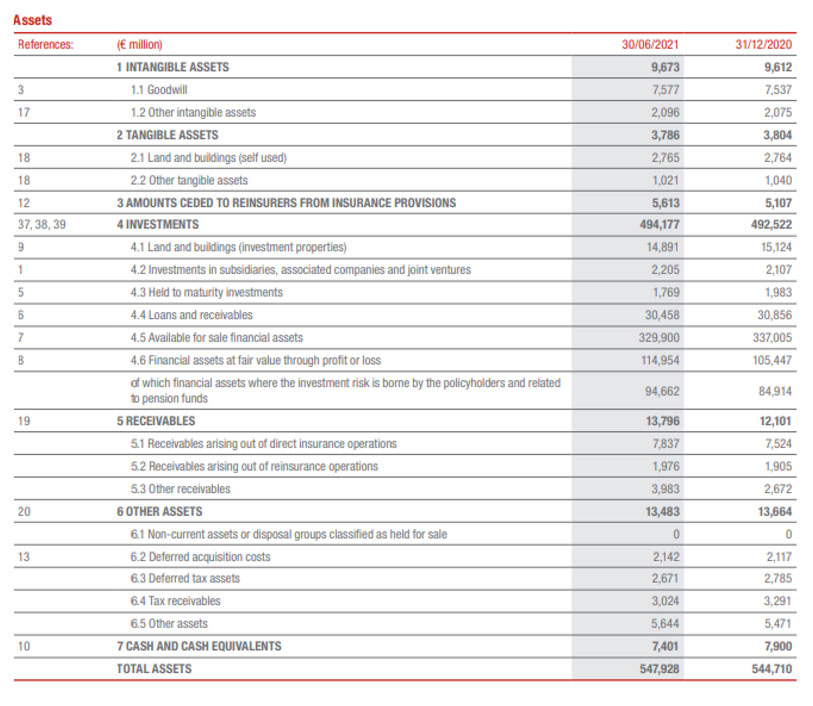

The Group's Total Assets Under Management reached € 672.4 billion, up +2.7% from 31 December 20206.

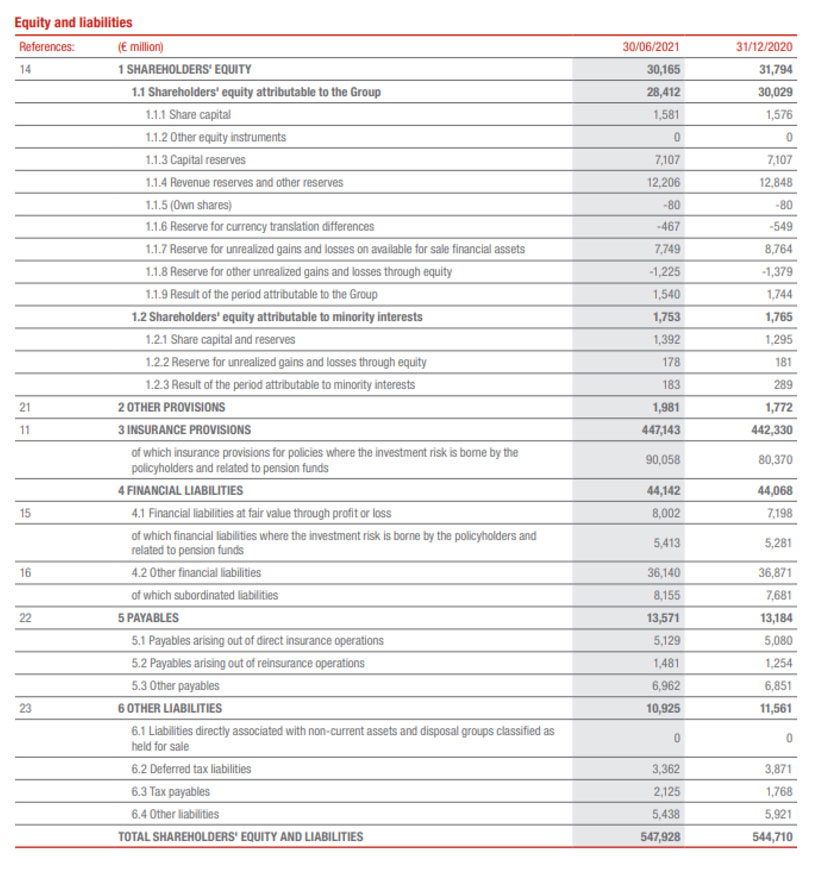

The Group's shareholders' equity was € 28,412 million, -5.4% compared to 31 December 2020. The change was due to a € 1,014 million decrease in the AFS reserves, deriving mainly from the performance of government bonds and the deduction of the entire dividend approved for a total of € 2,315 million, of which € 1,591 million related to the 2020 dividend, paid on 26 May 20217.

The Group confirmed its excellent capital position with the Solvency Ratio at 231% (224% FY2020). The increase of 7 p.p. was mainly attributable to the excellent normalised capital generation, net of the dividend for the period, calculated on a pro rata basis from the previous year’s dividend, and to market variances. These positive trends more than offset the impact of the regulatory changes at the beginning of the year, operating variances (in particular, re-risking) and M&A transactions.

In addition, the Board resolved to launch the preparatory activities of the procedure to define a possible slate of candidates for the Board renewal in 2022: said procedure will be submitted to the next meeting of the Board of Directors on 27 September.

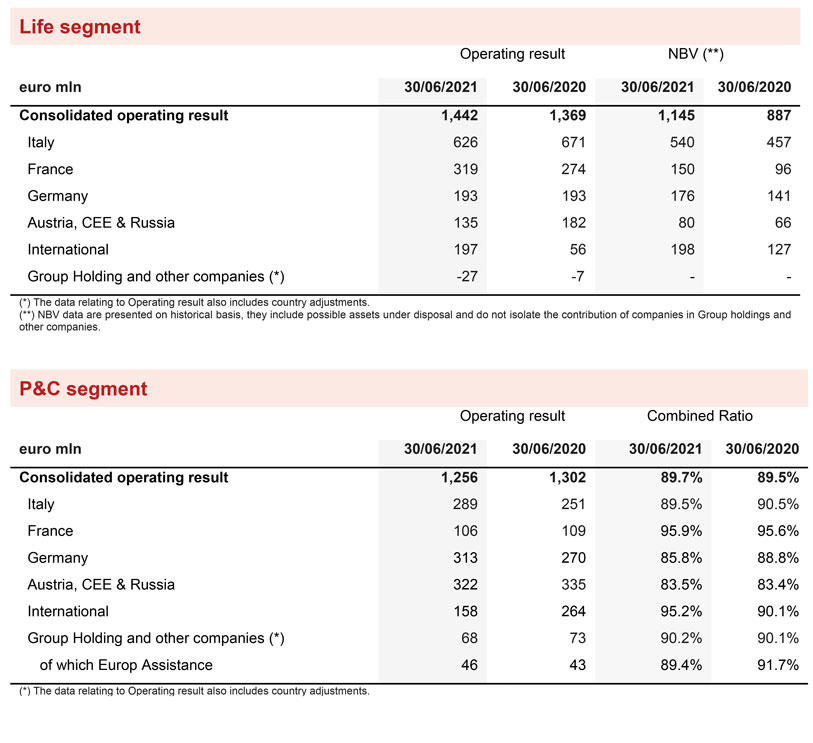

LIFE SEGMENT

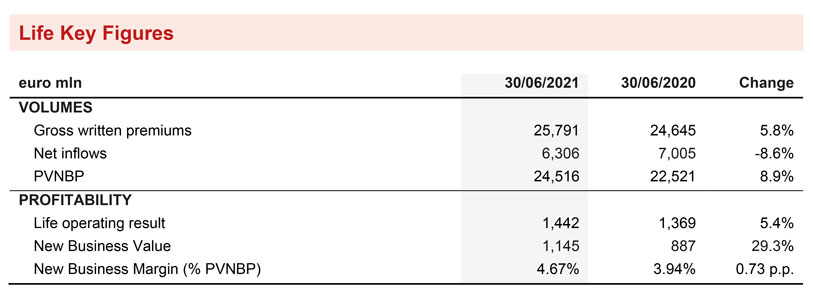

- Gross written premiums grew to € 25,791 million (+5.8%) in particular thanks to the positive performance of the unit-linked and protection lines

- The New Business Margin was confirmed at an excellent level at 4.67% (3.94% 1H20) and the new business value (NBV) grew to € 1,145 million (+29.3%)

- The operating result rose to € 1,442 million (+5.4%)

Gross written premiums in the Life segment grew by 5.8% to € 25,791 million, mainly driven by growth in the unit-linked line (+8.1%), especially in France and to a lesser extent, Germany. The protection line improved by +4%, mainly in Asia and Italy. The savings and pension business also increased (+2%), above all in France. Excluding the written premiums of a collective Life pension fund in Italy, total Life gross written premiums would have increased by 12.7% and unit-linked premiums by 38.4%.

Life net inflows were € 6,306 million (-8.6%). The decrease is attributable to the savings and pension line, consistent with the Group’s portfolio repositioning strategy. Excluding the collective Life pension fund in Italy, mentioned above, Life net inflows would have increased by 16.6%. Life technical provisions grew to € 393.4 billion (+2.3%). Adjusting for the effect from the deconsolidation of a pension fund in central and eastern European countries, growth in the Life technical provisions would have reached 3.4%.

New business in terms of PVNBP (Present value of new business premiums) rose to € 24,516 million (+8.9%;+23% excluding the collective Life pension fund in Italy, mentioned above).

Despite less favourable financial assumptions, the New Business Margin was confirmed among the best in the sector and reached 4.67% (+0.73 p.p.) thanks to the rebalancing of the business mix towards the more profitable lines of business and the continued improvement in the features of new products, particularly in Italy and France. Excluding the collective Life pension fund in Italy, mentioned above, the New Business Margin would have grown 0.46 p.p..

Positive trends in production and profitability enabled the new business value (NBV) to reach € 1,145 million (+29.3%; +36.4% excluding the collective Life pension fund in Italy, mentioned above).

The operating result rose to € 1,442 million (€ 1,369 million 1H20). The net investment result improved compared with 1H20, which was affected by the negative performance of financial markets and the acceleration of the provisions for guarantees to policyholders in Switzerland. The technical margin grew in the first half of the year (+7.5%), thanks to the development of unit-linked and protection products. Operating expenses increased in the acquisition component (+12%). The technical margin, net of expenses, returned to growth in the second quarter, after a decline in the first.

The technical margin was estimated8 to be impacted by € -62 million as a result of the Covid-19 pandemic, in particular for higher claims in the protection line, mainly in ACEER, France, Italy, the Americas and Southern Europe.

P&C SEGMENT

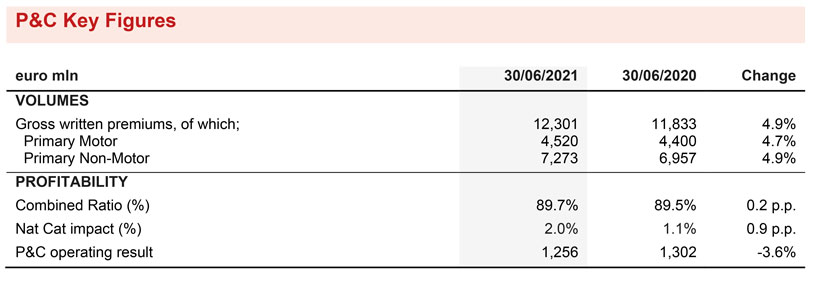

- Premiums rose to € 12,301 million (+4.9%), supported by the development of the motor and non-motor lines

- The Combined Ratio was substantially stable at 89.7% (+0.2 p.p.)

- The operating result was € 1,256 million (-3.6%)

Premiums in the P&C segment increased by 4.9%, on equivalent terms, to € 12,301 million, reflecting the positive development in both the motor line (+4.7%) and non-motor line (+4.9%).

The premiums of Europ Assistance returned to growth (+5.2%), which was mainly affected by the impact of Covid-19 on the travel insurance sector in 1H20.

Positive growth in the motor line was recorded across almost all countries in which the Group operates, in particular ACEER (+6.1%), Italy (+5.5%) and Argentina (+47.1%, also allowing for inflationary adjustments). The non-motor line grew by 4.9% with positive trends in the Group's main countries of operation.

The operating result confirmed its excellent contribution standing at € 1,256 million (-3.6%). The slight decrease was mainly due to the contraction of the investment result (-5.6%) reflecting lower current income, in light of the current environment for interest rates and the devaluation of the Argentinian Peso. The technical result also fell slightly (-1.5%).

The Combined Ratio was substantially stable at 89.7% (+0.2 p.p.), mainly reflecting the significant impact from natural catastrophe claims, which weighed 2.0 p.p. (1.1.p.p. 1H20). In particular, there were € 218 million of natural catastrophe claims (€ 118 million 1H20), including a storm in Spain in January, and subsequently, storms that affected central Europe in June. The improvement in the non-catastrophe current year loss ratio was essentially due to the minor impact from large man-made claims. The contribution from prior years increased slightly and stood at -3.3%. The expense ratio stood at 28.5% (+0.6 p.p.), growing especially in the acquisition component (+0.9 p.p.) which mainly reflected the evolution in the motor line, as a result of the growth in higher commission coverage, in particular in Italy, and the increase in expenses resulting from the development and support of business in ACEER.

The Group estimated9 its Combined Ratio excluding Covid-19 impacts to be 91.2%.

ASSET MANAGEMENT SEGMENT

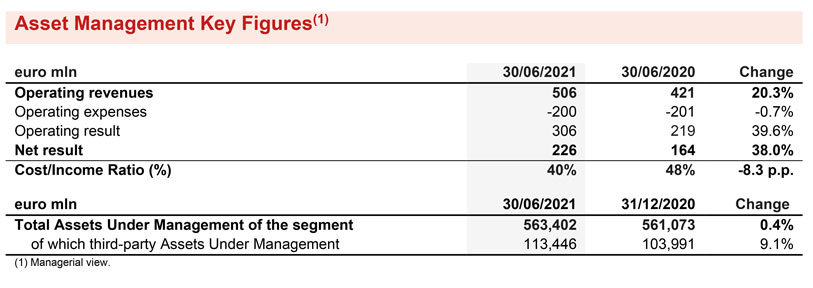

- The operating result of the segment rose to € 306 million (+39.6%)

- The net result of the segment was € 226 million (+38%)

The operating result of the Asset Management segment reached € 306 million (+39.6%), boosted mainly by the increase in operating revenues of € 506 million (+20.3%) supported also by the overall increase in assets under management.

Performance fees reached € 19 million (+52.6%) and operating expenses were essentially stable. The

contribution of external clients was 31% of total revenues, a slight decrease compared to 1H20.

The net result of the Asset Management segment grew to € 226 million (+38%).

Third-party Assets Under Management rose to € 113.4 billion (€ 104.0 billion at 31 December 2020) of which € 7.8 billion derived from the agreements entered into with Cattolica Assicurazioni in 2020, thanks to € 8.6 billion in net inflows and the positive performance of financial markets.

The value of the Total Assets Under Management of the segment was € 563.4 billion as of 30 June 2021.

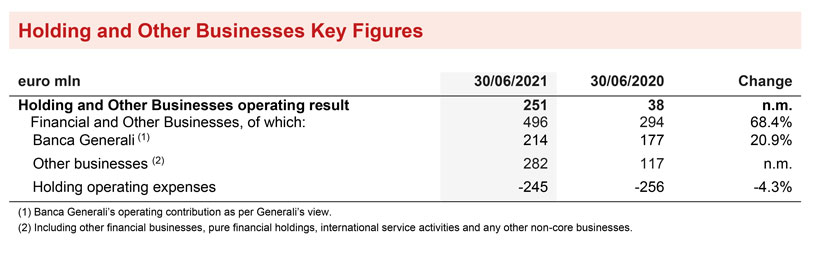

HOLDING AND OTHER BUSINESSES SEGMENT

- The operating result of the segment reached € 251 million

- Banca Generali and private equity continued to provide significant contributions

The operating result of the Holding and other businesses segment reached € 251 million (€ 38 million 1H20). In particular, Banca Generali's result rose to € 214 million (+20.9%), also thanks to the development of performance fees, which was partially offset by the provision of € 80 million10 in the second quarter, in order to protect customers.

Other businesses in the segment also provided a positive contribution, thanks to the excellent results of private equity.

Holding operating expenses stood at € -245 million (€ -256 million 1H20) reflecting the reduction in expenses, concentrated in the second quarter of the year.

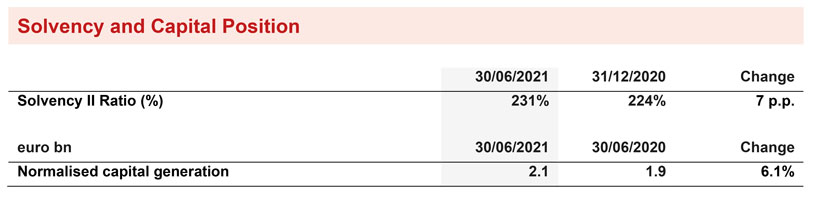

BALANCE SHEET AND CAPITAL POSITION

- Extremely solid capital position with the Solvency Ratio at 231% (224% FY2020)

- Strong normalised capital generation stood at € 2.1 billion (+6.1%)

The Solvency Ratio was extremely solid at 231% (224% FY2020). The increase of 7 p.p. was mainly attributable to the excellent normalised capital generation (+11 p.p.), supported by the value of new business in Life and P&C underwriting profitability, and to market variances (+9 p.p.), favoured by the recovery of interest rates, the positive performance of the equity sector and the narrowing of the spread on government bonds (only partially reduced during the second quarter). These positive effects more than offset the impact of regulatory changes that took place at the beginning of the year (-4 p.p.; linked to EIOPA changes on the Ultimate Forward Rate and the reference portfolio), operating variances (in particular, re-risking), M&A transactions (linked to the acquisition in Greece) and capital movements (-4 p.p.; relating to the dividend for the period, calculated on a pro rata basis compared to the dividend relating to the 2020 results).

The normalised capital generation was € 2.1 billion (+6.1%).

NEW STRATEGY FOR CLIMATE PROTECTION

In June 2021, Generali announced its new strategy for climate protection which updates and extends the Group’s existing plan approved in February 2018 with more ambitious targets. The strategy pledges significant action related to investment and underwriting activities, the Group's core businesses, committing to a low climate impact future. The new objectives include:

- € 8.5-9.5 billion of new green and sustainable investments in the period 2021-2025;

- Definition of a roadmap for the complete exclusion of investments and underwriting activities in the thermal coal sector in OECD countries and in the rest of the world;

- Gradual decarbonisation of the direct investment portfolio to become climate neutral by 2050.

OUTLOOK

Even though there continues to be uncertainty as to the development of further variants of COVID-19 as the year progresses, the current scenario, thanks to extensive vaccinations, foresees a recovery of the global economy in 2021, sustained by expansive monetary and fiscal policies, which will have a positive impact on the insurance sector as a whole.

In this context, the Group confirms and continues with its strategy to rebalance the Life portfolio in order to further increase its profitability and with a more efficient capital allocation. In the P&C segment, Generali's objective in the mature insurance markets in which the Group operates is to maintain the positive trend of premiums accompanied by excellent profitability, despite the impact of natural catastrophe claims in July in continental Europe and, at the same time, to gain ground in high potential markets, by expanding its presence and offer.

With regard to the Asset Management segment, actions will continue in 2021 to develop expansion into private equity and real assets, where Generali can leverage its capacity and commitment to sustaining the economic recovery, which will be accompanied by an extension of the product catalogue in terms of high convictions and multi-asset products for customers and partners, and of distribution capacity.

By leveraging all of these initiatives and in light of the results achieved in the first half of 2021, the Group confirms its target of annual compound growth in 2018-2021 of earnings per share of between 6% and 8%. In addition, the 2021 RoE is expected to be higher than 11.5%, with a cumulative dividend target for 2019-2021 of between € 4.5-5 billion, subject to the regulatory context.

SIGNIFICANT EVENTS OF 2021

Significant events that occurred following the end of the period are available in the 2021 Consolidated Half- Year Financial Report. The Report also contains the Glossary.

Q&A CONFERENCE CALL

The Group CEO, Philippe Donnet and Group CFO, Cristiano Borean, will participate to the Q&A session conference call for the consolidated results of the Generali Group as of 30 June 2021, which will be held on 3 August 2021, at 12.00 pm. CEST.

To follow the conference call, in a listen only mode, please dial +39 02 802 09 27.

The Manager in charge of preparing the company’s financial reports, Cristiano Borean, declares, pursuant to paragraph 2, article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

FURTHER INFORMATION BY SEGMENT

GROUP’S BALANCE SHEET AND INCOME STATEMENT11

1Changes in premiums, Life net inflows and new business premiums were presented in equivalent terms (at constant exchange rates and consolidation scope). The operating result, own investments and Life technical provisions excluded any assets disposed of during the same period of comparison.

2In June 2020, Generali won the mandate in Italy for the management of two investment segments of Cometa, the National Supplementary Pension Fund for workers in the engineering industry, the installation of industrial plants and similar sectors and for employees in the goldsmith and silversmith sector. Excluding the effect of this pension fund, Life net inflows would have increased by 16.6%.

3The adjusted net result - defined as the net result without the impact of gains and losses related to disposals - is equal to the net result of the period, which was not impacted by gains and losses related to disposals. The 1H20 adjusted net result amounted to € 957 million, which neutralised € 183 million resulting from the settlement agreement for the sale of BSI. In addition, excluding the one-off expense of the Extraordinary International Fund for Covid-19, the 1H20 adjusted net profit amounted to € 1,032 million.

4This amount, net of taxes, was € 75 million.

5Excluding the effect of the collective Life pension fund in Italy, Life net inflows would have increased by 16.6%.

6The 2021 Half-Year Financial Report takes into account, from a managerial view, a more consistent representation of the third-party assets under management. The value of the comparative period was therefore restated, on which the relative change was calculated.

7The second tranche, equal to € 0.46, will be payable as of 20 October 2021 and the shares will be traded ex-dividend as of 18 October 2021: such second tranche will be payable subject to the verification by the Board of Directors of the absence of impeding supervisory provisions or recommendations in force at that time.

8For more information on the methods used to determine the quantitative impacts, see the section ‘Disclosure on the quantitative impacts of Covid-19 on the Group’ in the Annual Integrated Report and Consolidated Financial Statements 2020.

9For more information on the methods used to determine the quantitative impacts, see the section ‘Disclosure on the quantitative impacts of Covid-19 on the Group’ in the Annual Integrated Report and Consolidated Financial Statements 2020.

10This amount, net of taxes and minorities, is equal to € 28 million.

11With regard to the financial statements envisaged by law, note that the statutory audit on the data has not been completed. The Group will publish the final version of the Consolidated Half-Yearly Financial Report 2021 in accordance with prevailing law, also including the Independent Auditor’s Report.