The Emerging Paradox

By Vincent Chaigneau, Head of Research, Generali Investments

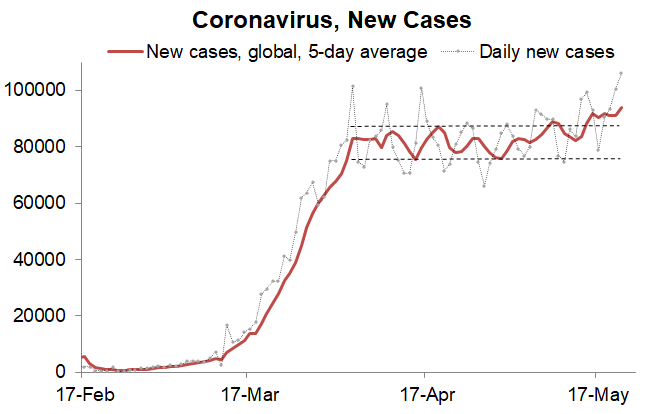

Reopening for business. The easing of the lockdowns is proceeding slowly but smoothly so far. Or is it? The western world has not suffered another wave of Covid-19 contagion. But globally new cases surged just over 100k per day on 20 and 21 May (see chart), as Emerging Market (EM) economies such as Russia, India, Brazil or Mexico have also eased restrictions despite their struggle to contain the pandemic.

Still, financial markets have celebrated the slow reopening of the world economy: after weeks of trading in a range, selected equity indices (e.g. MSCI World) reached new post-crisis highs, before US-China tensions tamed the bullish mood at the end of the week. Importantly, investor surveys show that cash is still very popular, while both sentiment and asset allocations remain rather defensive. In this context global markets are climbing the ‘wall of worry’: for many investors, the pain trade remains a continued risk rally despite an extremely challenging economic environment.

We see three main news behind this tentative upside break:

- Hopes that a vaccine will be available by the turn of the year. This defies all usual practice and would be a tremendous achievement, though not a risk-free one. This animated NYT graphics shows how much the timeline would need to be condensed for a virus to be on the market so quickly. On 18 May equity markets rallied as Moderna advertised promising early results on its Phase 1 trial: the vaccine, even in small doses, seems to be generating an immune response. Health news website STAT however poured cold water on this communication, rightly so given the very small size of the sample (45 subjects, of which eight results were available) and the lack of scientific details. A competing vaccine research program from Oxford University and AstraZeneca, also in the early stage of human trial, is making headlines. Our base case remains that a vaccine will not be available by the turn of the year, notwithstanding the strong political pressure. The main risk remains that a second wave will hit the world in the autumn, which governments need to prepare for and eventually manage without full lockdowns.

- Promises of further policy support. “We’re not out of ammunition by a long shot… So there’s a lot more we can do to support the economy, and we’re committed to doing everything we can as long as we need to,” Fed’s Powell said. Treasury secretary Mnuchin also reminded that so far the government had committed just $195bn in credit support, which serves as capital that the Fed can leverage through its many lending programs; so $259bn of the $454bn plan have yet to be rolled out. The Fed has plenty of QE room indeed. The FOMC Minutes on 20 May also suggested that the Fed will soon reinforce its forward guidance, basically promising to keep Fed Fund rates near zero for a very long time. This may come at the next FOMC meeting, on 10 June.

- A joint German-French statement pushing for a €500bn European Recovery Fund. The details are encouraging.

First, the Fund would provide EU budgetary expenditure for the most affected sectors and regions, in line with European priorities. So they are talking about grants, i.e. fiscal transfers, rather than loans.

Second, the initiative calls for a binding repayment plan, which would mobilise EU financial resources. Of course it is not perfect: the headline number is at the bottom end (about 4% of GDP) of the range considered earlier; also the plan is considered as ‘extraordinary’, not the start of a permanent initiative. But it is still a welcome solidarity effort, which adds up to the less convincing ESM initiatives (up to €240bn, or 2% of GDP, consisting in loans).

The sovereign spread complex reacted positively, with the 10-year BTP-Bund spread down 25-30bp over the past week to around 210bp. Next step: the European Commission is due to present its detailed Recovery Fund proposal on May 27.

It remains to be seen whether the ‘frugal four’ (Austria, Netherlands, Denmark, Sweden) and the ‘Visegrad Four’ (Poland, Slovakia, the Czech Republic and Hungary) can be convinced to sign on the plan.

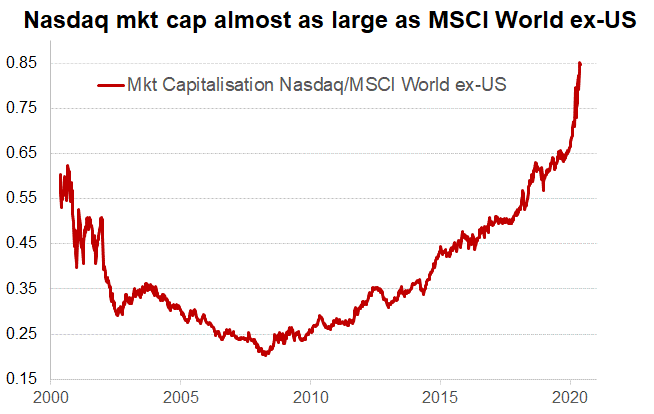

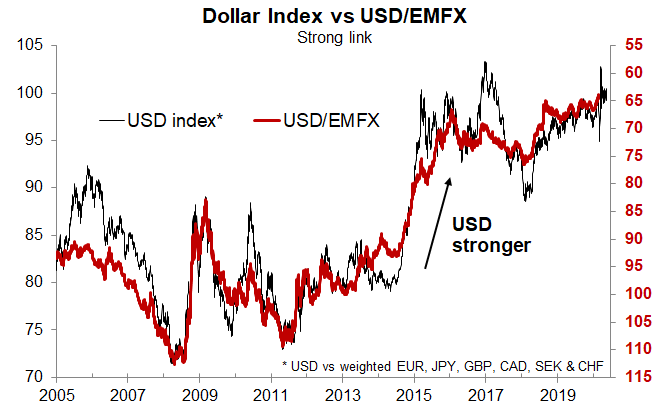

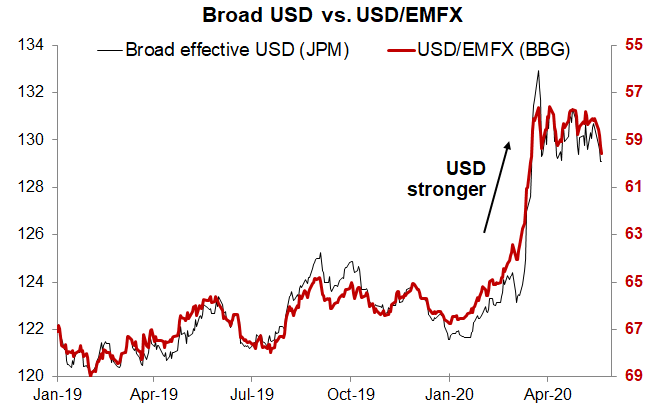

King dollar showing signs of fatigue? The US dollar is a key piece of the global financial puzzle, and often a barometer of investor sentiment. The USD strengthened sharply as risk aversion surged and dollar liquidity became scarce in the three weeks to 24 March (peak of market stress): on a trade-weighted basis the USD was then up almost 10% year-to-date. The currency has also benefited from the superiority of the US equity market, particularly in such deep economic recession: it is heavier in ‘growth’ stocks – technology in particular.

The market capitalisation of the Nasdaq is now just 15% short of that of the entire MSC World index, ex-US (see chart above); dollar strength itself has contributed to the surge of the ratio.

Since late March, however, the USD has seesawed, with a small downside bias. Will the Fed’s dovish forward guidance eventually take its toll on the USD? Possibly, and more so if Europe delivers on its Recovery Fund.

The emerging paradox. The green shoots in global markets have finally reached the shores of the EM currency market. EM assets overall tend to be very cyclical, given their exposure to global growth; they have thus been under pressure as the global economy crashed. Among EM assets (equities, Bonds, FX), currencies have been an easy target through this crisis:

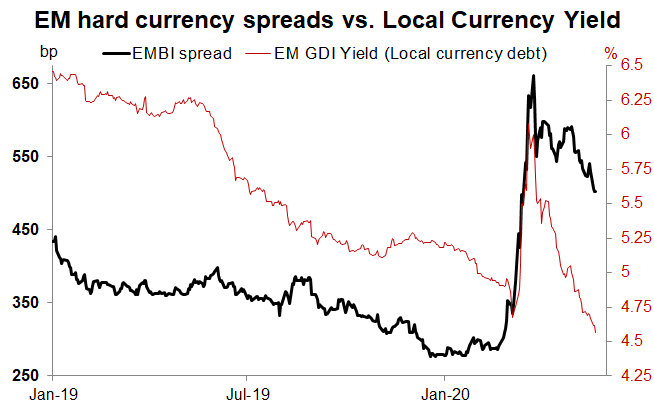

- First, most EM central banks have chosen to cut rates or even start QE, despite the pressure on their currencies. Low inflation indeed has allowed them focus on growth. Thanks to this policy easing, local rates have been falling: in contrast to hard-currency sovereign spreads (EMBI), which have only started to retreat, local rates are now on average below the levels seen before the crisis (left chart below).

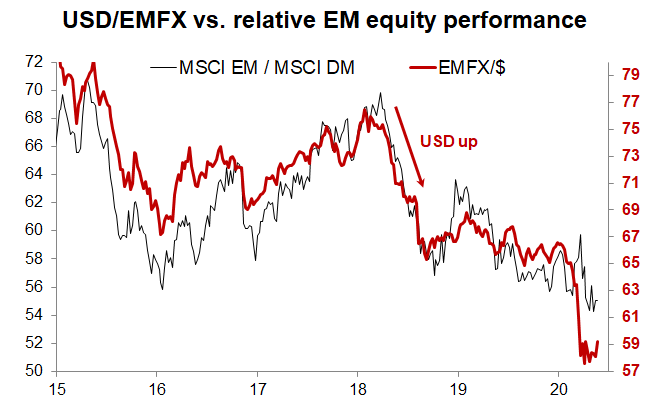

Such policy bias also explains that EM equities, at least on a relative basis vs. developed markets, have offered more resilience than currencies (right-hand chart).

- Second, although national situations differ (net exporters vs. importers), as a group EM currencies tend to be positively correlated to commodity prices, which crashed (especially oil prices).

- Third, EM currencies are very sensitive to global USD trends (see two charts below); hence the sharp EM currency sell-off in March. The Brazilian real BRL, South African Rand (ZAR) and Mexican peso (MXN) are still down respectively 28%, 20% and 17% year-to-date.

Following the March debacle, EM currencies as a group (e.g. JPM EM Currency Index, EMCI) have been in a tight range, failing to benefit from the broad recovery in risky assets. With the US dollar starting to pull back and commodity prices rebounding, however, they are now awakening and tentatively breaking the range to the upside. Paradoxically, this is happening right as Covid-19 is impacting the emerging world more severely and President Trump is toughening up his stance against China again (Huawei restrictions, potential legislation barring many Chinese companies from listing their shares on US stock exchanges, Hong Kong tensions as China introduces national security legislation, Covid accusations). The bounce has been led by the same high-beta currencies (ZAR, BRL and MXN up about 5% vs USD this week).

Conclusion: A few days do not make a trend; given our cautious views about the economic recovery (see last week’s commentary), we deem it premature to switch towards highly cyclical assets. Our moderately pro-risk stance remains biased towards defensive risk assets that are best positioned to benefit in an environment dominated by a limited appetite for risk and massive liquidity injections.

That said the development of the past week deserves attention: a continuation of the dollar pullback and EM currency bounce would signal rising optimism about the global cycle. For now our cautious pro-risk stance also applies to our approach to EM investment. EM countries as a group do not exhibit the same weakness as before previous crises (collectively improved current position, cheaper currency valuation) but individual situations differ. In equities we prefer countries with decent valuation and better resilience to Covid-19, such as South Korea and Taiwan. Resilience to the de-globalisation risk is also an important factor, and we see CEE countries relatively well positioned there.

In Hard Currency debt, where EM sovereign issuers have been very active recently in the EUR primary market, spreads were initially slow (relative to developed corporate bond spreads) to correct from the late March peak. But they have caught up recently, and lost in the process some of their Relative Value appeal. We are particularly cautious with a number of issuers in the BBB rating bucket that face a serious risk of being downgraded to High Yield (the likes of Mexico, Croatia or Romania).