Pause for (sobering) thought

By Vincent Chaigneau, Head of Research, Generali Investments

It Ain’t Over Till It’s Over. The coronavirus contagion continues to slow, but it is not a straight line to zero. In the two weeks to 10 April, the daily growth in the total number of recorded cases globally had slowed linearly from about 12% to 6%. But over the past week that pace has lost just over one point (now below 5%).

Unfortunately the decline towards 0% is likely to be asymptotic. And until the number of new cases falls to a very low level, it will be hard to ease the lockdowns measures. The risk indeed is that a second wave of infections would cause more deaths and force society back into severe lockdown.

A few countries managed the pandemic with a different strategy, relying on strict social distancing measures and ample testing (Singapore, Taiwan and South Korea). That worked, but Singapore has seen a new wave if infection recently, forcing the government to impose a lockdown since 7 April.

Japan, which currently has the fastest pace of contagion, is another matter of concern. The lesson is that any return to social and economic normality will be very progressive, and include social distancing measures and ample testing- if and when enough kits can be made available.

For now lockdown are being extended, e.g. for another three weeks in the UK and France (11 May).

Even in the US, where President Trump is very eager to kick start the economy again, the plan to ease lockdown measures is fairly cautious, leaving much responsibility to governors and setting a number of markers for the three-step easing to be rolled out.

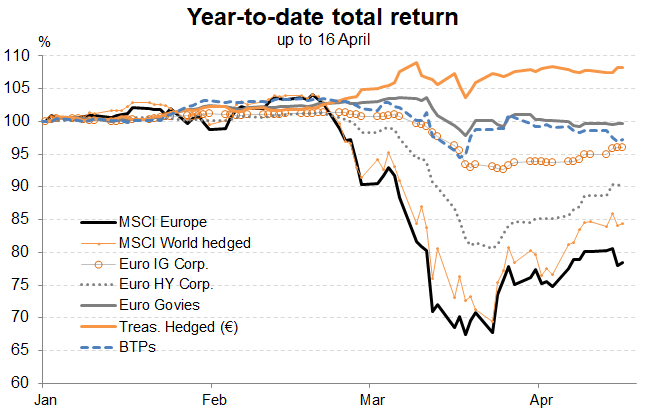

Medical breakthrough? Financial markets have shown clear signs of soothing since late March (see first chart), thanks to the slower coronavirus contagion and a powerful global economic policy response.

Investors had rushed to safety in March but have recently started to put their massive pile of cash back to work again: over the past week global equity and bond funds have seen substantial inflows. Financial markets paused for thought in mid-April, until hopes of a medical breakthrough pushed risk assets higher again on Friday 17 April.

The health care media STAT published a report about patients in a Chicago hospital responding positively to a Gilead treatment. The company urged caution. “The totality of the data need to be analysed in order to draw any conclusions from the trial. Anecdotal reports, while encouraging, do not provide the statistical power necessary to determine the safety and efficacy profile of remdesivir as a treatment for Covid-19.” Gilead expects to get a more complete set of results by the end of April. The trial for the most seriously ill patients does not include a control group (being ‘treated’ with a placebo).

Longer lockdowns = deeper recession. Each month of severe lockdowns probably takes nearly 3 points of annual growth GDP growth. So our forecast of a 1% decline in world GDP this year needs to be revised down. The IMF this week released its World Economic Outlook, predicting a 3% fall in global GDP.

The risks are to the downside. China released its Q1 GDP numbers, showing a 9.8% drop over the quarter, or -6.8% vs Q1 2019. This is bad, but the Q2 numbers for the western economies are likely to be worse. US retail sales and housing numbers for March were ugly, yet they didn’t capture the full extent of the economic damages caused by the lockdown.

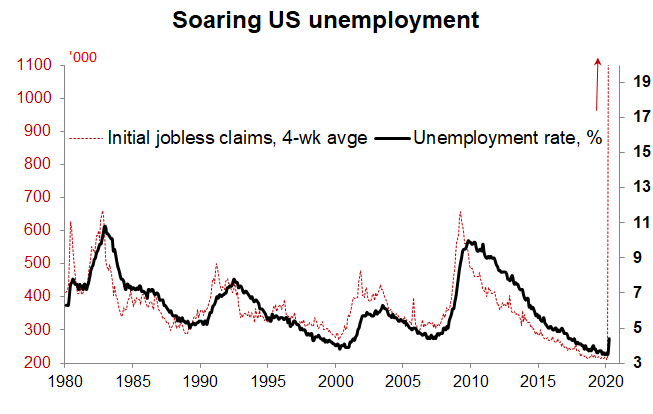

Over the past four weeks, 22 million Americans have asked for jobless claims; this means the unemployment rate is likely to surge to 17% very quickly (Chart 2).

Hopefully many people will get back into the job after the lockdowns end, but expect the healing process to be slow. Such ‘sudden stop’ of the economy – effectively the worst since the great depression by many measures – inevitably creates chain effects that make the recovery slower; one does not go out for a jogging right after a cardiac arrest. In the IMF’s baseline scenario, by end 2021 the advanced economies’ GDP will still be short of the pre-crisis level.

The chain effects include more cautious behaviours from consumers and corporations. The US households’ savings rate went up from 4% of disposable income before the Great Financial Crisis (GFC, 2008-09) to about 8% in the aftermath. Expect it to go even higher after the Global Covid Crisis (GCC); this will imply softer consumer trends.

Corporations have also seen their treasury and balance sheet positions deteriorate, which will undermine capital expenditures (capex). Policy intervention has focused on keeping businesses alive, but baring substantial debt forgiveness, many corporations will still end up with a much weaker financial position. Questions about debt sustainability will also limit the governments’ firepower next year, following the huge spending of 2020.

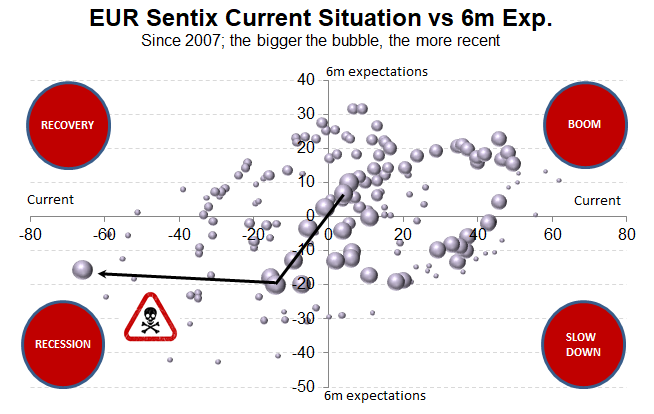

Conclusion. A medical breakthrough would accelerate the return to social and economic normality. Hopes are rising, but the jury is still out. In the meantime, investors need to digest the horrendous short-term economic dive, and the chain effects that will prevent a V-shape recovery. Some may be complacent; e.g. surveys show that most realise the depth of the near-term recession, but -6month expectations are very far from the record lows of previous crises (Chart 3).

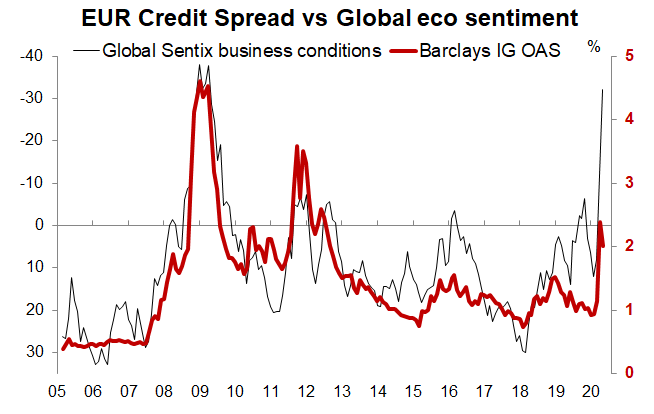

While we still find that risky assets offer value in the longer term, our preference for now still goes for a cautious re-risking of portfolios. We prefer defensive sectors and stocks, as well as safer credits, as heavy policy intervention and central bank buying help contain spread widening (Chart 4).

Credits: Generali Insurance Asset Management S.p.A. Società di gestione del risparmio, 17 aprile 2020