10 February 2021

Choppy, not murky

Generali Investments’ Market Perspectives

- A prospective economic boom into spring/summer, the clearing of tail risks and an impending US fiscal stimulus still bode well for risky assets.

- Yet with parts of the markets looking frothy, correction risks require more vigilance. Elevated Covid-19 cases in Europe and tighter lockdowns on new mutations may test investors’ recovery hopes. A looming spike in US inflation may test central banks’ yield curve control and valuations alike.

- We retain our pro-risk tilt, but slightly trim Credit and Equity overweights. Setbacks may offer buying opportunities into the spring economic acceleration.

Author: Thomas Hempell, Head of Macro & Market Research, Generali Investments

Our increased preference for risk assets, even after the November rally, has paid out well, with the MSCI World up another almost 5%. Emboldened by the rollout of vaccines and a nearing economic rebound, investors have kept looking through rising Covid-19 numbers and bouncing US yields. The clearance of tail risks has played its part. The last-minute UK/EU trade deal has finally taken a hard Brexit nightmare off investors’ minds and Poland and Hungary dropped opposition to the EU budget and Recovery Fund, avoiding a stalemate. The pre-Christmas US fiscal deal ($900bn) and Georgia-induced “blue wave” (more fiscal support coming) also helped.

Going forward, the prospect of re-opening economies amid progressing vaccination still matters most for risk sentiment. US Congress will likely water down President Biden’s push for an extra US$ 1.9 trillion stimulus, but this may still prove powerful enough for a >6% rebound of the US economy this year. A strong start into the reporting season and the reassurance by major central banks that they will stick to their highly accommodative policies for longer will continue to underpin risk appetite and the search for yield.

Frothy markets requiring higher vigilance

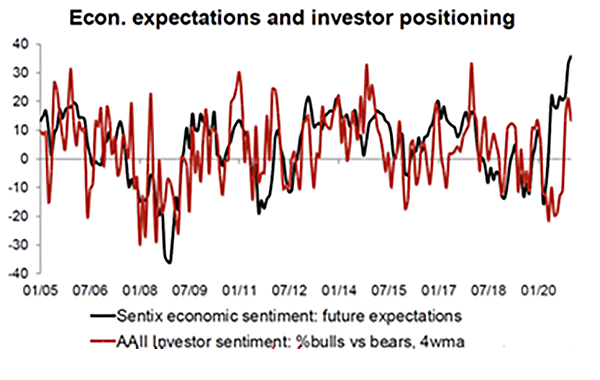

Yet with selected market segments getting frothy and market positions very consensual, higher vigilance is required. First, the rally since November has been fuelled by high recovery hopes (chart). Positions are generally not extreme, but more vulnerable to disappointment if new mutations and a sluggish vaccine rollout in Europe delay the onset of the recovery. Retail buying has contributed to the equity rally, but we find it reassuring that the bullish sentiment (e.g. AAII survey) has flattened out through January. Retail trading (r/WallStreetBets) has pushed selected stocks to crazy levels and caused a pick-up in volatility but we see limited implications for the broader markets insofar Hedge Funds losses and “de-grossing” do not lead to broad deleveraging and capitulation.

Second, while we expect yields to back up only mutedly amid central banks’ de facto yields curve control, risks are tilted towards a stronger bounce. US inflation will rise temporarily into spring mostly on base effects, but also due to fiscal stimulus, pent-up demand and higher commodity prices. Inflation expectations and yields could temporarily overshoot, posing a threat to elevated valuations in many market segments, including Growth and Tech stocks.

Setbacks as buying opportunities

Ultimately, we deem such setbacks as buying opportunities. With vaccination capacities now building rapidly and economies learning to better cope with the virus, the 2021 recovery may be delayed but not derailed. While there are upside risks to US prices, low underlying inflation trends remain the much stronger challenge to central banks in the euro area and most other advanced economies amid wide output gaps and high unemployment. In our tactical positioning, we trim our overweight in Credit and Equities (with a preference for Cyclicals and Value), mirrored by milder underweights in Cash and Core Govies. We still like EM exposure in Equities and Fixed Income, with our focus in the latter on safer higher-yielding issuers that have lagged the recent rally.