Double Materiality Assessment

The double materiality assessment is the strategic process through which Generali Group identifies the material sustainability matters on which it will focus its actions in order to create long-term value while driving a positive impact on people and the planet.

We have conducted a materiality assessment periodically since 2014. Our methodology has been refined over the years to align with the context and regulatory developments.

In 2024, following the entry into force of the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), we developed a new methodological approach based on the concept of double materiality of sustainability matters across the value chain.

Each sustainability matter (e.g. climate change) is assessed both against its positive and negative impacts (impact materiality) and against its risks and opportunities (financial materiality), taking into account each of the four segments of the value chain that the Group has identified in light of its business model and responsible roles: investments, insurance, own operations, and supply chain.

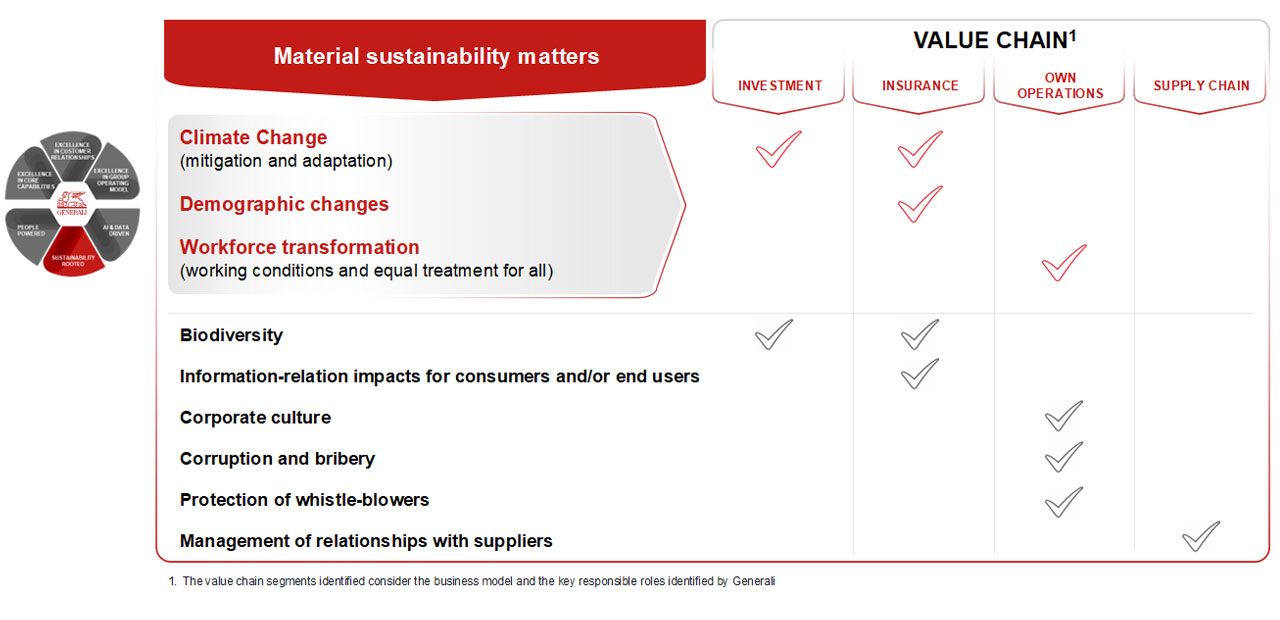

The sustainability matters linked to material impacts, risks, and opportunities identified through the double materiality assessment process represent, on one hand, the basis for the Group Sustainability Statement and, on the other, the input for the Lifetime Partner 27: Driving Excellence sustainability strategy, with reference to three topics which, besides being material, are also strategic: climate change, demographic changes and workforce transformation.

| Strategic Priorities | ESRS Topic/sub-topic | SDGs |

|

Climate change |

E1 – Climate change

|

|

|

Demographic changes |

S4 – Consumers and end-users

|

|

| Workforce transformation |

S1 – Own workforce

|

|

Climate change *

Why it is strategic for Generali: climate change mitigation refers to efforts to reduce or prevent the emission of greenhouse gases in order to limit the increase in global temperature. Since the beginning of the industrial revolution, the global average temperature has increased by 1.47°C compared to pre-industrial levels (1850-1900). This phenomenon is mainly caused by the increase in greenhouse gas concentrations in the atmosphere, resulting from the use of fossil fuels. To avoid the worst effects of climate change, the 2015 Paris Agreement set the goal of limiting the global temperature increase to well below 2°C, with efforts to keep the increase within 1.5°C. For financial companies like the Generali Group, contributing to climate change mitigation becomes an absolute priority, both to reduce the negative impacts caused by their business on the external world and to mitigate the financial risk they face.

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

E1 – Climate change Climate change mitigation |

Investment |

|

| Insurance |

|

Why it is strategic for Generali: climate change adaptation refers to measures taken to protect society and the environment from the negative effects of global warming, such as the increased frequency and severity of extreme weather events. In 2025, estimated global economic losses from natural events were $ 220 billion, of which 51% was uninsured, highlighting the need for adaptation solutions to protect individuals and businesses. It becomes a priority for Generali to contribute to the resilience and adaptation of the communities in which it operates, which increasingly face the consequences of extreme events, as well as to mitigate the financial risk that Generali might suffer as a result of these same events.

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

E1 – Climate change Climate change adaptation |

Investment |

|

| Insurance |

|

Demographic changes *

Why it is strategic for Generali: addressing the growing gaps in healthcare and pension systems becomes a priority, particularly for the insurance sector. This is important both because the business could contribute to increasing social resilience and because addressing the consequences of demographic changes could have a positive impact on communities, as well as represent an opportunity for the Group.

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

S4 – Consumers and end-users Demographic changes |

||

| Insurance |

|

Workforce Transformation *

Why it is strategic for Generali: Generali is a human-centric group and, also with the aim of preserving and strengthening its competitiveness and contributing to a solid sustainability strategy, it considers essential to work on building a resilient workforce that best responds to future challenges, in line with its role as a Responsible employer. To this aim, the Group is committed to further strengthening its distinctive culture, promoting sustainable working practices, and investing in the continuous development of its people. In particular, working on Diversity, Equity and Inclusion (DEI), on Group employees’ well-being and energy, and on the promotion of sustainability has become even more important to further strengthen their engagement. The generational change, together with rapid technological evolution, requires a strategic approach to workforce planning and further evolution of the training offer to maintain or increase the professional relevance of our people in a context of rapid and significant transformation. At the same time, Generali aims to be the employer of choice for top talent, supporting responsible growth in a competitive market. In recent years, the Group has also adopted hybrid work models and witnessed the evolution of own workforce demographics, which include four generations, increasingly oriented to social and environmental aspects.

| ESRS Topic/sub- topic |

Value Chain |

Double materiality assessment output for CSRD purposes |

|

S1 – Own Workforce Working conditions; |

||

| Own operations |

|

Biodiversity

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

E4 – Biodiversity and ecosystems Direct impact drivers of biodiversity loss; |

||

| Investment |

|

|

| Insurance |

|

Information-related impacts for consumers and/or end-users

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

S4 – Consumers and end-users Information-related impacts for |

||

| Insurance |

|

Corporate Culture

| ESRS Topic/sub- topic |

Value Chain |

Double materiality assessment output for CSRD purposes |

|

G1 – Business conduct Corporate culture |

||

| Own operations |

|

Corruption and bribery

| ESRS Topic/sub-topic | Value Chain | Double materiality assessment output for CSRD purposes |

|

G1 – Business conduct Corruption and bribery |

||

| Own operations |

|

Protection of whistle-blowers

| ESRS Topic/sub-topic | Value Chain |

Double materiality assessment output for CSRD purposes |

|

G1 – Business conduct Protection of whistle-blowers |

||

| Own operations |

|

Management of relationships with suppliers

| ESRS Topic/sub- topic |

Value Chain | Double materiality assessment output for CSRD purposes |

|

G1 – Business conduct Management of relationships with suppliers |

||

| Supply chain |

|

* Strategic priority

The identification of material impacts, risks, and opportunities followed a structured process that involved both internal and external stakeholders

Given the relevance of the exercise also in defining the strategic plan, and as outlined in its Sustainability Group Policy, Generali performs a double materiality assessment every three years, whilst carrying out an annual review of the double materiality assessments in the years in between, to ensure that the results remain valid for the current year.

The annual review process includes the assessment, through a dedicated analysis, of the presence of potential significant changes in internal sources (e.g., portfolio composition, risk assessment, policies and procedures) and external sources (e.g., external databases, sector reports and white papers), as well as the presence of any internal factors that could lead to significant changes in Generali's organisational and operational structure (e.g., extraordinary transactions and reorganisations) and external factors (e.g., geopolitical context, regulatory context and market trends) with a potential impact on the Group.

The double materiality assessment process, including the annual review process, consists of the following stages:

1. Pre-assessment

Once the main methodological choices underlying the double materiality assessment had been defined, a preliminary analysis on positive and negative impacts, as well as risks and opportunities is carried out on each sustainability matter under analysis*, for each of the four segments of the value chain.

Where available, Generali relied on internal data and analyses such as climate scenario analysis, operational risk assessments, metrics, and existing targets. In addition, external data and information from data providers, industry studies and market-recognized institutions/associations and expert judgement of key function involved were used.

* For the analysis, the sub-topics related to the 10 topics identified by the ESRS were considered, in addition to further entity-specific topics based on Generali's business, industry trends, and previous materiality assessments carried out by the Group.

2. Feedback collection

The second phase of the process includes the direct engagement of internal and external stakeholders, a crucial step in identifying the impacts, risks and opportunities material to Generali and its value chain.

The results of the pre-assessment phase are shared and validated by internal functions of the Group, as well as by the Sustainability Taskforce to assess their soundness and consistency. Furthermore, in order to gather local perspectives, local sustainability representatives of the Countries in which Generali operates are engaged via a dedicated survey.

In addition to internal stakeholders, the feedback collection phase includes the active engagement of selected external stakeholders, who provide a significant external perspective to integrate material topics into the Group’s business model and strategy. Engagement takes place through individual interviews with the aim of gathering any further feedback and comments.

Once all the feedback received has been collected and consolidated, the final results of the double materiality assessment are shared individually with members of the Top Management (Group Management Committee - GMC) to gather further feedback on the results of the analyses and the strategic implications.

3. Final validation

Both the methodology and the results are formalised and presented to the GMC and the Innovation and Sustainability Committee (ICS) respectively and then submitted to the Board of Directors of the Parent Company for approval.

The results of the double materiality assessment were approved on 20 May 2024 and later confirmed on 19 December 2025.