Consolidated Results as of 31 December 2017 - Press Release (1)

15 March 2018 - 07:30 price sensitive

Operating result hits record high, net profit over € 2.1 billion, dividend rises 6% to € 0.85 per share. Confirming generali strategy fully on track

- Operating result at record of € 4.89 billion (+2.3%) thanks to the Life segment, the Investments, Asset & Wealth Management business and cost reduction target reached ahead of schedule

- Net profit over € 2.1 billion (+1.4%)

- Operating RoE at 13.4%, in line with the strategic plan target (>13%)

- Increase in profitability of life products, with New Business Value (NBV) rising 53.8%. Life net cash inflows at € 9.7 billion, among the highest levels in the European sector. Life technical reserves increased by 4.2%

- Combined Ratio at 92.8%, confirmed as the best among large peers

- The capital position is further strengthened: Regulatory Solvency Ratio at 208%; Economic Solvency Ratio at 230%

- Dividend per share at € 0.85, up 6% (€ 0.80 FY2016)

Generali Group CEO Philippe Donnet declared: “The excellent results that we presented today confirm the validity and effectiveness of our strategic plan in this current market context. We are perfectly positioned to reach all of our objectives that we had set for 2018. In light of these results, the Board of Directors will propose a dividend of 0.85 Euro per share, an increase of 6 per cent from 0.80 Euro in 2016. Our focus on technical excellence, combined with the results of our Investments, Asset & Wealth Management business and the cost reduction target hit two years ahead of schedule, have pushed the operating result to record levels. In 2017, we implemented a series of important projects, such as the launch of the new asset management strategy, the rationalizing of the international footprint and the transformation of our German business - all initiatives that contribute to the overall resilience of our Group. These results, obtained thanks to the daily commitment and passion of our colleagues, agents and collaborators, allow us to look to the future with confidence and to create sustainable value for all of our stakeholders.”

Milan - At a meeting chaired by Gabriele Galateri di Genola, the Assicurazioni Generali Board of Directors approved the consolidated financial statements and the Parent Company’s draft financial statements for the year 2017.

EXECUTIVE SUMMARY

The Group closed the year 2017 with strong results and excellent capital position. In particular, the operating result and net profit both increased. There was improvement of the quality of life net cash inflows and strongly increased new business margins. They confirm the full implementation of the strategy presented in 2016 that will be completed by year-end.

The Group’s operating result reached the record level of € 4,895 million, up 2.3% thanks to the positive performance of the life segment and the Investments, Asset & Wealth Management business2 and to the cost reduction reached two years ahead of schedule (-€200 million in mature markets). The 1.8% increase in the Life result is due to a better investment performance; the growth in the result of the segment Holding and Other Activities, reaching € 59 million, reflects the excellent results of Banca Generali and the enhanced performance of Asset Management Europe. Both segments balance the decrease of the P&C operating result (€ 1,972 million, -4.9%) affected by €416 million in natural catastrophe claims that mainly came from the US hurricanes and the storms that swept Central Europe as well as by the lower contribution of investment returns in a low interest rate context. Excluding the impact of natural catastrophe claims in both years under comparison, the P&C operating result would be stable.

The operating return on equity, the Group’s main economic profitability indicator, came to 13.4% (unchanged compared with the 31 December 2016 figure), confirming the strategic objective (>13%).

Net profit reached € 2,110 million, up 1.4% due to the improvement in the operating and non-operating results that mostly benefit from lower impairment losses and notwithstanding the impact of the discontinued operations and the increase in fiscal obligations.

As for production, the total premiums of the Group were steady at € 68,537 million (-0.2%), with the life segment slightly down at € 47,788 million (-1%) while the P&C segment rose 1.7% to € 20,749 million.

Life net inflows amounted to € 9,718 million, proving to be among the highest levels of the market. The life technical reserves stood at €388.7 billion, up 4.2%. In particular, the unit linked reserves grew by 12.1%.

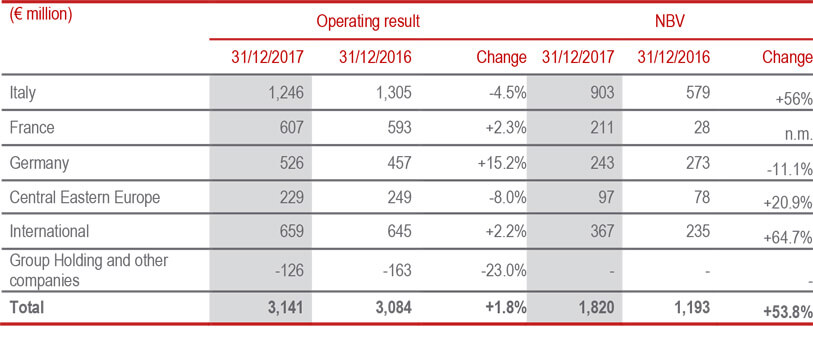

The strategic reorientation toward the unit-linked and pure risk businesses, together with the effective redefinition of the financial guarantees, resulted in significant growth of profitability (margin on PVNBP) of 1.46 p.p., rising to 4.01% (2.56% at 31 December 2016). Also the new business value (NBV) improved consequently (+53.8%), standing at € 1,820 million (€ 1,193 million at 31 December 2016).

Growth in P&C premiums is due to both the motor and non-motor segments.

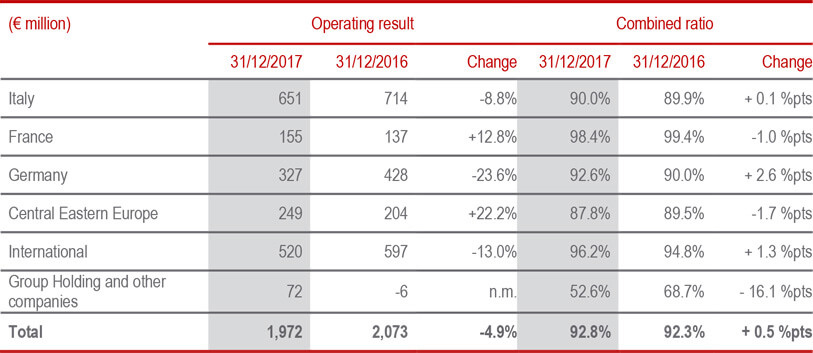

The Combined Ratio, at 92.8% (+0.5%), ranks number one among our large European peers and is consistent with the Group’s proven track record of technical excellence. In particular, not considering the impact of natural catastrophes, the loss ratio – the effect of claims on premiums – improved by 0.6% (62.9% from 63.5% in 2016).

The Regulatory Solvency Ratio – which represents the regulatory view of the Group’s capital and is based on use of the internal model, solely for companies that have obtained the relevant approval from IVASS, and on the Standard Formula for other companies – stood at 208% (178% FY 2016).

The Economic Solvency Ratio of the Group, which represents the economic view of the Group’s capital and is calculated by applying the internal model to the entire Group perimeter, stood at 230% (194% FY 2016).

DIVIDEND PER SHARE

The dividend per share to be proposed at the next Shareholders’ Meeting is €0.85, up by € 5 cents per share (+6%) compared to the previous year (€ 0.80 FY2016). The pay-out ratio is equal to 63%, from 60% in 2016.

The total dividend relating to shares outstanding amounts to €1,330 million. The dividend payment date shall be from May 23 with record date on May 22 and ex-dividend date from May 21.

LIFE SEGMENT

- Operating result up to € 3.1 billion (+1.8%)

- Increased new business value (NBV) to € 1.8 billion (+53.8%) and the new business margin (NBM) +1.46 p.p. thanks to products having better characteristics in terms of return vs. risk

- Net cash inflows at € 9.7 billion

- Premiums at € 47.8 billion (-1%)

- Technical reserves up by 4.2%

The net cash inflows stood at € 9,718 million, one of the highest levels in the market. The trend (-17,1%) reflects in particular the decline registered in Italy (-20.8%) due to payments coming from surrenders and the strategy for rebalancing the portfolio. International declined as well (-57.9%) that takes into account a decline in inflows in Asia and EMEA combined with higher payments. Compared to 2016, the net cash inflows are composed exclusively of unit linked policies and protection while it is negative for traditional savings policies. The life technical reserves stood at €388.7 billion, up 4.2%. In particular, the unit linked reserves grew by 12.1%.

The reorientation toward the unit linked and pure risk businesses, together with the reduction of financial guarantees, resulted in significant margin expansion (margin on PVNBP) of 1.46 p.p., rising to 4.01% (2.56% at 31 December 2016).

New business in terms of present value of new business premiums (PVNBP) amounted to €45,429 million, down by 2.3%, in both the single premium (-2.8%) and the annual premium policies (-2.6%). Unit linked production rose sharply (+28.7%) and the protection line improved slightly (+3%). The traditional savings and pension line premiums posted a significant decrease (-19.0%) due to the Group’s strategic actions aimed at reducing business subject to financial guarantees. As a result of the strategic objectives, the new business value (NBV) improved significantly (+53.8%), standing at € 1,820 million (€1,193 million at 31 December 2016).

Life premiums totalled € 47,788 million (-1%). The performance was consistent with the underwriting policy that led to an increase in unit linked premiums (+22.4%) in particular in Italy (+57.3%) and France (+52.1%). Premiums for protection policies grew 7% reflecting the general increase across the countries where the Group is present.

P&C SEGMENT

- Premiums up to € 20.7 billion (+1.7%)

- Both the motor (+3%) and non-motor (+0.9%) segments improved

- Combined Ratio at 92.8%, best among large peers

Premiums of the P&C segment totalled € 20,749 million, up 1.7% due to the motor segment (+3.0%) driven by Germany (+4.2%), CEE Countries (+3.2%), the Americas (+25.7%), France (+2.6%) and Spain (+3.8%), which more than offset the drop in motor premium income in Italy (-4.5%) where the average premium in the market continues to fall, and measures are being taken by the Group to recover the returns of the portfolio. Also non-motor premium income is up (+0.9%), which mainly benefited from the development in the CEE Countries (+3.6%), in the EMEA region (+2.6%) and by Europ Assistance (+14%). Italy and France fell 1.8% and 2%, respectively, because of the weak market conditions in the corporate and property lines.

The operating result of the P&C was € 1,972 million (€ 2,073 million at 31 December 2016). The decrease (-4.9%) was mostly influenced by the greater impact of natural catastrophe claims, which on the whole affected the year for € 416 million, mainly due to the US hurricanes and the storms that struck Central Europe. Excluding the impact of natural catastrophe claims in both years under comparison, the P&C operating result would be stable.

The Group Combined Ratio stood at 92.8% (+0.5 p.p. compared to 31 December 2016), confirming its leadership position among large European peers. In particular, the loss ratio remained stable. Not considering the impact of natural catastrophes, the loss ratio improved by 0.6% (62.9% from 63.5% in 2016).

HOLDING AND OTHER ACTIVITY SEGMENT (3)

The operating result of the Holding and other businesses segment amounted to € 59 million, considerably up compared to the loss of € 74 million in 2016.

The operating result of the financial and other businesses segment grew to € 513 million (€ 384 million at 31 December 2016). The increase (33.6%) was driven by the performance of the financial segment, particularly the excellent results of Banca Generali, which rose from € 190 million to € 241 million, due to higher performance fees as well as the positive results of the other asset management and real estate companies.

At 31 December 2017, the third party assets managed by the Group companies amounted to €67,474 million (€56,324 million at 31 December 2016), up by 19.8%.

OUTLOOK

In an improving macroeconomic and financial context still characterised by low interest rates and uncertainty in the financial markets, the disciplined execution of the current strategic plan will continue. The Group will continue to rebalance the portfolio in the life segment with the goal of optimising its profitability and allowing capital to be allocated more efficiently through the simplification and innovation of the range of product solutions. Despite the strong competitive pressure in the P&C business, premium income is expected to rise. The above-mentioned initiatives will permit the Group to offset the prolonged low-interest rate scenario and will encourage growth, confirming the objectives set in the strategic plan.

The Manager in charge of preparing the company’s financial reports, Luigi Lubelli, declares, pursuant to paragraph 2 article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

THE GENERALI GROUP

Generali is an independent, Italian Group, with a strong international presence. Established in 1831, it is among the world’s leading insurers and it is present in over 60 countries with total premium income exceeding €68 billion in 2017. With nearly 71,000 employees in the world and 57 million customers, the Group has a leading position in Western Europe and an increasingly significant presence in Central and Eastern Europe as well as in Asia. In 2017, Generali Group was included among the most sustainable companies in the world by the Corporate Knights ranking.

NOTE TO EDITORIAL STAFF

At 7:30 a.m. the following documents will be available on www.generali.com: press release, pre-recorded video with transcription, presentation for analysts, financial statements and other financial documents.

The Analyst Call will take place at 12:00. Journalists may listen in by dialling +39 02 3600 8045 (listen-only mode).

The Generali corporate app offers the most recent institutional information package, which has been optimized for mobile devices. The app may be downloaded free of charge from Apple and Android stores.

1 Changes in premiums, net cash inflows, PVNBP (the present value of new business premiums) and NBV (New Business Value) are presented in equivalent terms, that is at constant exchange rates and scope of consolidation. With reference to the divestment of the Dutch and Irish companies in application of IFRS 5, their value of assets and liabilities, and economic result - net of taxes - were separately entered in the specific items of the financial statements. The 2016 comparative figures were likewise reclassified. For more information, please refer to the paragraph “Change in presentation of the Group performance measures” in the Note to the Management Report.

2 As communicated on 21 February 2018, there is a new geographic segmentation created by three main markets – Italy, France and Germany, and four regional structures (CEE countries, International, Investments, Asset & Wealth Management and Group Holding and other companies).

3 This segment includes the activities of the Group companies in the asset and wealth management sectors, the costs incurred for management and coordination and business financing, and all other operations that the Group considers to be ancillary to the core insurance business.

List of annexes:

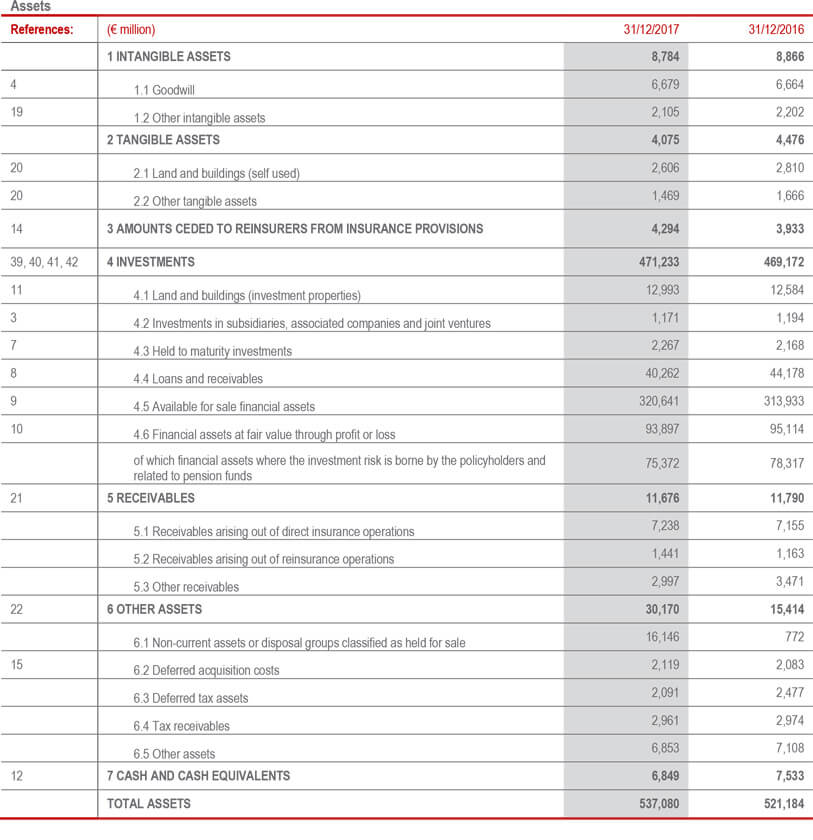

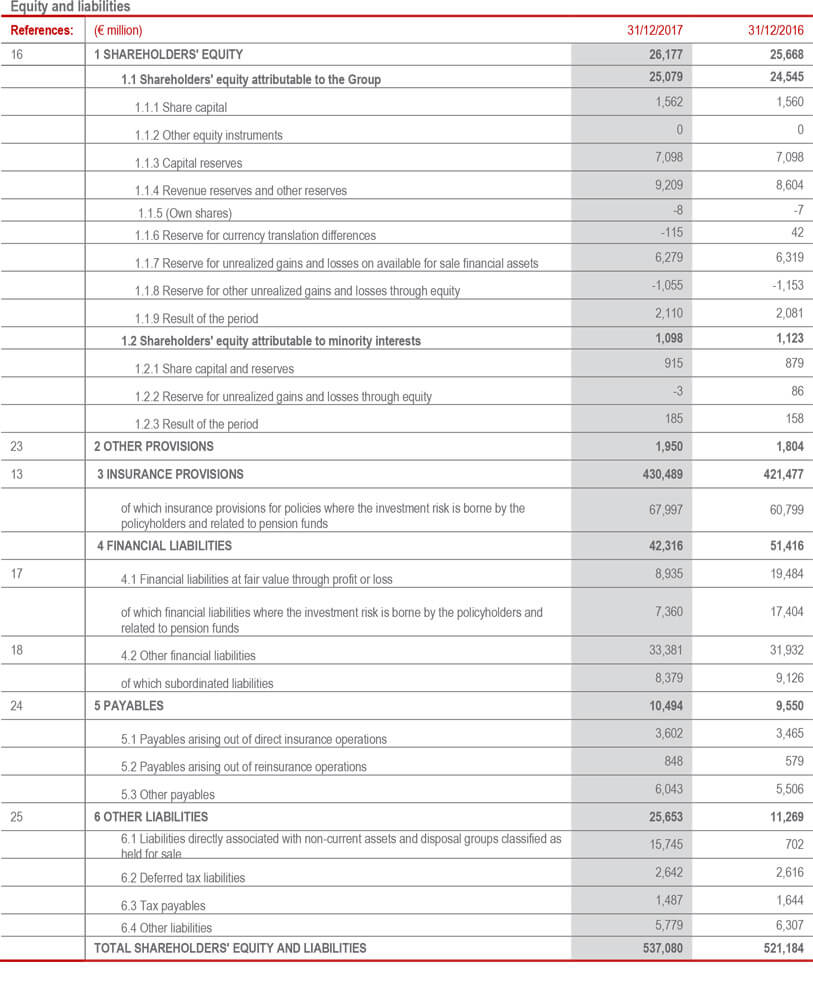

Group balance sheet and income statement

1. GROUP’S BALANCE SHEET AND INCOME STATEMENT

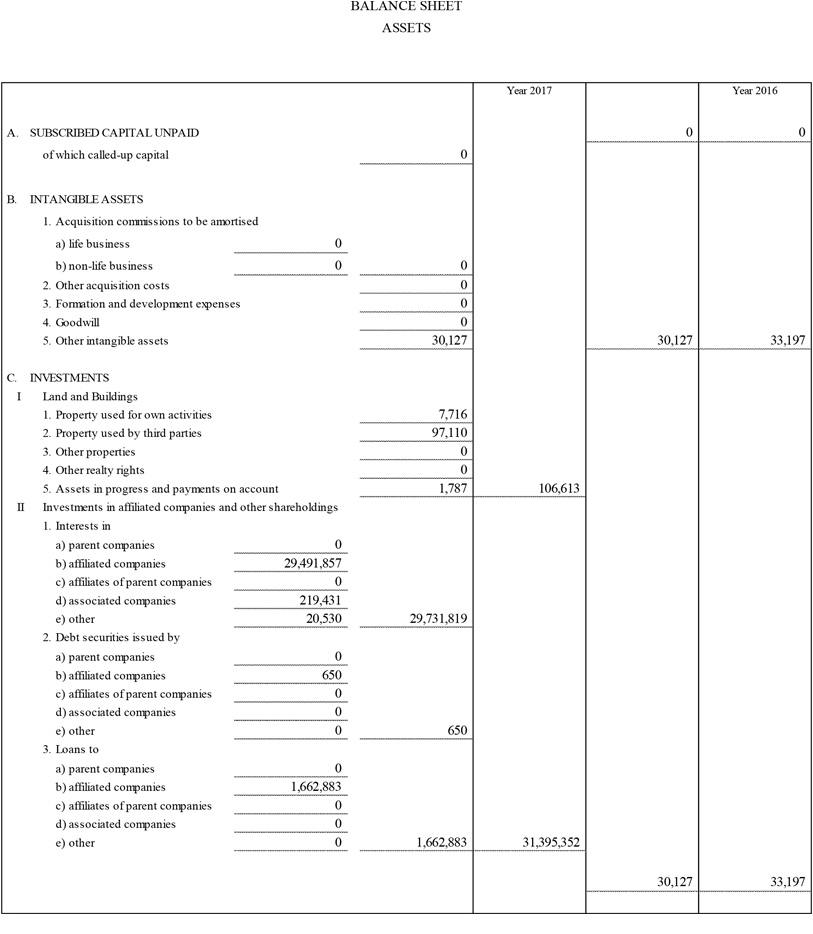

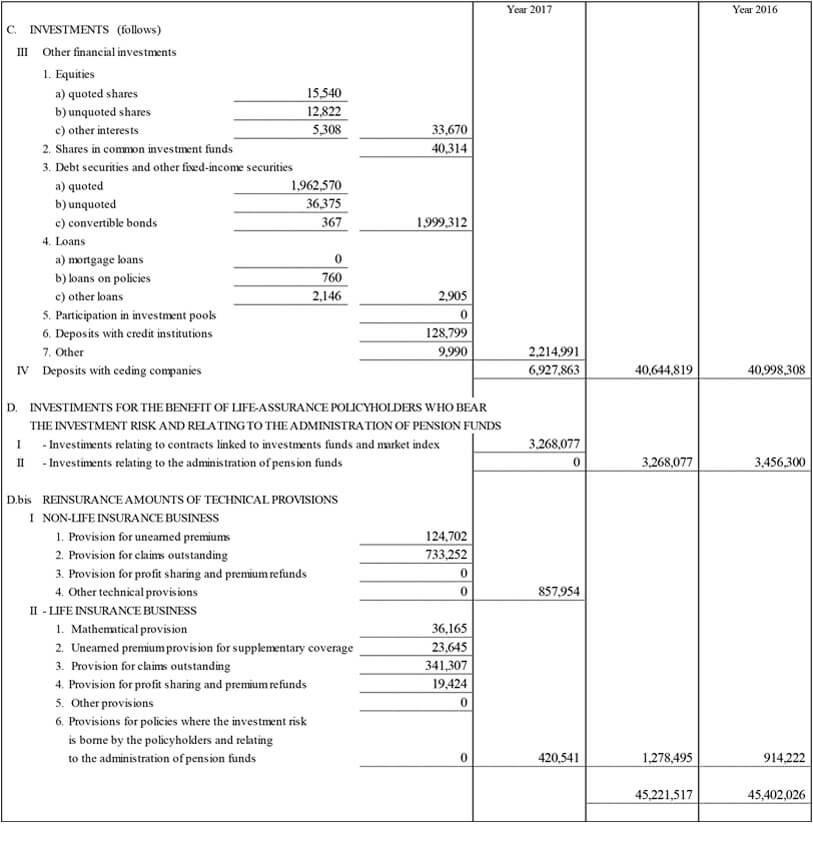

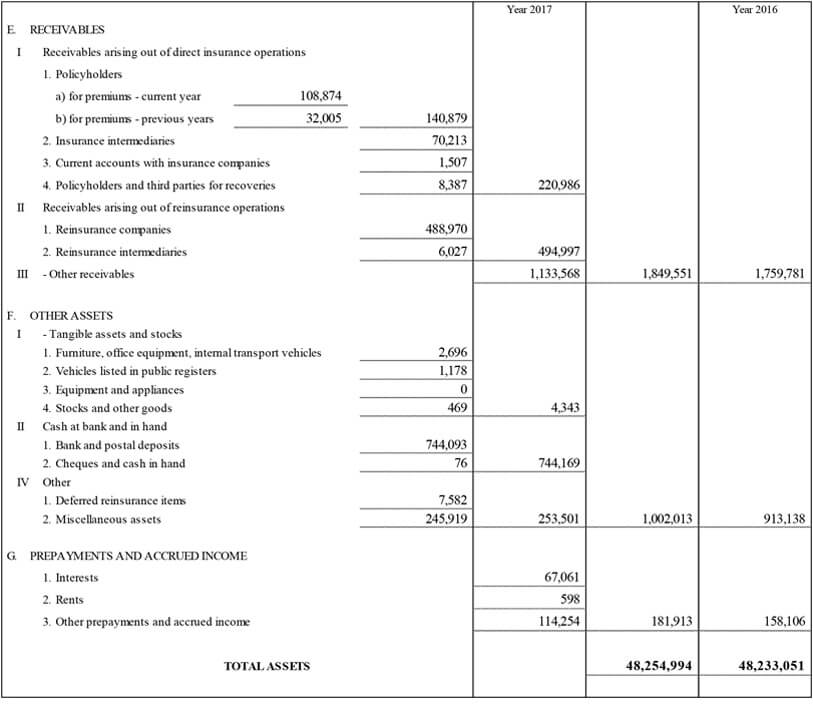

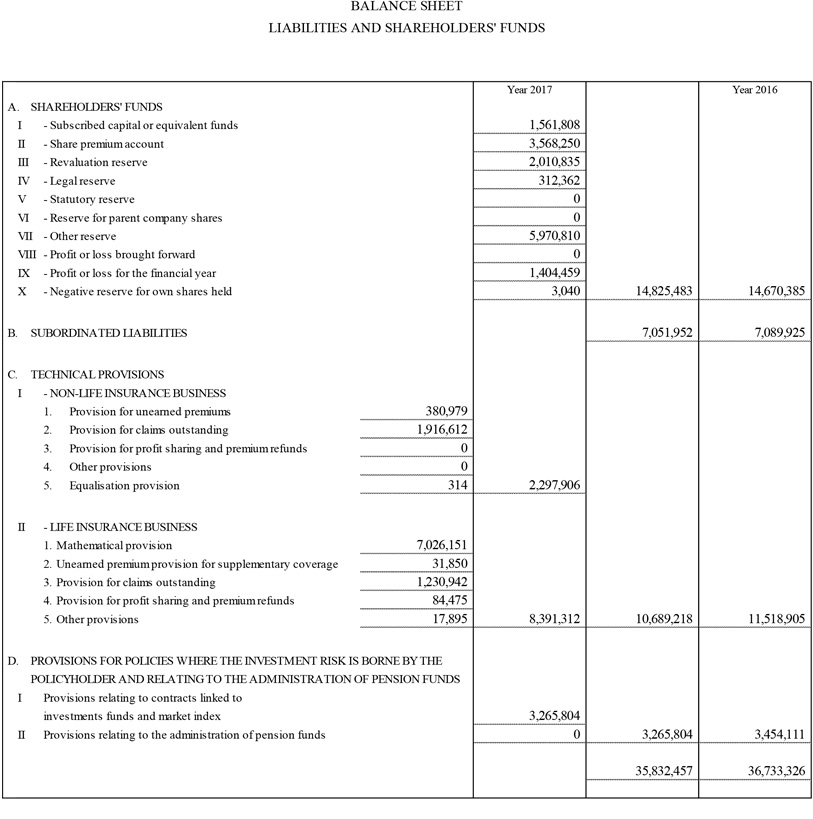

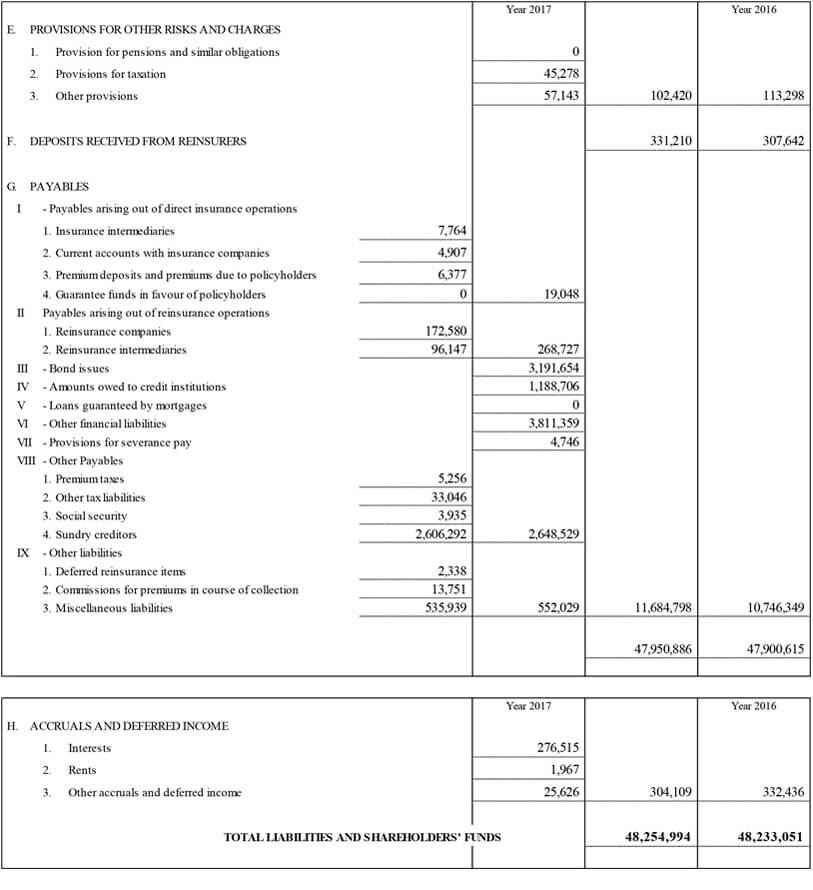

BALANCE SHEET

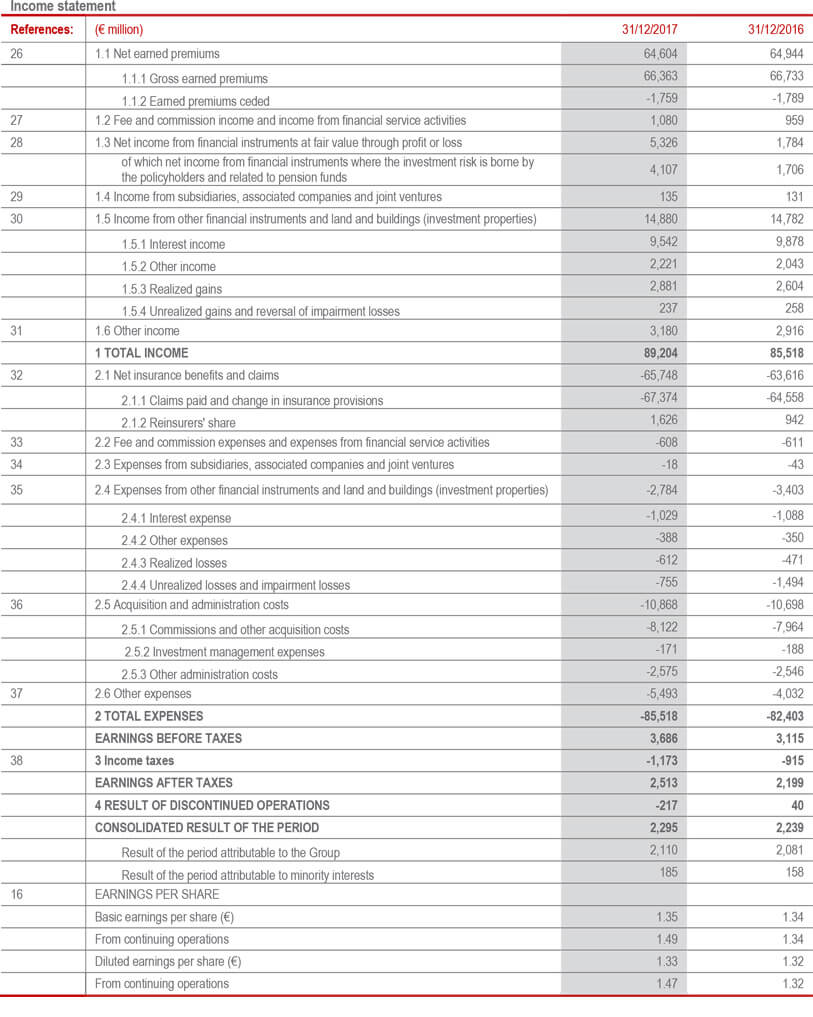

INCOME STATEMENT

Parent Company balance sheet and income statement

2.Parent Company balance sheet and income statement

BALANCE SHEET

(in thousands euro)

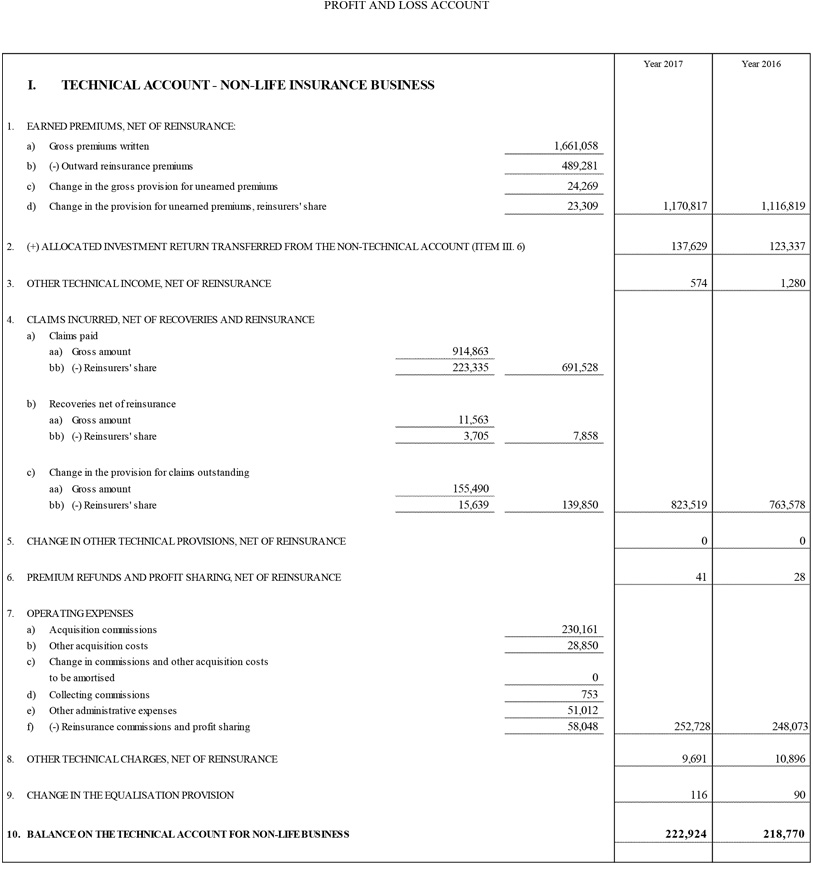

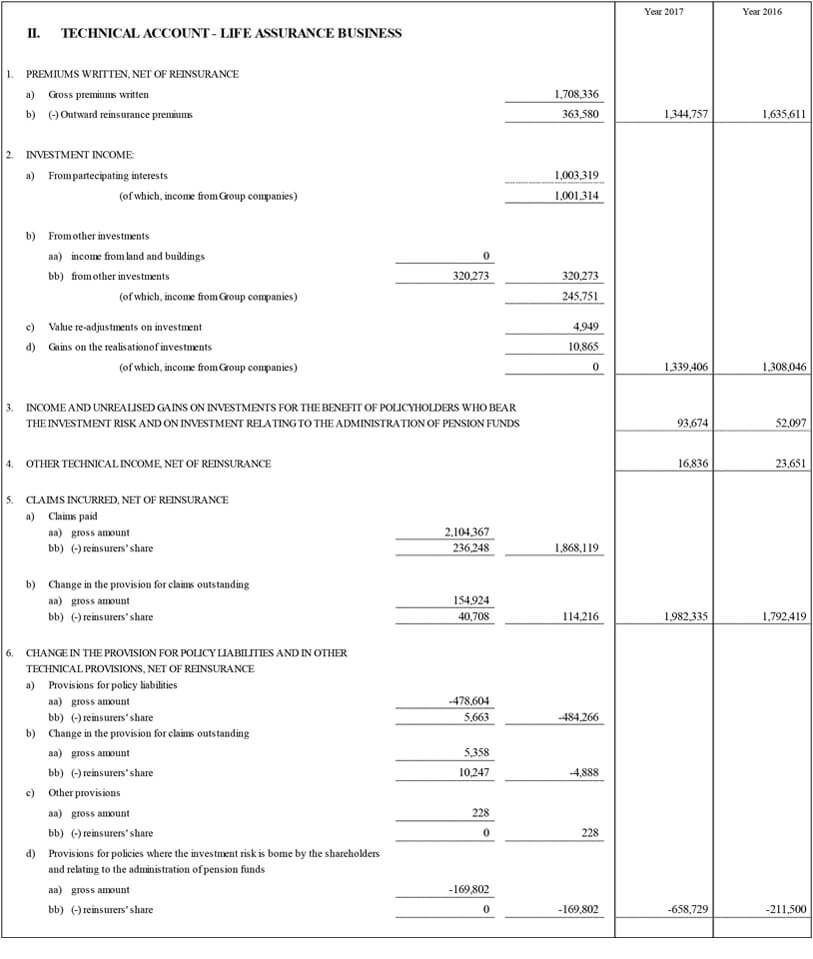

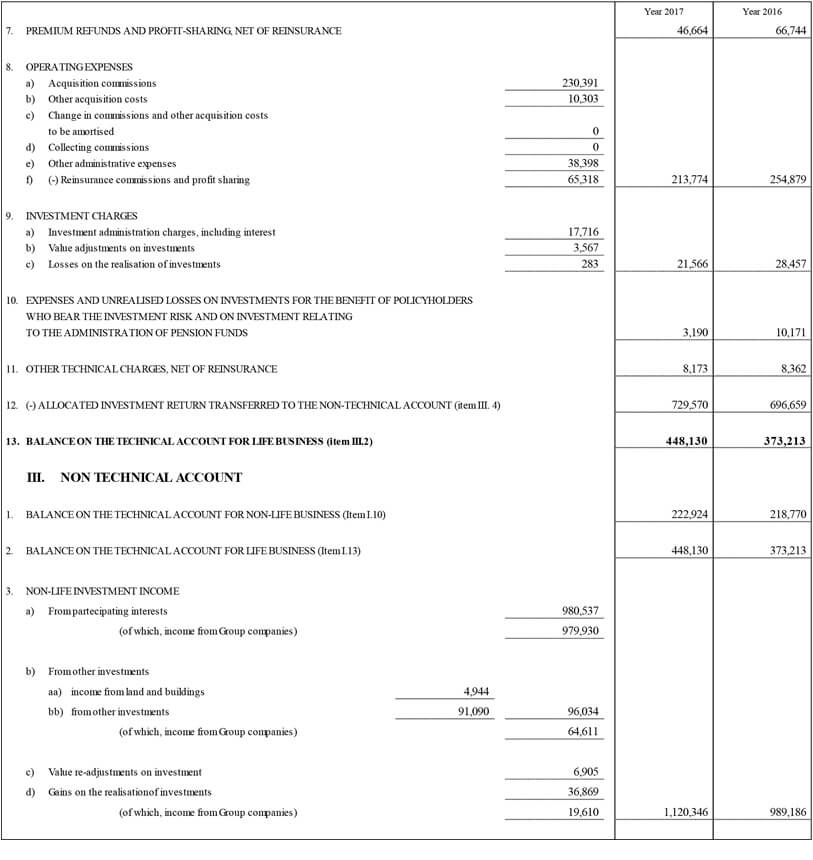

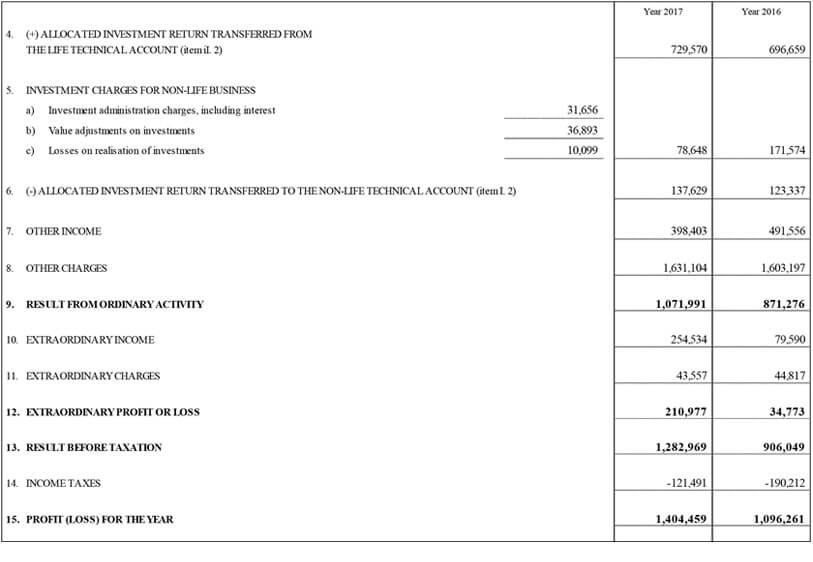

PROFIT AND LOSS ACCOUNT

(in thousands euro)