17 August 2021

Central banks’ strategies to cement dovish bias

Generali Investments’ Core Matters

Authors: Christoph Siepmann / Martin Wolburg / Paolo Zanghieri

- Fears of secular stagnation and higher concerns on inequality are leading to a new fiscal and monetary policy era, espe-cially in the US.

- The new Fed strategy is geared to full employment and will tolerate higher realised inflation. Some aspects remain rather vague, calling for a close monitoring of the evolution of the labour market and inflation expectations.

- The ECB is evolving too but faces a more difficult task given its different governance. The forthcoming review should cement a dovish bias.

- The BoJ will have to stick to its accommodation of fiscal expansion as its best means to overcome deflation risks.

- Persistent monetary support is a boon for risk assets, but at the same time increase their fragility to the rise in yields which will follow normalization and to the headwinds from more redistributive policies potentially hitting profits.

Central Banks: new challenges amid stretched policy stance

The new US administration has embarked on an ambitious plan to mitigate inequalities and spur growth via a relaunch of public investment. This could be the starting point of a new era of macroeconomic policy, not only in the US but on an international level. It also appears to be a major break-up with supply-side policies, introduced forty years ago by the Reagan/ Volcker tandem. In economic terms, we see fears of secular stagnation and greater concerns about in-equality as the main driving forces. On a higher level, mitigating the increasing split of societies, particularly so in the US, might be the ultimate motive.

Secular stagnation (in its most basic version: rather low growth rates for an extended period) and inequality are not independent of each other. Over the last decades, globalisation and technological progress have led to an increase in wealth, income and trade around the world but also to much more unequal distributions, especially in Advanced Economies. “Secular stagnation” has often been described as an “oversupply” of all things, which also constantly de-presses inflation. This lack of demand could be “inequality-driven”. As “rich” people typically have a higher savings rate and a lower marginal propensity to spend, the global “savings glut” creates a deflationary gap. Consequently, de-mand-side policies could help and fill the gap. However, to do this sustainably, taxes must be raised. The current initiative for a global minimum corporate tax shows the US ambition but also highlights political obstacles to push it through Congress.

Central banks have been accused of running easy monetary policies – not least through the Covid-19 crisis – that have pushed real estate and equity prices higher, thus especially supporting the “rich”. Yet the major central banks are adjusting their strategy by implicitly taking into account inequality and slower potential growth. The Fed last year committed to a more inclusive approach to employment. From a distributional perspective this implies a higher weight on poor (primarily affected by unemployment) versus middle-income people (primarily affected by inflation). The ECB released an update of its strategy on July 8 to endorse a more complex strategy comprising climate change and side-effects from its policy stance. Among other things, the ECB stated in an accompanying document that it will “continue to assess the two-way interaction between income and wealth distribution and monetary policy.” The Bank of Japan (BoJ) has recently developed more targeted tools (funding for lending schemes) that could be directed more specifically to sectors or special policies.

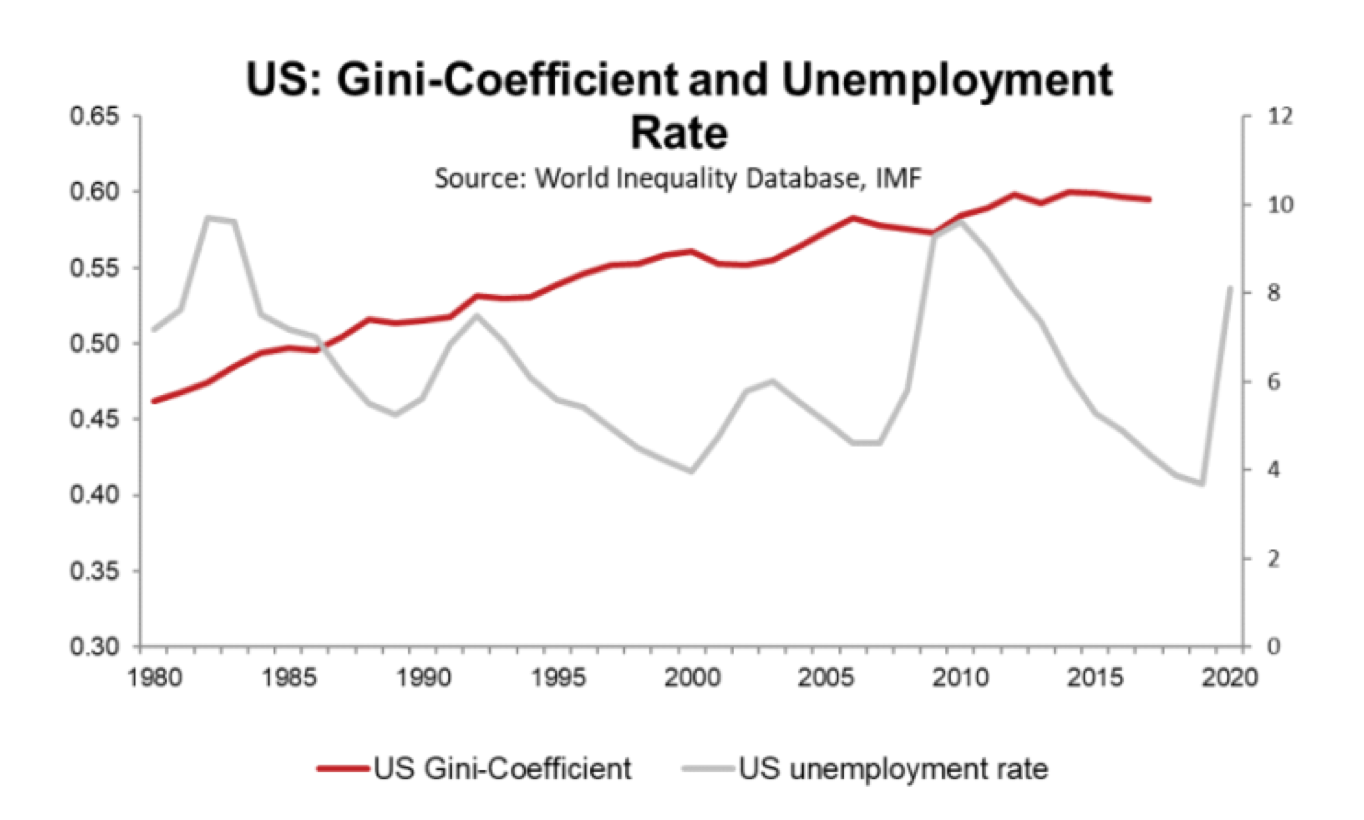

However, as the graph shows for the US, even very low un-employment failed to reduce inequality (measured by the Gini coefficient) in the past. In other words, cyclical policies have had a very limited impact on the structural inequality problem. Still, monetary policy can help to make fiscal policies more easily sustainable by buying government bonds, keeping key rates lower than otherwise (so-called financial repression) and tolerating higher inflation. It is debatable whether higher inflation would help the “poor” though.

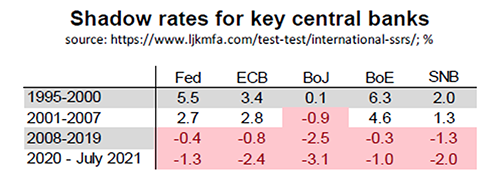

Monetary policy has already been ultra-accommodative for more than a decade, which complicates the matter. Shadow rates adjust the policy rate by incorporating the effect of un-conventional policy measures. Estimates for the major central banks show that they have been on a downtrend since the mid-90s and are currently negative. They first became negative in Japan with the BoJ fighting deflation; the GFC and the euro crisis led all other central banks to adopt measures that pushed the effective policy rate below zero. The Covid-19-induced policy measures pushed the shadow rates deeper into the negative. There are clearly limits for stretching these policies further. The recent spike in inflation and the uncertainty on how temporary it will be, add to the difficulties.

The case seems the clearest for Japan. With no meaningful inflation at the horizon, the BoJ will hardly be constrained. The Fed is probably most exposed to higher inflation problems - but they recently strengthened the labour market side of the dual target. Regarding inflation, the ECB finds itself between the BoJ and the Fed and has a different setting. But the recent review has also cemented a dovish bias.

In this piece we take stock of where the Fed, ECB and BoJ stand in the development of their monetary policy framework. Each has its own challenges:

- The Fed faces a credibility test, as its new monetary policy framework, more tolerant to inflation, lacks clarity and is being implemented during a period of volatile inflation. This requires investors to have a view on how the evolution of employment and expected inflation will fare in comparison with the target.

- As part of its new strategy the ECB has adopted a symmetric inflation target, became more complex and greener. The fundamental challenge will be to find a balance between satisfying the statutory inflation target in a low growth environment without neglecting the risks of financial market fragmentation between states (a threat to the stability of the euro area). In a low inflation environment, financing conditions will be key for monetary policy. They also comprise intra-EMU government bond spreads and the term premium. Indirectly this supports debt sustainability.

- After three decades of near zero inflation, the Bank of Japan has added funding for lending to its policy tools. But its main focus will continue to be government deficit monetisation.