Financial Information as of 31 March 2024 (1)

21 May 2024 - 07:00 price sensitive

Generali achieves continued operating result growth thanks to all segments. Return to positive Life net inflows. Solid capital position confirmed

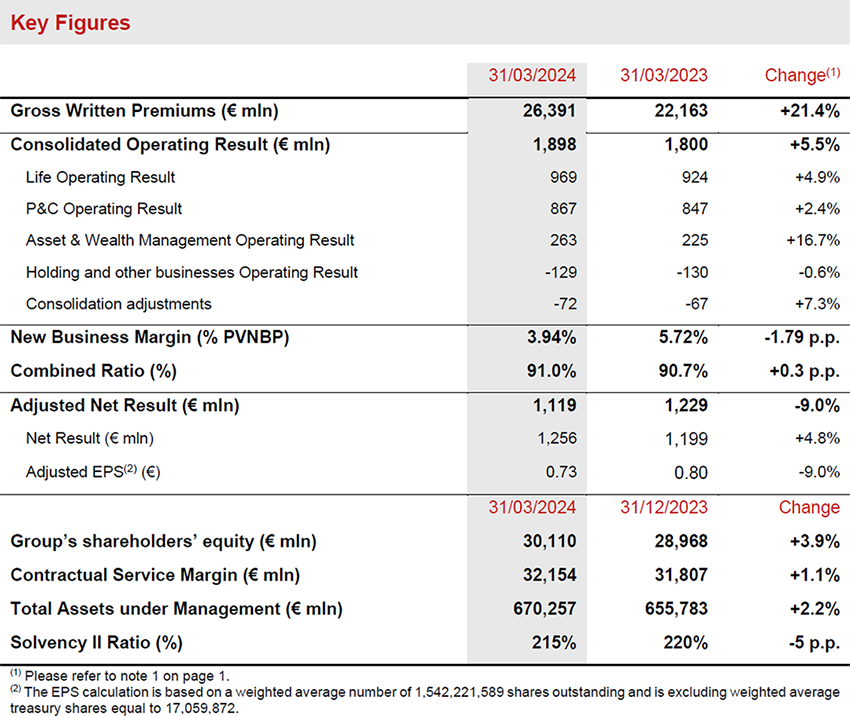

- Gross written premiums increased to € 26.4 billion (+21.4%), driven by both Life and P&C

- Positive Life net inflows at € 2.3 billion entirely thanks to protection and unit-linked and consistent with the Group’s strategy. New Business Value up 5.0%

- Combined Ratio was 91.0% (+0.3 p.p.). The undiscounted Combined Ratio improved to 93.7% (-0.5 p.p.)

- Continued growth in operating result to € 1.9 billion (+5.5%), thanks to the solid contribution of all business segments

- Adjusted net result was € 1.1 billion (-9.0%). The adjusted net result would have risen by 8.0% excluding a one-off capital gain incurred during 1Q2023

- Solid capital position confirmed, with Solvency Ratio at 215% (220% FY2023)

Generali Group CFO, Cristiano Borean, said: “In the first quarter of 2024 Generali delivered continued growth of its operating result, thanks to the solid contribution of all business segments. The Group achieved positive Life net inflows, built on our strategic decision to focus on protection and unit-linked lines and the commercial actions implemented during 2023. The P&C segment also benefits from the consolidation of Liberty Seguros for the first time, an acquisition which is already contributing positively to the Group’s earnings profile. Thanks to our diversified insurance and asset management model and solid capital position, driven by strong normalised capital generation, we remain fully on-track to meet all the targets of our ‘Lifetime Partner 24: Driving Growth’ strategy.”

Executive summary (2)

Milan - At a meeting chaired by Andrea Sironi, the Assicurazioni Generali Board of Directors approved the Financial Information at March 31st 20243 of the Generali Group.

The Group’s gross written premiums increased by 21.4% to € 26.4 billion, with strong performances in both the Life and P&C segments. Life net inflows returned to positive levels of € 2.3 billion, entirely driven by protection and unit-linked, in line with the Group’s strategy and reflecting the success of commercial actions implemented since 2023.

The operating result grew to € 1,898 million (+5.5%), with positive contribution from all business segments.

The Life operating result grew to € 969 million (+4.9%). New Business Value (NBV) improved to € 688 million (+5.0%).

The operating result of the P&C segment increased to € 867 million (+2.4%) also benefitting from Liberty Seguros, which was consolidated starting from February 2024. The Combined Ratio was 91.0% (90.7% 1Q2023) reflecting a smaller benefit from discounting. The undiscounted Combined Ratio improved to 93.7% (94.2% at 1Q2023).

The Asset & Wealth Management segment operating result grew significantly to € 263 million (+16.7%), thanks to the strong performance of Banca Generali.

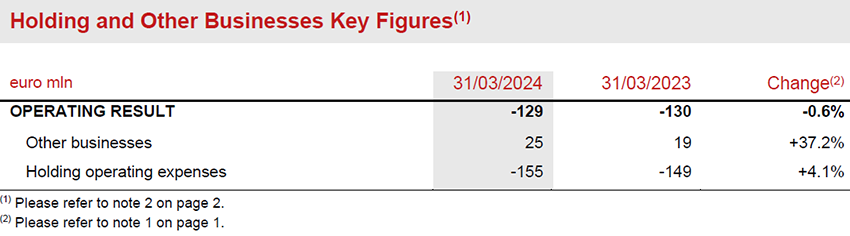

The operating result of the Holding and Other Businesses segment was € -129 million (€ -130 million 1Q2023).

The adjusted net result was € 1,119 million (€ 1,229 million 1Q2023). 1Q2023 included a non-recurring capital gain (€ 193 million net of taxes) related to a London real estate development disposal. Excluding this effect the adjusted net result would have increased by 8.0%.

The net result grew to € 1,256 million (€ 1,199 million 1Q2023) embedding € 58 million net capital gain from the disposal of TUA Assicurazioni.

The Group’s shareholders' equity increased to € 30.1 billion (€ 29.0 billion FY2023).

The Contractual Service Margin (CSM) grew to € 32.2 billion (€ 31.8 billion FY2023).

The Group's Total Assets Under Management increased to € 670.3 billion (€ 655.8 billion FY2023).

The Group confirmed its solid capital position, with a Solvency Ratio at 215% (220% FY2023). The decrease of 5 p.p. reflected in particular the acquisition of Liberty Seguros. This effect, coupled with the negative regulatory changes and the dividend provision for the period, has been partially offset by the sound contribution of normalised capital generation and the positive market variances.

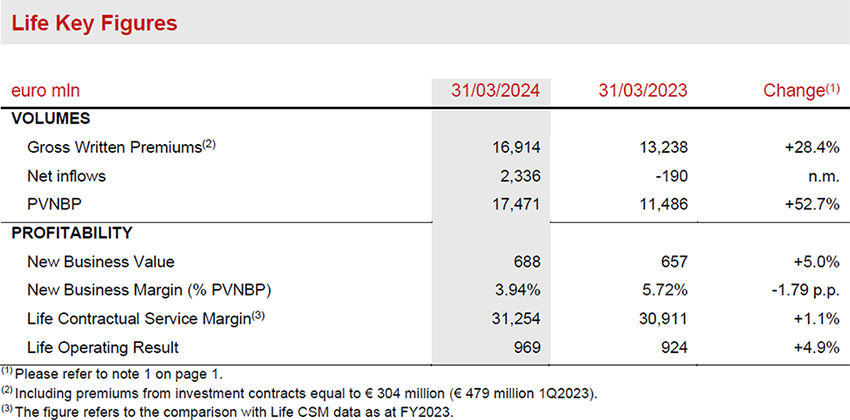

Life Segment

- New Business Value (NBV) increased to € 688 million (+5.0%) thanks to a very strong Present Value of New Business Premiums (PVNBP) growth (+52.7%)

- Life CSM grew to € 31.3 billion (+1.1%)

- Operating result stood at € 969 million (+4.9%)

Gross written premiums in the Life segment posted a strong growth reaching € 16.9 billion (+28.4%). The development was positive across all business lines, with particularly strong performance in savings and pension (+52.5%) in Italy and France, reflecting the commercial actions implemented since 2023, as well as in China. The protection line confirmed its healthy growth trajectory (+9.6%) in most countries. Unit-linked also increased (+8.6%), particularly in the largest markets of France, Italy and Germany.

Life net inflows were € 2.3 billion, returning to positive levels. Net outflows from savings and pension (€ -106 million) improved significantly compared to the same period of last year (€ -2,972 million 1Q2023), also benefitting from the commercial actions implemented since 2023. Protection and unit-linked lines recorded positive net inflows, with protection reaching € 1,490 million, led by Italy and France. Unit-linked net inflows were € 951 million.

New business volumes (expressed in terms of present value of new business premiums - PVNBP) increased significantly to € 17.5 billion (+52.7%) thanks to:

- strong production of savings in Italy to support the traditional business net inflows;

- France, benefitting from the market momentum in hybrid sales;

- China, which recorded exceptional volumes in the first quarter (also driven by regulatory changes becoming effective in April) that are expected to return to more normal levels going forward;

- growth of protection business, amplified by the IFRS 17 accounting treatment of collective protection business in France4. After neutralising for this accounting effect with no real economic implications, PVNBP would have grown by 31.8%.

New Business Value (NBV) rose to € 688 million (+5.0%), supported by strong volumes. The New Business Margin on PVNBP (NBM) stood at 3.94% (-1.79 p.p.). The NBM reduction would have been halved to around -0.9 p.p. after neutralizing the accounting effect of French protection business. Aside from this, the reduction mainly reflects the commercial initiatives to support net inflows in Italy, the effect of lower interest rates and a larger weight of China.

The Life Contractual Service Margin (Life CSM) increased to € 31.3 billion (€ 30.9 billion FY2023). The positive development was mainly driven by the contribution of the Life New Business CSM of € 826 million, which, coupled with the expected return of € 424 million, more than offset the Life CSM release of € 761 million. The latter also represented the main driver (approximately 80%) of the operating result, which rose to € 969 million (€ 924 million 1Q2023).

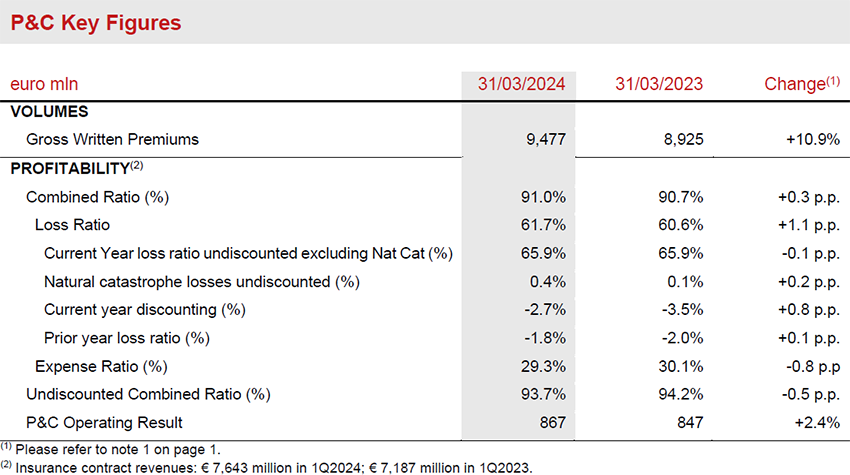

P&C Segment

- Premiums increased to € 9.5 billion (+10.9%)

- Combined Ratio at 91.0% (+0.3 p.p.). Undiscounted Combined Ratio improved to 93.7% (-0.5 p.p.)

- Operating result grew to € 867 million (+2.4%)

P&C gross written premiums grew to € 9.5 billion (+10.9%) driven by the positive performance of both business lines.

Non-motor increased by 6.0%, achieving widespread growth across all main areas. Europ Assistance premiums grew by 6.1%, on top of the very strong double-digit expansion achieved during 2023.

The motor line rose by 17.6% across all the main areas, with particularly positive business dynamics in CEE, Germany, Italy, Austria and Asia. Excluding the contribution from Argentina, a country impacted by hyperinflation, motor line premiums increased by 5.5%.

The Combined Ratio reached 91.0% (90.7% 1Q2023) due to an increase in the loss ratio to 61.7% (+1.1 p.p.), which was mainly caused by a lower current year discounting benefit. The undiscounted combined ratio improved to 93.7% (94.2% 1Q2023). The undiscounted current year loss ratio (excluding nat cat) remained stable at 65.9%. The expense ratio decreased to 29.3% (30.1% 1Q2023).

The operating result grew to € 867 million (+2.4%) also reflecting the positive contribution from the consolidation of Liberty Seguros. The operating insurance service result was € 685 million (€ 667 million 1Q2023) notwithstanding a lower discounting effect of € 205 million compared to € 250 million at 1Q2023. The undiscounted operating insurance service result grew by 15.1% to € 481 million (€ 418 million 1Q2023).

The investment result was € 182 million (€ 180 million 1Q2023), reflecting a € 124 million increase in the operating investment income that was compensated by € 123 million increase in the insurance finance expenses.

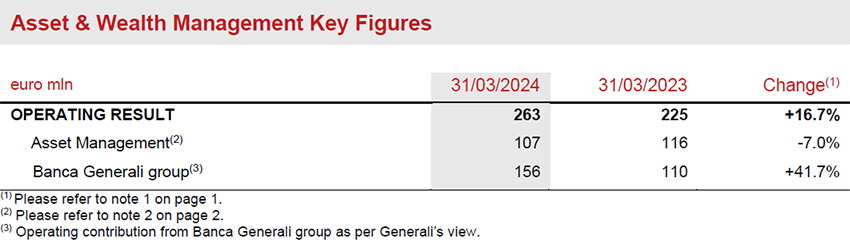

Asset & Wealth Management Segment

- Asset & Wealth Management operating result increased to € 263 million (+16.7%)

- Banca Generali group operating result rose to € 156 million (+41.7%)

The operating result of the Asset & Wealth Management segment stood at € 263 million (+16.7%).

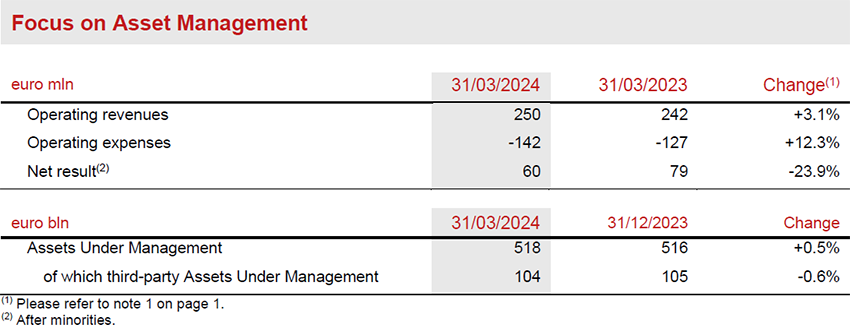

In particular, the Asset Management operating result stood at € 107 million (-7.0%). Operating revenues posted a positive development (+3.1%), reflecting in particular the growth of recurring fees to € 214 million (+3.9%).

Operating expenses rose to € 142 million (+12.3%), impacted mainly by a difference in timing of variable compensation costs, which last year were booked in the second quarter. Excluding this item, the operating result would be broadly stable.

The operating result of the Banca Generali group rose to € 156 million (+41.7%), thanks to the positive contribution of the net interest margin, continuous diversification of fee income sources and important contribution of performance fees. Total net inflows at Banca Generali in 1Q2024 were € 1.6 billion.

The net result of the Asset Management segment was € 60 million (-23.9%). Besides the operating expenses item mentioned above, the net result was also impacted by some one-off costs related to the acquisition of Conning Holdings Limited and different timing in tax payments, which last year were booked in the second quarter. Adjusting for both operating and non-operating timing effects, the net result would have declined by less than 5%.

The AUM pertaining to the Asset Management companies were € 518 billion, slightly up compared to FY2023. Third-party AUM were broadly flat at € 104 billion compared to FY2023. Net flows from external clients were positive for € 0.4 billion in 1Q2024.

Holding and other businesses Segment

- Operating result stable at € -129 million

- Positive contribution from France

The operating result of the Holding and Other Businesses segment was stable at € -129 million (€ -130 million 1Q2023). The contribution from Other businesses was € 25 million, growing by € 7 million compared to 1Q2023, thanks to the improvement of France’s investment income.

Holding operating expenses increased to € -155 million, mainly reflecting project costs and higher shared-based payments which were € -23 million in 1Q2024 (€ -20 million 1Q2023).

Outlook

Over the coming months, the expected timing and extent of rate cuts by central banks are set to drive financial markets in the US and Europe as inflation pressures continue to ease, even if along a more gradual path than seen over 2023. The Fed and ECB are likely to proceed cautiously in easing their policy amid tight labour markets and strong wage growth. Global growth in 2024 may slightly slow versus 2023, while the Euro area is set to recover following a protracted period of stagnation.

In this context and in line with the priorities set out in the “Lifetime Partner 24: Driving Growth” plan, the Group continues to execute its strategy to rebalance the Life portfolio to further increase profitability and allocate capital more efficiently. It will also maintain its focus on product simplification and innovation, with the introduction of a range of modular product solutions that are designed to meet customer needs and are marketed through the most suitable and efficient distribution channels. Primary focus areas include protection and health, as well as capital-light savings.

In the Property & Casualty segment, the Group's objective is to maximize profitable growth - with a focus on the non-motor line - across its insurance markets, particularly strengthening its position and offering in countries with high growth potential. The Group will strengthen its adaptive approach towards tariff adjustments in both motor and non-motor, taking into account the increase in reinsurance coverage costs due to the increased natural catastrophe claims in recent years. The growth of the P&C segment will continue with the aim of enhancing its leadership in the European insurance market for private individuals, professionals and small and medium-sized enterprises (SMEs) and also benefitting from the recent acquisition of Liberty Seguros operations in Spain, Portugal and Ireland.

In the Asset & Wealth Management segment, following the important milestone of the acquisition of Conning Holdings Limited completed on April 3rd 2024, Asset Management will continue to implement its strategy with the objectives of expanding the product offering, particularly in real and private assets, enhancing third party distribution capabilities, and extending its presence in new markets. In Wealth Management, the Banca Generali group will continue to focus on its targets of growth, profitability and shareholders’ remuneration as outlined in its strategic plan.

With reference to the Group’s investment policy, it will continue to pursue an asset allocation strategy aimed at ensuring consistency with liabilities to policyholders and, where possible, at increasing current returns.

The Group confirms its commitment to pursue sustainable growth, enhance its earnings profile and lead innovation. This is in order to achieve a compound annual growth rate in earnings per share5 between 6% and 8% in the period 2021-2024, generate Net Holding Cash Flow6 exceeding € 8.5 billion in the period 2022-2024 and distribute cumulative dividends to shareholders for an amount between € 5.2 billion and € 5.6 billion in the period 2022-2024, with a ratchet policy on the dividend per share. With the payment of the 2023 dividend on May 22nd, the Group achieves the latter target reaching cumulative dividends in the period 2022-2024 of € 5.5 billion.

Significant events after March 31st 2024

On April 3rd Generali announced the completion of the acquisition of Conning and its affiliates from Cathay Life.

On April 18th Generali presented a new organizational structure for an integrated insurance and asset management Group.

On April 24th the 2024 Annual General Meeting approved the 2023 Financial Statements, dividend distribution and € 500 million share buyback7.

Other significant events that occurred after the end of the period are available on the website.

***

The glossary and the description of alternative performance indicators are available in the Group Annual Integrated report 2023.

Q&A conference call

The Group CFO, Cristiano Borean, the Group General Manager, Marco Sesana and the CEO Insurance, Giulio Terzariol, will host the Q&A session conference call for the results of the Generali Group at March 31st 2024, which will be held on May 21st 2024, at 12.00 pm CEST.

To follow the conference call, in a listen only mode, please dial +39 02 8020927.

***

The Manager in charge of preparing the company’s financial reports, Cristiano Borean, declares, pursuant to paragraph 2, article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

1 Changes in premiums, Life net inflows and new business are presented on equivalent terms (at constant exchange rates and consolidation scope).

The amounts are rounded and may not add up to the rounded total in all cases. Also, the percentages presented can be affected by the rounding.

21Q2023 figures have been restated considering: (1) LTIP and other share-based payments (including WeShare plan) have been moved from non-operating results to operating results (€ 21 million in 1Q2023; € 24 million 1Q2024); (2) AWM segment now includes all the operating and non-operating costs that were previously considered as holding expenses, including the aforementioned LTIP and other share-based payments (respectively € 7 million in the operating result and € 1 million in the non-operating result).

3The Financial Information at March 31st 2024 is not an interim Financial Report according to the IAS 34 principle.

4French collective protection business underwritten in 4Q2023 with coverage starting in 2024 was deemed to be profitable and hence recognized entirely in 1Q2024. In 2023, the majority of this business, underwritten at the end of 2022, was considered onerous and thus recognized earlier in 4Q2022, in line with IFRS 17 requirements.

53 year CAGR based on 2024 Adjusted EPS (according to IFRS 17/9 accounting standards and Adjusted net result definition currently adopted by the Group), versus 2021 Adjusted EPS (according to IFRS 4 accounting standards and Adjusted net result definition adopted by the Group until 2022).

6Net Holding Cash Flow and dividend expressed on cash basis (i.e. cash flows are reported under the year of payment).

7Subject to regulatory approval.