Generali Group consolidated results as at 31 December 2025

12 March 2026 - 07:00 price sensitive

Generali achieves record operating and adjusted net result in successful first year of “Lifetime Partner 27: Driving Excellence”

- Gross written premiums increased to € 98.1 billion (+3.6%) thanks to significant growth in P&C (+7.6%)

- Best-in-class Life net inflows, rising to € 13.5 billion driven by Protection & Health and Unit-Linked & Hybrid. New Business Value grew to € 3.1 billion (+6.2%)

- Combined Ratio (CoR) improved significantly to 92.6% (-1.4 p.p.); undiscounted CoR continued its very positive development to 94.3% (-1.6 p.p.)

- Best-ever operating result at € 8.0 billion (+9.7%) driven by all business segments

- Adjusted net result reached all-time high of € 4.3 billion (+14.5%). Adjusted EPS rose substantially to € 2.85 (+16.2%)

- Total AUM of € 900 billion (+4.3%), with € 16 billion net inflows in Asset Management

- Extremely solid capital position with Solvency Ratio at 219% (210% FY2024) thanks to the Group’s strong normalised capital generation

- Dividend per share of € 1.64 (+14.7%) and € 500 million share buyback to be proposed at AGM, confirming commitment to increased shareholder returns

Generali Group CEO, Philippe Donnet, said: "Our record 2025 results mark a very successful first year of our strategic plan ‘Lifetime Partner 27: Driving Excellence’ and confirm the continued value creation for all our stakeholders. In an environment still characterised by great uncertainty, we further strengthened our role as a true Lifetime Partner for all customers, offering them protection, stability and peace of mind. The focus on excellence in core capabilities is reflected in the outstanding P&C performance, with strong underlying technical profitability, and in the best-in-class Life net inflows, which highlight Generali’s European leadership in this segment and the high quality of the new production. Asset & Wealth Management also demonstrated increasing momentum with solid net inflows. Furthermore, we are accelerating the transformation of the Group operating model through the broad deployment of AI, digitalisation and automation, and we are very pleased with the remarkable progress made towards our ambitious Sustainability targets. Building on this impressive delivery and our very strong capital position, and consistently with the clear commitment to ensuring ever‑growing returns to our shareholders, we are once again proposing an increased dividend per share, alongside the launch of the 500 million euro share buyback for 2026. Our people are the key foundation of the success of the Group, and I want to sincerely thank all colleagues and advisors for this outstanding start to the strategic plan.”

Executive summary

Milan – At a meeting chaired by Andrea Sironi, the Generali Board of Directors approved the consolidated financial statements and the Parent Company’s draft financial statements for the year 2025.

Gross written premiums rose to € 98.1 billion (+3.6%), thanks to significant growth in both Life and P&C.

Life net inflows were very positive at € 13.5 billion mainly driven by Protection & Health and Unit-Linked & Hybrid, in line with the Group’s strategy.

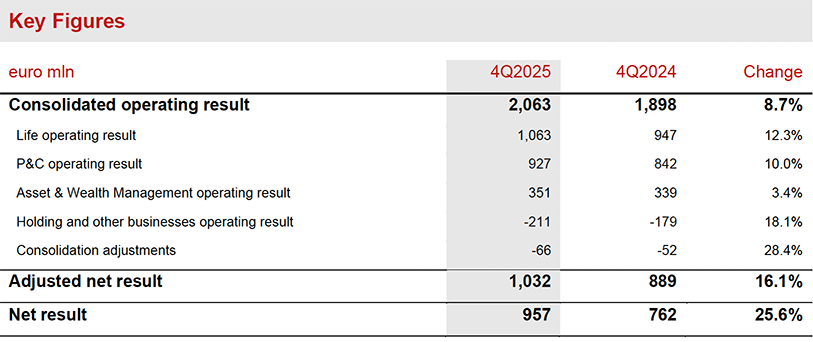

The operating result grew to a record € 8,004 million (+9.7%), thanks to the positive performance of all business segments.

The Life operating result increased to € 4,154 million (+4.3%) and the New Business Value improved to € 3,147 million (+6.2%).

P&C operating result grew very strongly to € 3,663 million (+20.0%) with the Combined Ratio improving to 92.6% (-1.4 p.p.) and the undiscounted Combined Ratio continuing its very positive development to 94.3% (-1.6 p.p.). It also benefitted from the improved undiscounted current year attritional loss ratio and a lower impact from natural catastrophes, partially offset by prior year development.

The operating result of Asset & Wealth Management reached € 1,194 million (+1.5%) mainly driven by the Asset Management result, which increased to € 662 million (+7.5%). The operating result of the Holding and other businesses was € -610 million (€ -536 million FY2024).

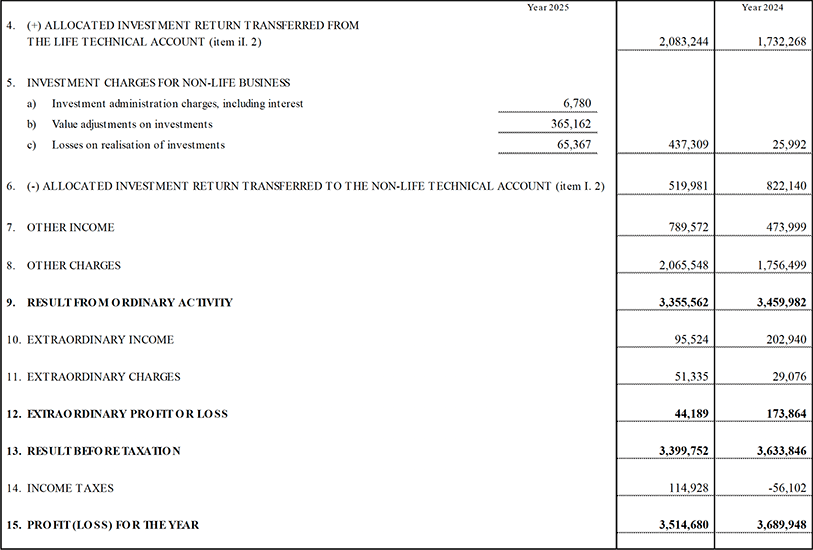

The adjusted net result1 rose by 14.5% to a record high of € 4,315 million (€ 3,769 million FY2024) – demonstrating the positive effect of the Group’s diversified profit sources.

The net result grew by 12.0% to € 4,172 million (€ 3,724 million FY2024) driven by the business performance in the period.

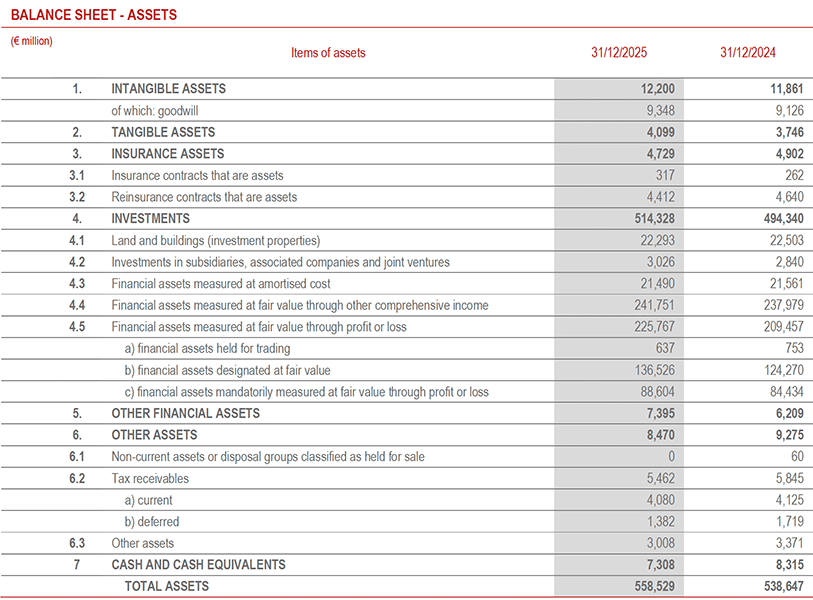

The Group’s shareholders' equity increased to € 32.1 billion (+5.5%) thanks to the results in the period and the issuance of the € 500 million perpetual Restricted Tier 1 bond classified as an equity instrument, partially offset by the 2025 dividend payment, the purchase of treasury shares related to the Group’s incentive plans and the € 500 million share buyback.

The Contractual Service Margin (CSM) rose by 10.8% to € 34.6 billion (€ 31.2 billion FY2024).

The Group’s Total Assets Under Management (AUM) grew significantly to € 900 billion (+4.3% compared to FY2024) with third party AUM reaching a record level of € 384 billion of which € 273 billion is managed by Asset Management.

The Group confirms its extremely solid capital position, with the Solvency Ratio at 219% (210% FY2024) thanks to strong normalised capital generation.

Dividend per share

The dividend per share, which will be proposed at the upcoming Annual General Meeting, is € 1.64 payable as from 20 May 2026, while shares will trade ex-dividend as from 18 May 2026.

This represents a 14.7% increase compared to the prior year, reflecting the Group’s excellent results, the strong cash and capital position and the increasing focus on shareholder returns set out in the “Lifetime Partner 27: Driving Excellence” strategic plan.

The dividend proposal represents a total maximum pay-out of € 2,480 million.

The Group also confirmed its intention to launch a € 500 million share buyback for 2026, subject to AGM and regulatory approval.

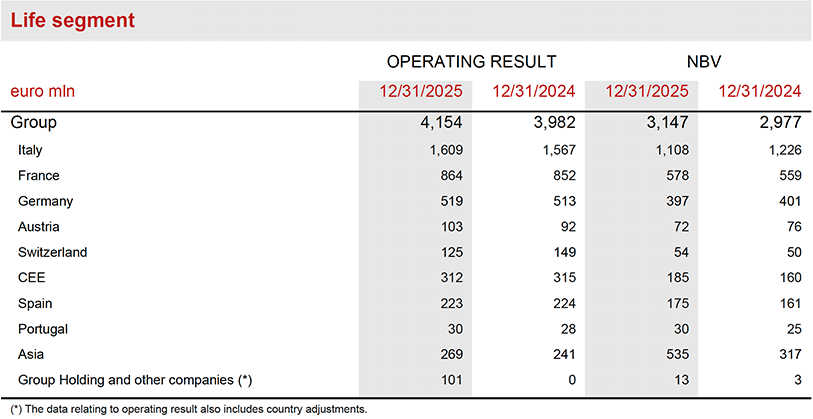

Life

- Operating result rose to € 4,154 million (+4.3%)

- Life net inflows were very positive at € 13.5 billion (+42.5%)

- New Business Margin was 5.66% (+0.25 p.p.); New Business Value (NBV) grew to € 3,147 million (+6.2%)

Gross written premiums in Life increased to € 61.9 billion (+1.4%) driven by savings and protection & health. Specifically, savings recorded a strong increase (+10.7%), specifically in Asia (+46.3%), while protection & health (+5.6%) grew in most countries in which the Group operates. Hybrid and Unit-Linked products recorded a 4.0% contraction, reflecting the comparison with a strong FY2024 during which targeted commercial actions were implemented.

Life Net inflows continued their strong upward trend, reaching € 13,487 million (€ 9,674 million FY2024), thanks to the positive contribution of all business segments and lower surrenders. Net inflows in savings rose to € 2,406 million, driven by Italy, Germany, and Asia. Protection & health stood at € 4,472 million, mainly supported by inflows in Italy while Hybrid and Unit-Linked products reached € 6,608 million, benefitting in particular from growth in France.

New Business Volumes (expressed in terms of present value of new business premiums - PVNBP) rose to € 55.6 billion (+1.5%), mainly thanks to solid production in France, Germany and Asia. New Business Value (NBV) grew significantly to € 3,147 million (+6.2%), supported by higher volumes and improved profitability. New Business Margin (NBM) increased to 5.66% (+0.25 p.p.).

Life Contractual Service Margin (Life CSM) increased to € 33.6 billion (€ 30.3 billion FY2024) supported by the contribution of New Business CSM, amounting to € 3,010 million, and by the expected return of € 1,492 million, which more than offset the release of Life CSM for € 3,223 million.

Life operating result increased to € 4,154 million (€ 3,982 million FY2024), driven by the rise in the operating insurance service result, which amounted to € 3,243 million (€ 3,039 million FY2024). This is mainly composed of the release of the contractual service margin, which improved to € 3,233 million (€ 2,986 million FY2024). This result more than compensated for the slight decline in the operating investment result, amounting to € 911 million (€ 943 million FY2024).

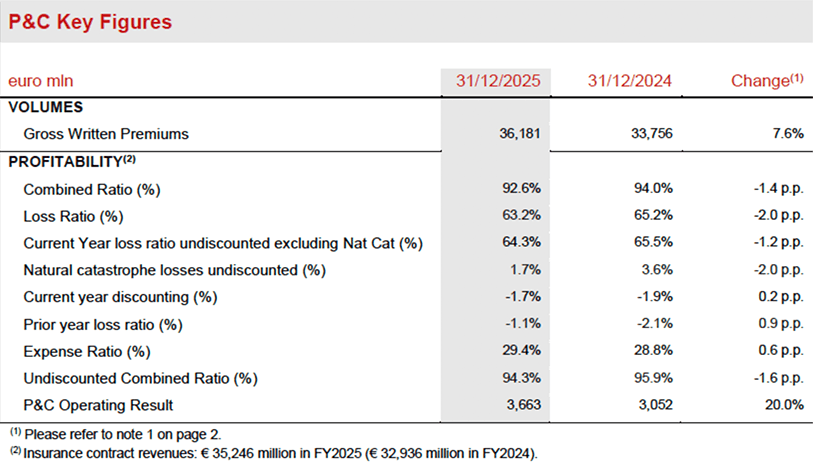

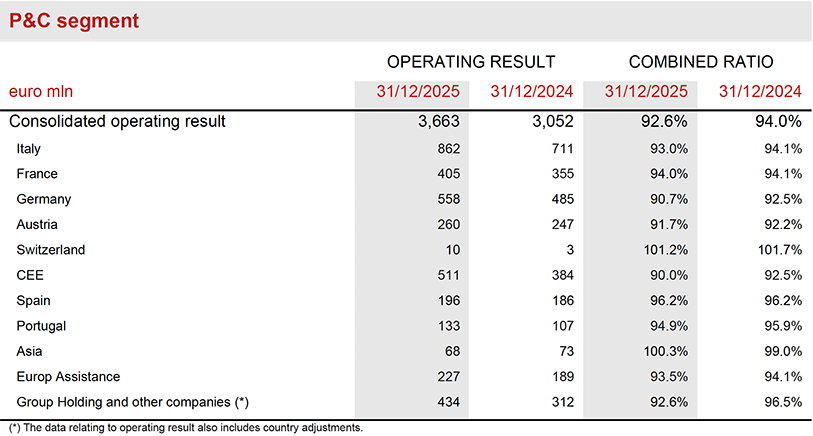

P&C

- Operating result grew strongly to € 3,663 million (+20.0%)

- Premiums increased significantly to € 36.2 billion (+7.6%)

- Combined Ratio improved significantly to 92.6% (-1.4 p.p.). Undiscounted Combined Ratio continued its positive development to 94.3% (-1.6 p.p.)

P&C gross written premiums grew significantly to € 36.2 billion (+7.6%) thanks to the performance of both business lines. Non-motor was up 7.3% while motor rose by 7.5% with both achieving growth across all main areas in which the Group operates. Considering also the accepted business underwritten by Europ Assistance, non-motor premiums grew by 7.5%. Excluding the contribution from Argentina, a country impacted by hyperinflation, motor premiums increased by 5.7%.

Combined Ratio improved to 92.6% (94.0% FY2024) reflecting the improvement in the loss ratio to 63.2% (-2.0 p.p.), partially offset by an increase in expense ratio to 29.4% (+0.6 p.p.) entirely driven by higher acquisition costs. The trend in the loss ratio reflects an improved current year attritional profitability (excluding Nat Cat) and a reduced impact from undiscounted Nat Cat losses of 1.7%, corresponding to € ‑593 million (€ ‑1,202 million FY2024). These effects offset the lower benefit from current year discounting, equal to ‑1.7% (+0.2 p.p.), as well as the reduced contribution from prior year development (+0.9 p.p.).

Undiscounted combined ratio improved to 94.3% (95.9% FY2024).

The operating result increased to € 3,663 million (€ 3,052 million FY2024), benefitting from the strong increase in the operating insurance service result, which rose to € 2,613 million (€ 1,976 million FY2024), more than offsetting the decrease in the operating investment result to € 1,050 million (€ 1,076 million FY2024). The decrease was entirely related to Argentina, due to the very significant decline in the local inflation rate. The operating investment result excluding Argentina improved to € 1,018 million (€ 976 million FY2024).

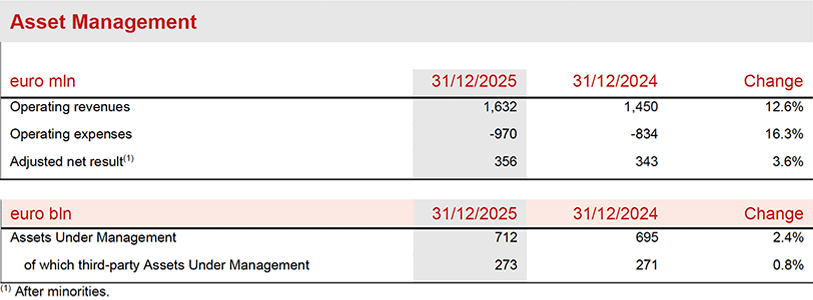

Asset & Wealth Management

- Asset & Wealth Management operating result amounted to € 1,194 million (+1.5%)

- Third party AUM reached the record level of € 273 billion (+0.8%), supported by € 9.6 billion of positive net inflows and the consolidation of MGG

- Banca Generali group operating result was € 532 million (-5.1%) reflecting the lower contribution from performance fees

The Asset & Wealth Management operating result amounted to € 1,194 million (+1.5%). The Asset Management operating result increased to € 662 million (+7.5%), thanks to higher performance fees and the contribution of Conning Holdings Limited (CHL) and its subsidiaries, including MGG Investment Group. The decrease in the Banca Generali group operating result, which was €532 million (-5.1%), reflects the lower contribution from performance fees.

Operating revenues increased to € 1,632 million (+12.6%) thanks to the contribution of CHL and its subsidiaries (€ 378 million), higher average value of AUM, and an increase in average fee margins as well as higher performance fees of € 162 million (€ 91 million at FY2024).

Operating expenses rose to € 970 million (+16.3%), mainly due to the inclusion of CHL and its subsidiaries for € 280 million and higher personnel costs. The Asset Management cost/income ratio was up to 59.4% (+1.9 p.p.) mainly reflecting the full-year consolidation of CHL and its subsidiaries.

The adjusted net result of Asset Management increased to € 356 million (+3.6%). The net result was also affected by integration and M&A costs, as well as other non‑recurring items recorded in the non‑operating result.

AUM pertaining to the Asset Management companies grew to € 712 billion at YE2025 (+2.4% compared to YE2024), a result achieved despite a negative impact of approximately € 26 billion due to foreign exchange movements. The growth was mainly supported by positive net inflows amounting to € 16.2 billion and the positive market environment.

Third party AUM managed by the Asset Management companies grew to a record level of € 273 billion (+0.8%), supported by € 9.6 billion of positive net inflows and strong performance across the affiliates despite the foreign exchange impact.

Holding and other business

- Operating result was € -610 million

Operating result of the Holding and other businesses segment was € -610 million (€ -536 million FY2024).

The operating result of Other businesses was € 150 million (€ 157 million FY2024), mainly resulting from a one‑off exit tax payment related to the closure of a foreign entity and lower intra‑group dividends. Holding operating expenses increased by 9.8%, also due to costs related to strategic projects.

Solvency, Capital Generation and Net Holding Cash Flow

- Extremely solid capital position with the Solvency Ratio at 219% (210% FY2024)

- Continued strong Normalised Group Capital Generation rising to € 5.2 billion

- Net Holding Cash Flow at € 3.8 billion

The Group confirms its extremely solid capital position with a Solvency Ratio at 219% (210% FY2024). The increase reflected the sound contribution of normalised capital generation (+20 p.p.) and positive market variances (+14 p.p.). These factors more than offset the negative regulatory changes (-3 p.p.), non-economic variances (-8 p.p.), M&A operations (-3 p.p.) and capital movements (-11 p.p.). The impact from the proposed new € 500 million share buyback announced today will be accounted for on the Solvency Ratio after having received all the relevant approvals.

Normalised Group Capital Generation, which includes the full impact from the share buyback for the Long-Term Incentive Plan (LTIP) executed in 2025, increased to € 5.2 billion (€ 4.8 billion FY2024) and was supported by the positive performance of all business segments.

Net Holding Cash Flow was € 3.8 billion (€ 3.8 billion FY2024), mainly thanks to growing remittance entirely driven by recurring components and higher reinsurance cash flows. This more than compensated the increase in Holding company expenses, driven by the launch of strategic initiatives, and a normalisation of the tax component, following a very strong 2024 which also benefitted from a one-off effect.

Outlook

The recent US and Israeli attack on Iran will exert a drag on the global economy, through both energy prices and general confidence. Before the attack, GDP was expected to expand by around 3% in 2026 thanks to previous interest rate cuts, more expansionary fiscal policy in many large economies and progressive easing of trade-related uncertainties. In the baseline scenario of a limited escalation of the attack, this drag is expected to be mild: less than 0.2 p.p. in the US, an energy self‑sufficient economy, 0.2–0.3 p.p. in the Euro area, and slightly more in Asia. The base scenario is based on the assumption that both the US and China have a vested interest in keeping the conflict contained: China depends on fossil energy imports from the region, while the US is approaching mid-term elections focused on the affordability crisis. Faced with a stagflationary shock, central banks may accept a rise in inflation, if oil prices spike only briefly. Still, this may reduce the room for the Fed to cut rates further. The potential impact on Euro area consumer prices may not be negligible. At the beginning of March it appears rather unlikely that the ECB would raise rates, but a long-lasting spike in energy prices would threaten that view, given the risks of second-round inflation effects. All in all, the evolution of the attack remains subject to high uncertainties, and a prolonged escalation would pose a risk of stagflation.

In this context, with the strategic plan Lifetime Partner 27: Driving Excellence, Generali is focused on executing according to its three strategic priorities, excellence in customer relationships, excellence in core capabilities and excellence in the Group’s operating model and based on its three foundations, People, AI and Data and Sustainability. The Group is deepening its Lifetime Partner relationships with seamless, personalised omni‑channel experiences, while accelerating growth in preferred profit pools, increasing technical proficiency and scaling AI and Group-wide assets.

In Life, capitalising on Generali’s broad customer base and strong distribution footprint, Generali’s focus remains on improving technical proficiency and on simplification, offering updated and integrated solutions to adapt to evolving customer needs throughout their lifetime. The main areas of focus include protection and health products, as well as capital-light savings solutions, with the goal of becoming the health partner of choice for each customer. The Group’s hybrid and unit-linked offers continue to be a priority to address growing customer needs for financial security with the objective to become the go-to partner for retirement and savings.

In P&C, the Group's objective is to maximise profitable growth - with a focus on non-motor lines - across the insurance markets where it operates, strengthening its position and offering, especially in countries with high growth potential. The Group confirms and reinforces its flexible approach to tariff adjustments, also considering a general increase in extreme natural events. The non-motor offer will continue to be enhanced through the addition of modular solutions designed to address specific customer needs. Generali will continue to increase its focus on developing insurance solutions related to the environment and climate change. As part of this, Generali has established the Group Climate Hub, which plays a key role in defining methodologies and approaches to understand and manage physical risks.

With reference to investment policy, the Group will continue to pursue an asset allocation strategy aimed at ensuring consistency with policyholder liabilities and improving risk-adjusted returns with a focus on increasing current income. Investments in private and real assets will continue to be pursued gradually to enhance portfolio diversification and capture opportunities, with a prudent approach that takes into account the lower liquidity and higher complexity of these instruments. In real estate, the Group will pursue a policy of geographical and sectorial diversification, closely monitoring and evaluating market opportunities and asset quality.

In Asset & Wealth Management, Generali will continue to expand its product offering, particularly in real and private assets, and enhance distribution channels while also benefitting from the investment capabilities obtained through the acquisition of MGG Investment Group. In Wealth Management, also thanks to the recent acquisition of Intermonte and the launch of Insurbanking, Banca Generali group will focus on enhancing its future growth path and maintaining robust shareholder remuneration.

Through the Lifetime Partner 27: Driving Excellence plan the Group is committed to delivering its ambitious 2025-2027 targets:

- strong earnings per share growth: 8-10% EPS CAGR2;

- solid cash generation: > € 11 billion cumulative Net Holding Cash Flow3;

- Increasing dividend per share4: >10% DPS CAGR5,with ratchet policy

underpinned by a clear capital management framework, with increased focus on shareholder returns:

- over € 7 billion cumulative dividends6 (2025-2027);

- a commitment to a minimum annual € 500 million share buyback, to be assessed at the beginning of each year of the plan (for a total commitment of at least € 1.5 billion5 over the plan), with a € 500 million share buyback executed in 2025 and a further € 500 million to be launched in 20265.

Generali's Sustainability Commitment

Sustainability is fully embedded in Generali’s Lifetime Partner 27: Driving Excellence strategy. The main achievements for 2025 include:

- as a responsible investor, +€ 8.7 billion vs FY2024 in climate investments solutions7 while continuing the decarbonisation of the corporate investment portfolio reaching -60%8 vs FY2019;

- as a responsible insurer, more than € 2.2 billion (+22.0% vs FY20249) in premiums from climate insurance solutions while continuing the decarbonisation of the private motor insurance portfolio reaching -24.4%10, and more than € 3.5 billion (+9.6% vs FY2024) in new business premiums from health and life protection, and pension insurance solutions for underserved customers;

- as a responsible employer, 85% of engagement rate (+2 p.p. vs FY2024), 31% of upskilling index and a 48.5% GHG emissions reduction from own operations against the base year 201911;

- as a responsible corporate citizen, through the global initiatives of The Human Safety Net, initiatives across 25 countries with more than 515,000 beneficiaries reached (+50.6% vs FY2024).

Thanks to these commitments and results, Generali’s leadership has been confirmed by independent assessments, including an ‘AAA’ MSCI ESG rating and inclusion in the Dow Jones Sustainability Index Best-in-Class.

Significant events after 31 December 2025

On January 7th, Generali placed a €650 million subordinated bond.

On January 14th, Giulio Terzariol assumed the role of Direttore Generale – Group Deputy CEO, following the positive completion of the customary regulatory process.

On February 10th, Generali announced it partners with Swiss Life Global Solutions establishing the global #1 employee benefits network based on a long-term commercial partnership and a binding commitment for the acquisition of Swiss Life Network (SLN) by Generali Employee Benefits (GEB).

On March 9th, Generali reached an agreement for the sale of its Irish and Northern Irish P&C operations.

Other significant events that occurred after the end of the period are available on the website.

***

The Annual Integrated Report and Consolidated Financial Statements 2025, as well as the Management Report and Parent Company Financial Statements 2025 will be published on the Group website on 24 March 2026.

Q&A conference call

The Group CEO, Philippe Donnet, the Direttore Generale – Group Deputy CEO, Giulio Terzariol, the Group CFO, Cristiano Borean, the Group General Manager, Marco Sesana and the CEO of Generali Investments Holding, Woody Bradford, will host the Q&A session conference call for the consolidated results of the Generali Group as of 31 December 2025, which will be held on 12 March 2026 at 12.00 pm CEST.

To follow the conference call, in a listen only mode, please dial +39 02 8020927.

***

The Manager in charge of preparing the company’s financial reports, Cristiano Borean, declares, pursuant to paragraph 2, article 154 bis of the Consolidated Law on Finance, that the accounting information in this press release corresponds to the document results, books and accounting entries.

Generali 4Q2025 results

Further information by segment

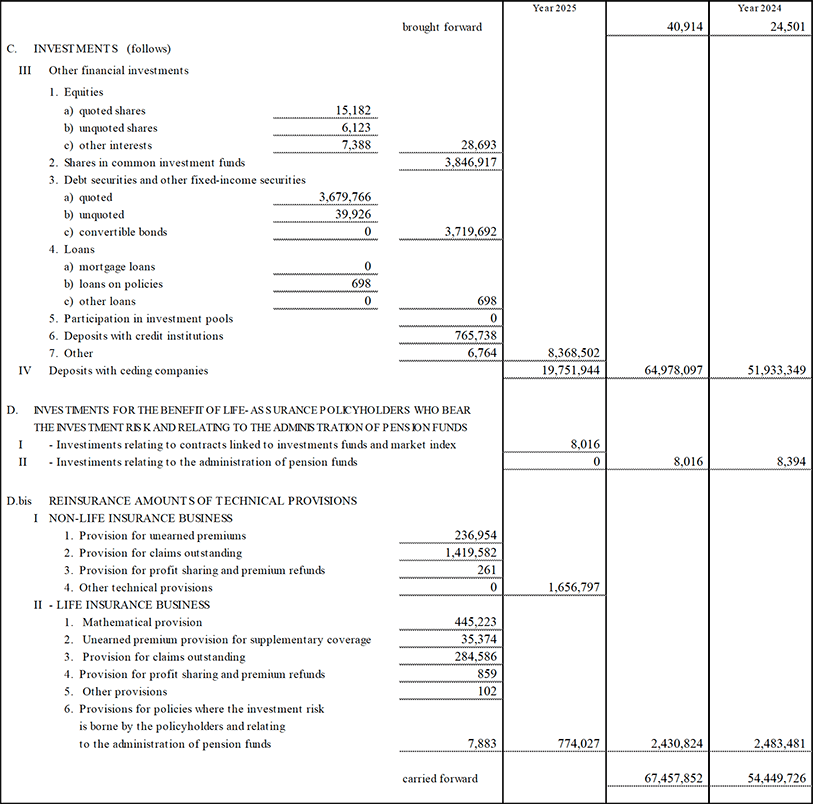

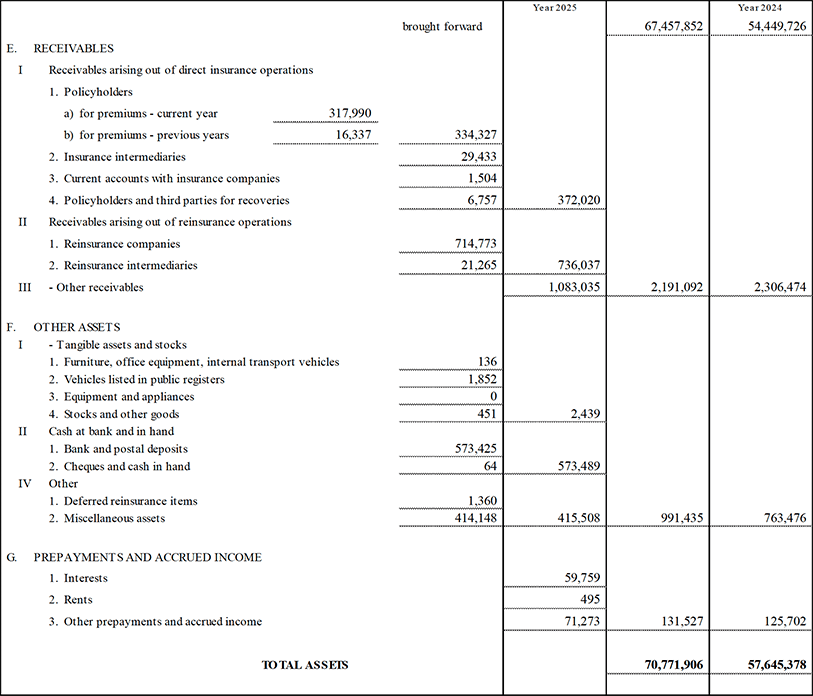

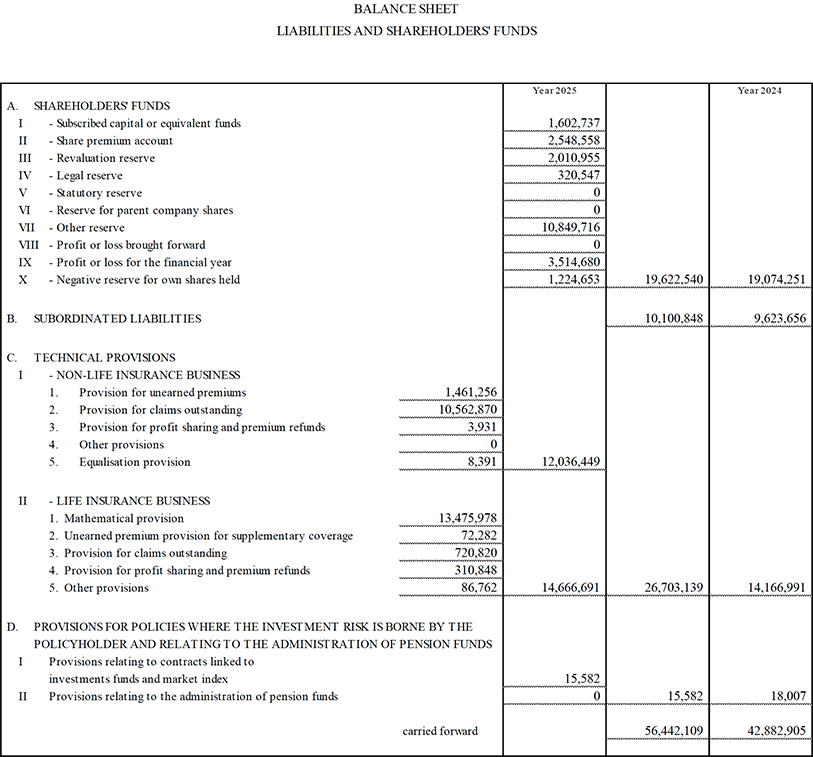

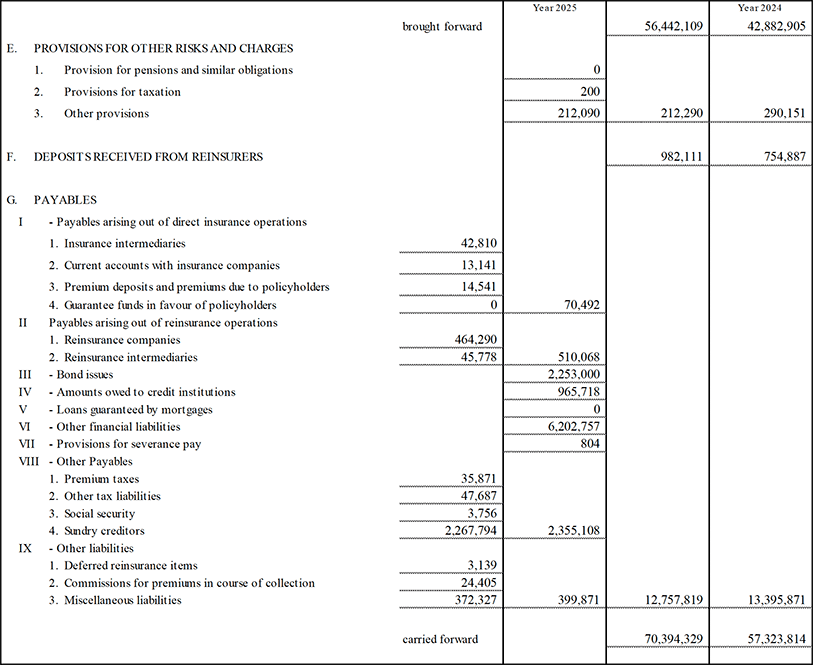

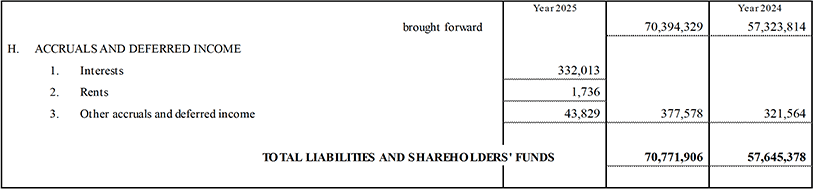

Balance sheet (12)

Income statement

Parent Company’s Balance Sheet and Income Statement (13)

(in thousands euro)

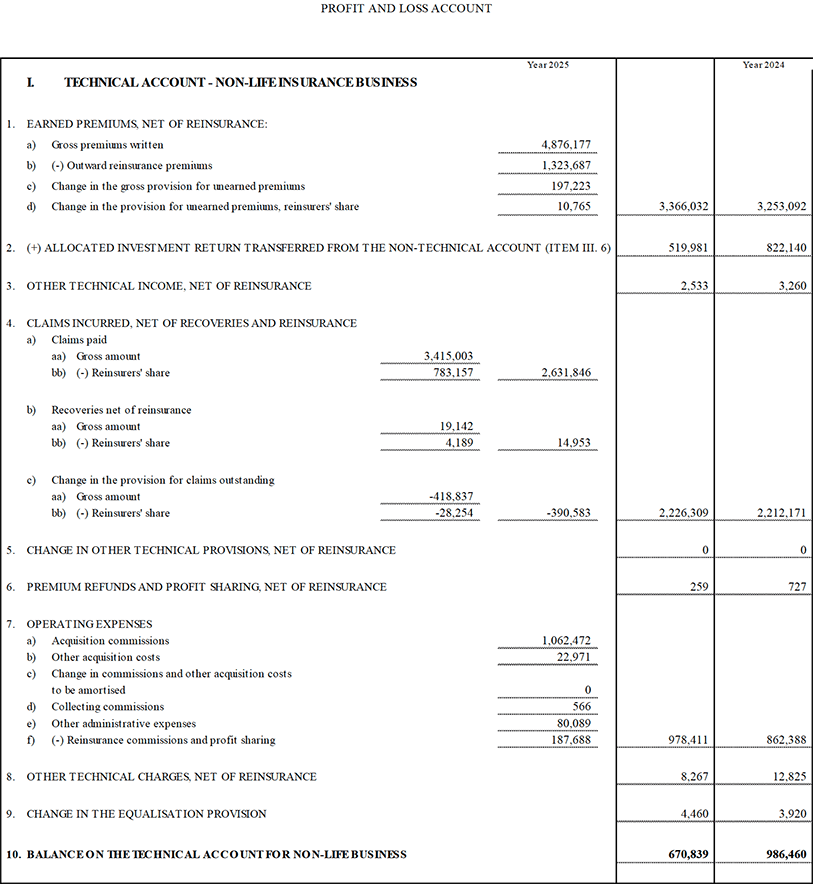

Profit and Loss Account

(in thousands euro)

1 For definition of the adjusted net result, please refer to note 2 on page 2.

2 3-year CAGR based on the Group’s adjusted net result.

3 Expressed on cash basis.

4 Subject to all relevant approvals.

5 3-year Dividend per Share (DPS) CAGR with 2024 baseline at € 1.28 per share.

6 Subject to all relevant approvals.

7 Target is +12 € Bn and it is measured as 2025-2027 cumulated net new investments. Target covers a broad range of asset classes, both direct investments and funds, and includes bonds, corporate, government infrastructure debt-equity, and real estate. Subject to market environment and constraints.

8 Target for corporate investments includes listed equity, corporate bonds within the general account portfolio and it is -60% YE29 vs YE19. For listed equity and corporate bonds, the reduction is measured by carbon intensity weighted on € Mn invested (YE25: 72.7 tCO2e/€ Mn). Subject to market environment and constraints. Target for real estate is -60% YE29 vs YE19. The reduction is measured by carbon intensity per square meter. Subject to market environment and constraints. At YE2025 the reduction for Real Estate portfolio accounts for 61% vs FY2019 (YE 25: 23.9 kgCO2e/m2).

9 Target is 8-10% 2024-2027 GDWP CAGR. It includes car coverages for green mobility, energy efficiency and renewable energy business. Subject to market environment and constraints.

10 Target for Personal Motor portfolio is -30% YE30 vs YE21 reduction, measured by carbon intensity weighted on GWP and includes motor underwriting private portfolios of Italy, Germany, France, Switzerland, Austria, Czech Republic, Hungary, Slovenia, Poland, Spain, and Portugal (YE25: 0.26 ktCO2e/€ Mn); Target for GC&C portfolio is -40% YE30 vs YE21, for corporate clients with public emissions. Subject to market environment and constraints. At YE2025 the reduction for GC&C portfolio accounts for 33.7% vs YE21 (YE25: 0.18 ktCO2e/€ Mn).

11 Target is -60% YE30 vs YE19. It includes scope 1, 2, and 3 emissions and it is calculated in absolute GHG emissions. Net-zero target for own operations is anticipated to 2035. Subject to market environment and constraints.

12 With regard to the financial statements envisaged by law, note that the statutory audit on the data has not been completed. The Group will publish the final version of the Consolidated Full-Year Financial Report 2025 in accordance with prevailing law, also including the Independent Auditor’s Report. In compliance with IFRS8, it should be noted that, following the changes introduced by the application of the new IFRS9 and IFRS17, comparative data in the financial statements have been appropriately restated.

13 With regard to the financial statements envisaged by law, note that the statutory audit on the data has not been completed. The Group will publish the final version of the Proposal of Management Report and Financial Statements of Parent Company 2025 in accordance with prevailing law. In compliance with IFRS8, it should be noted that, following the changes introduced by the application of the new IFRS9 and IFRS17, comparative data in the financial statements have been appropriately restated.